The Copyright Royalty Judges have announced that the new COLA-adjusted minimum statutory rate for 2026 is 13.1¢ for physical and downloads, up from 12.7¢, effective 1/1/26. This is the last year of the Phonorecords IV rate period, so that’s an increase from the 9.1¢ frozen mechanical rate that had been in effect for 15 years.

The adjusted rate stands in stark contrast to the streaming mechanical which not only has been frozen for the entire 5 year rate period, but has actually declined substantially due to Spotify’s bundling silliness. That smooth move has set up what will no doubt be a donnybrook in Phonorecords V, i.e., the next rate proceeding which is due to start any minute now (actually more like January, which is close enough).

It must be said that the reason there’s a rate increase for physical/downloads is due to the efforts of independents who filed two rounds of comments in Phonorecords IV and also the willingness of the labels to be flexible and reasonable. I suspect that has a lot to do with the fact that at the end of the day, we are all in the same business and it’s to everyone’s advantage that songwriters thrive. Obviously, the same cannot be said of the streaming platforms like Spotify that are busy seeding AI tracks with both hands. I really don’t know what business those people think they are in, but it’s not the music business.

We are rapidly approaching the next rate-setting proceeding before the three-judge panel at the Copyright Royalty Board for the royalty payable to copyright owners (and ultimately to songwriters) for exploitations of songs. These proceedings set rates for the next five year period and are numbered to tell them apart. The last proceeding, for example, was styled “Phonorecords IV” or sometimes “CRB 4” for those who struggle with long words. (Using the “CRB” acronym instead of “Phonorecords” is actually misleading because the CRB sets a number of rates.)

The proceedings will likely be divided in two: One proceeding for songs exploited in physical records like vinyl, CDs and permanent downloads and one proceeding for streaming mechanicals. These hearings are simultaneous and not sequential, so each hearing will be conducted side by side.

One reason for these simultaneous hearings is that the participants in each of the proceedings differ–the physical/download participants are songwriters and publishers on one side and the record companies on the other. The streaming participants are (often) the same songwriters and publishers on one side, but the streaming services are on the other.

The participants are incented to reach a voluntary settlement that they then present to the Copyright Royalty Judges for approval. The settlement negotiations are largely conducted in secret and no one on the songwriter side except a couple of participants knows anything about the terms of the settlement until it is presented to the Judges and the Judges make it public.

At this point, the Judges are required to entertain comments from the public as to whether the public supports the settlement (as required under a federal law applicable to all of the administrative state agencies from the Environmental Protection Agency to the Social Security Administration to the Copyright Royalty Board).

No matter how much some of the publishers would like to spin it, it is this public comment step where it all began to fall apart during the last proceeding styled “Phonorecords IV”, particularly over the “frozen mechanicals” issue. Signally, this disintegration of the initial physical/downloads “settlement” attracted a prairie fire of public comments that rejected the authority of the NMPA and NSAI to speak on behalf of all songwriters and publishers and also rejected the side deal that these groups had negotiated with the labels. The Judges listened, and the Judges rejected that settlement–I believe for the first time in the history of the rate setting proceedings.

The same was not true of the streaming mechanicals piece, however. I never did read a well-reasoned explanation for why participants lacked authority to speak on behalf of all songwriters, i.e., beyond their own members, in the frozen mechanicals proceeding, but that authority could not be questioned in the streaming proceeding. It should have been apparent to anyone paying attention that any consensus behind the time-encrusted “Big Pool” royalty calculation method for streaming mechanicals was rapidly crumbling apart. The Judges’ “39 Steps” royalty calculation is as mysterious as a Hitchcock movie and many did not trust it. And more importantly for our discussion today–still do not trust it at all.

As we approach Phonorecords V, there are some fundamental questions that all involved need to be asking themselves. The first is whether we want to go back to the same tired process of secret meetings with the big reveal resulting in public hostilities in the comments–against what is ostensibly our side. This before we even get to the negotiation with the other side.

The powers that be had the chance over the last few years to bring in some different viewpoints. Had they done so, they would have both diffused the inevitable collision, but could also have gotten the benefit of those viewpoints when there was still time to build alliances. There’s an idea–an integrative negotiation with a collaborative outcome.

Another fundamental question is whether we can reach a fairly quick deal with the labels on the physical/download side so that all concerned can turn their attention to bringing the streaming rates into some semblance of reality. Because the songwriters did such a persuasive job of raising the frozen mechanicals rates from 9.1¢ to 12¢ plus a COLA, that minimum statutory rate has now increased to 12.7¢. Given current inflation projections, it’s likely that the statutory rate will increase to about 13¢ and change by the end of 2026.

If a settlement could be reached quickly, it would not surprise me if someone came up with the idea of simply taking the then-extant minimum rate (for 2027) as the new base rate for the first year of Phonorecords V (2028) plus extending the annual COLA to protect songwriters in the out-years of PR V. Wherever the actual penny rates end up, if the songwriters and labels could reach an agreement quickly, it would save a bunch of effort and allow everyone to turn their attention to the streaming rates.

I wonder if it’s even possible to reach a negotiated settlement with the streaming services on the streaming mechanical. The entire concept of the “Big Pool” royalty rate is failing for streaming on both the sound recording and the song side of the deals. It was, frankly, a silly idea to begin with–and that takes us back to the beginning of streaming when deals were poorly negotiated with little to no accountability because physical still paid the bills. The general idea was that “superfans” would rule according to Thomas Hesse in Billboard who was around at the time: “If you get to superfans, who listen to music all the time, you get to all the money — not just from those people, but you get all the money from everybody.” The reality is that you can replace “superfans” with “superstars” or more simply, “market share”, and you would have a much better understanding of the “Big Pool” concept. The Big Pool is actually just a hyper efficient marketshare distribution of a pool of money.

What Spotify has demonstrated with their short sighted move on bundling is simply all the reasons why they are disliked and untrustworthy. They said the quiet part out loud–we have no idea what we are doing in this business but we–and not songwriters or musicians–are getting stupid rich at it. It is unlikely that anyone is going to welcome more of the same in Phonorecords V.

What is becoming apparent to an increasing number of songwriters is that there is one metric that matters to Spotify’s CEO–stock market valuation. That is what has made him a billionaire. That is what has made plenty of people at Spotify into millionaires. That is also the one metric that songwriters and artists have never participated in. Our negotiators have had their eye on the wrong ball.

I say if we’re going to spend millions on the government’s rate proceedings anyway, let’s get something for it for a change, shall we?

God gave Noah the rainbow sign, no more water, the fire next time.

James Baldwin, The Fire Next Time

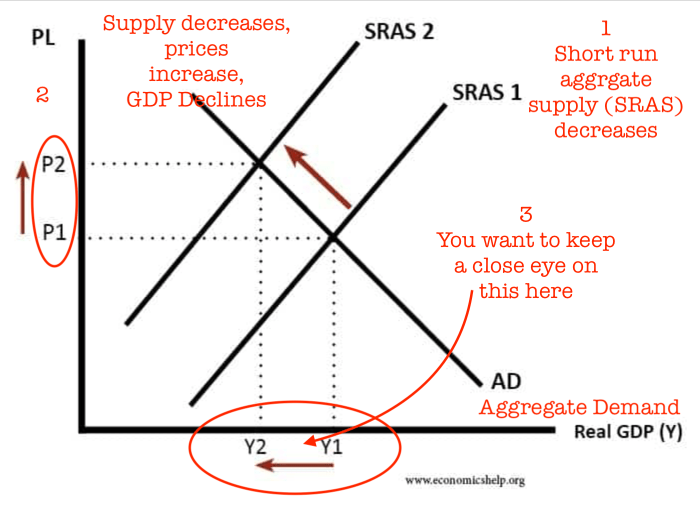

Remember the stagflation three point play? Supply contracts, prices go up due to those supply side shocks and real gross domestic product contracts. Stagflation also results in higher unemployment. Stagflation can take a long time to shake out of an economy once it sets in.

Stagflation’s three point play

We can learn from the economic history of stagflation, particularly in Japan and the U.S. Japan had a stagflationary period started by the economic shock of the collapse of Japan’s real estate market (not unlike what is happening in China with Evergrand and Sinic) and the follow on effect of a 60% decline in Japan’s stock market. The U.S. had a stagflationary period in the 1970s brought on by a dependence on foreign oil and predatory pricing largely by OPEC. That led to skyrocketing oil prices and gas lines. Both countries experienced a “Lost Decade” due to stagflation.

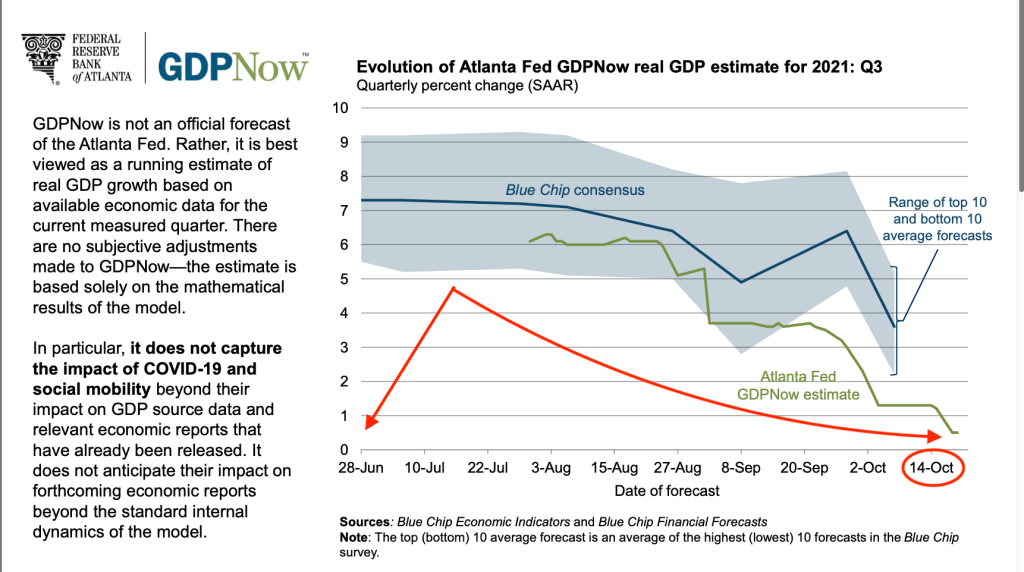

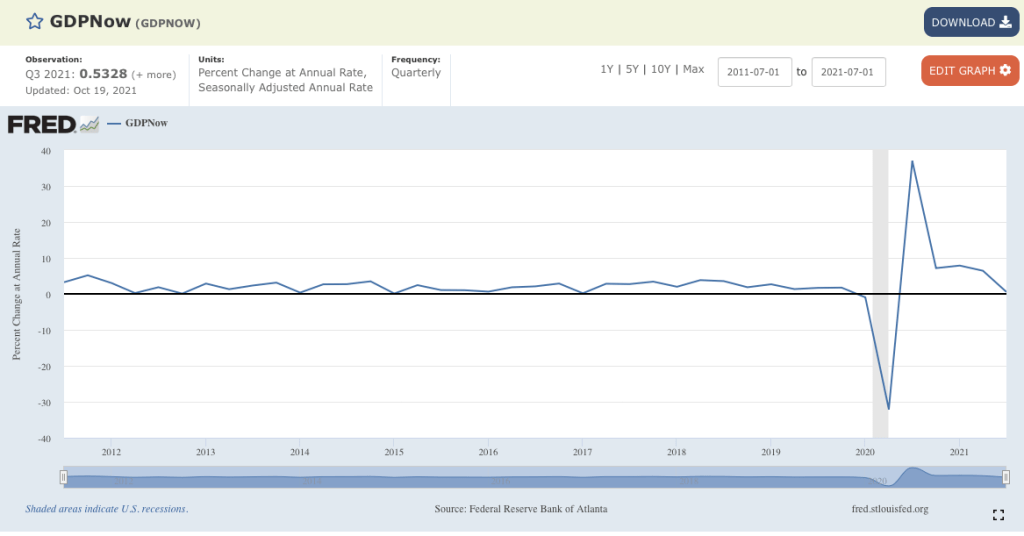

The Federal Reserve Bank of Atlanta announced this week that it projects real GDP grown in the third quarter of 2021 to fall to 0.5% with some caveats:

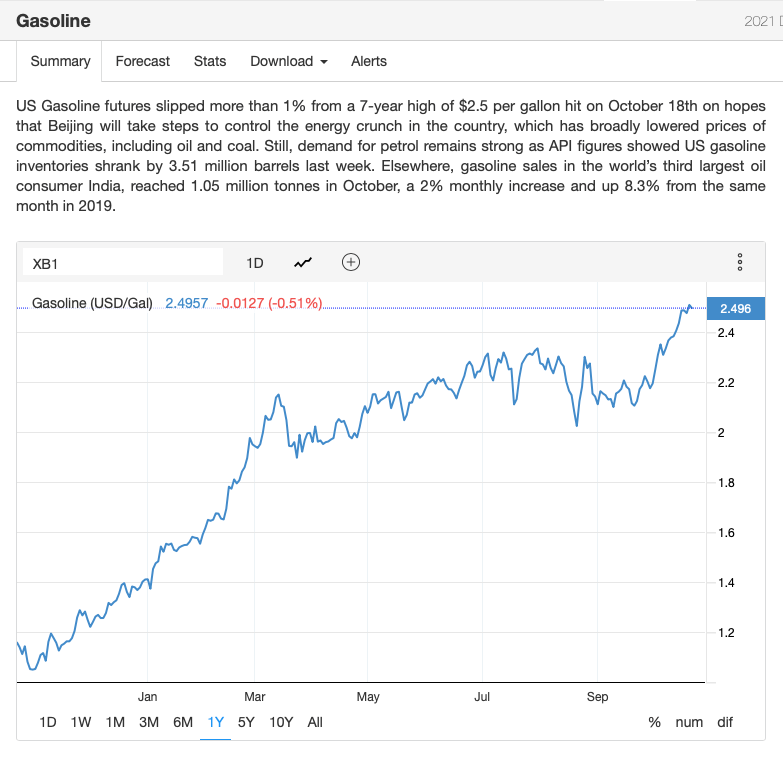

The point of these graphs is to emphasize that the US economy appears to be heading to a contraction and inflation brought on by a combination of supply side shocks (cost-push inflation) and demand caused in part by government actions (demand-pull inflation) combined with sharp increases in gasoline prices among other commodities. Gasoline prices ratchet through many products in the economy and have been sharply higher over the last 12 months as the U.S. became more dependent on OPEC production.

All the indications are that the U.S. may be headed into a prolonged period of stagflation which is inflation combined with a stagnating economy. It seems less and less likely that inflation is “transitory” and more likely that it will last well into 2023 and possibly 2024.

How does this affect songwriters? Remember that the mechanical rates set in the current Copyright Royalty Board rate proceeding will fix prices until 2027, so it appears that there will be considerable overlap between the inflation cycle and the royalty rates–all the more reason to seek the same inflation indexing for songs as the CRB recently granted for sound recordings.

Readers should now better understand the century of sad history for U.S. mechanical royalties that cast a long commercial shadow around the world. This history explains why extending the freeze on these mechanical rates in the current CRB proceeding (“Phonorecords IV”) actually undermines the credibility of the Copyright Royalty Board if not the entire rate setting process. The CRB’s future is a detailed topic for another day that will come soon, but there are many concrete action points raised this week for argument in Phonorecords IV today–if the parties and the judges are motivated to reach out to songwriters.

Let’s synthesize some of these points and then consider what the new royalty rates on physical and downloads ought to be.

1. Full Disclosure of Side Deals: Commenters were united on disclosure. Note that all we have to go on is a proposed settlement motion about two side deals and a draft regulation, not copies of the actual deals. The motion acknowledges both a settlement agreement and a side deal of some kind that is additional consideration for the frozen rates and mentions late fees (which can be substantial payments). The terms of the side deal are unknown; however, the insider motion makes it clear that the side deal is additional consideration for the frozen rate.

It would not be the first time that a single or small group negotiated a nonrecoupable payment or other form of special payment to step up the nominal royalty rate to the insiders in consideration for a low actual royalty rate that could be applied to non-parties. The rate—but not the side deal–would apply to all. (See DMX.)

In other words, if I ask you to take a frozen rate that I will apply to everyone but you, and I pay you an additional $100 plus the frozen rate, then your nominal rate is the frozen per unit rate plus the $100, not the frozen rate alone. Others get the frozen rate only. I benefit because I pay others less, and you benefit because I pay you more. Secret deals compound the anomaly.

This is another reason why the CRJs should both require public disclosure of the actual settlement agreement plus the side deal without redactions and either cabin the effects of the rate to the parties or require the payment of any additional consideration to everyone affected by the frozen rate. Or just increase the rate and nullify the application of the side deal.

It is within the discretion of the Copyright Royalty Judges to open the insider’s frozen mechanical private settlement to public comment. That discretion should be exercised liberally so that the CRJs don’t just authorize comments by the insider participants in public, but also authorize public comments by the general public on the insiders work product. Benefits should flow to the public–the CRB doesn’t administer loyalty points for membership affinity programs, they set mechanical royalty rates for all songwriters in the world.

2. Streaming Royalty Backfire: If you want to argue that there is an inherent value in songs as I do, I don’t think freezing any rates for 20 years gets you there. Because there is no logical explanation for why the industry negotiators freeze the rates at 9.1¢ for another five years, the entire process for setting streaming mechanical rates starts to look transactional. In the transactional model, increased streaming mechanicals is ultimately justified by who is paying. When the labels are paying, they want the rate frozen, so why wouldn’t the services use the same argument on the streaming rates, gooses and ganders being what they are? If a song has inherent value—which I firmly believe—it has that value for everyone. Given the billions that are being made from music, songwriters deserve a bigger piece of that cash and an equal say about how it is divided.

3. Controlled Compositions Canard: Controlled comp clauses are a freeze; they don’t justify another freeze. The typical controlled compositions clause in a record deal ties control over an artist’s recordings to control over the price of an artist’s songwriting (and often ties control over recordings to control over the price for the artist’s non-controlled co-writers). This business practice started when rates began to increase after the 1976 revision to the U.S. Copyright Act. These provisions do not set rates and expressly refer to a statutory rate outside of the contract which was anticipated to increase over time—as it did up until 2006. Controlled comp reduces the rate for artist songwriters but many publishers of non-controlled writers will not accept these terms. So songwriters who are subject to controlled comp want their statutory rate to be as high as possible so that after discounts they make more.

Because controlled comp clauses are hated, negotiations usually result in mechanical escalations, no configuration reductions, later or no rate fixing dates, payment on free goods and 100% of net sales, a host of issues that drag the controlled comp rates back to the pure statutory rate. Failing to increase the statutory rate is like freezing rate reductions into the law on top of the other controlled comp rate freezes—a double whammy.

It must be said that controlled compositions clauses are increasingly disfavored and typically don’t apply to downloads at all. If controlled comp is such an important downward trend, then why not join BMG’s campaign against the practice? If you are going to compel songwriters to take a freeze, then the exchange should be relief from controlled compositions altogether, not to double down.

4. Physical and Downloads are Meaningful Revenue: Let it not be said that these are not important revenue streams. As we heard repeatedly from actual songwriters and independent publishers, the revenue streams at issue in the insider motion are meaningful to them. Even so, there are still roughly 344.8 million units of physical and downloads in 2020 accounting for approximately $1,741.5 billion of label revenue on an industry-wide basis. And that’s just the U.S. Remember—units “made and distributed” are what matter for physical and download mechanicals, not “stream share”. If you don’t think the publishing revenue is “meaningful” isn’t that an argument for raising the rates?

U.S. Recorded Music Sales Volumes and Revenue by Format (Physical and Downloads) 2020

5. Inflation is Killing Songwriters: The frozen mechanical is not adjusted for increases in the cost of living, therefore the buying power of 9.1¢ in 2006 when that rate was first established is about 75% of 9.1¢ in 2021 dollars.

6. Willing Buyer/Willing Seller Standard Needs Correction: When the willing buyer and the willing seller are the same person (at the group level), the concept does not properly approximate a free market rate under Section 115. Because both buyers and sellers at one end of the market are overrepresented in the proposed settlement, the frozen rates do not properly reflect the entire market. At a minimum, the CRJs should not apply the frozen rate to anyone other than parties to the private settlement. The CRJs are free to set higher rates for non-parties.

7. Proper Rates: While the frozen rate is unacceptable, grossing up the frozen rate for inflation at this late date is an easily anticipated huge jump in royalty costs. That jump, frankly, is brought on solely because of the long-term freeze in the rate when cost of living adjustments were not built in. The inflation adjusted rate would be approximately 12¢ (according to the Bureau of Labor Statistics Inflation Calculator https://www.bls.gov/data/inflation_calculator.htm).

Even though entirely justified, there will be a great wringing of hands and rending of garments from the labels if the inflation adjustment is recognized. In fairness, just like the value of physical and downloads differ for independent publishers, the impact of an industry-wide true-up type rate change would also likely affect independent labels differently, too. So fight that urge to say cry me a river.

Therefore, it seems that songwriters may have to get comfortable with the concept of a rate change that is less than an inflation true up, but more than 9.1¢. That rate could of course increase in the out-years of Phonorecords IV. Otherwise, 9.1¢ will become the new 2¢–it’s already nearly halfway there. The only thing inherent in extending the frozen mechanicals approach is that it inherently devalues the song just at the tipping point.