For the past two years, Wall Street has treated artificial intelligence as a one-way trade. Hyperscalers, semiconductor companies, utilities, private-credit funds, and data-center developers have committed hundreds of billions of dollars to what may ultimately become nearly $1 trillion in AI-related infrastructure investment over roughly two years.

The underlying assumption has been remarkably consistent: demand for increasingly powerful AI models will continue growing fast enough to justify unprecedented spending on chips, data centers, transmission lines, substations, and electric generation.

But investment booms rarely end because one assumption proves wrong. They end when several assumptions begin to weaken at the same time.

That appears to be happening.

Ed Dowd’s recent Substack analysis argues that the economics supporting today’s AI buildout are becoming increasingly fragile. Financing is tightening. Enterprise customers are demanding clearer returns on investment. Open-weight models continue improving while driving prices lower. And perhaps most importantly, the physical infrastructure required to support AI is becoming a political issue.

Gary Marcus recently challenged David Sacks’ argument that regulation is the principal threat to American AI leadership (Sacks really needs some new sheet music). Marcus instead argued that the industry faces a far more fundamental economic problem:

“The real issue is that LLMs are commodities; lots of people know how to make them, and everybody is doing more or less the same thing, training on more or less the same data. That means nobody has a technical moat. Which means you get price wars and low margins and more and more competitors over time.”

If Marcus is right, Wall Street may eventually discover that AI resembles cloud computing more than pharmaceuticals. There may be tremendous demand—but not necessarily extraordinary profits. That observation dovetails with Goldman Sachs’ increasingly cautious assessment of the AI investment cycle. Goldman has repeatedly warned investors that the buildout depends on continued access to capital, sustained enterprise demand, adequate electric power, and enough economically valuable use cases to justify unprecedented capital expenditures.

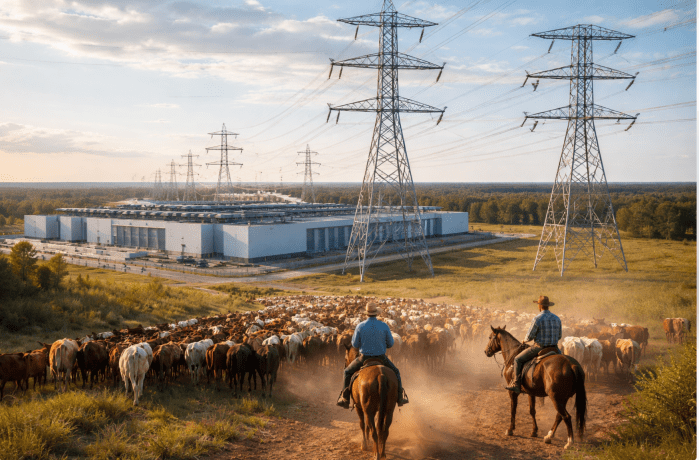

AI does not exist in ‘the cloud.’ It exists on electric grids. Every new model depends on substations, transmission lines, transformers, cooling systems, water supplies, and local political consent.

For months, we’ve tracked what has become a genuine data center backlash. Communities across Texas, Georgia, Louisiana, Virginia, Oklahoma, Utah, Alabama, and elsewhere are increasingly questioning the costs of hosting massive AI infrastructure.

Politicians, meanwhile, are discovering that AI infrastructure is much easier to announce than it is to build. Many governors and local officials have promoted data centers by assuring taxpayers that the projects will ‘pay their own way.’ But that message begins to unravel the moment the infrastructure breaks ground or annexes farmland.

A homeowner facing a 765-kV transmission line across family property is unlikely to be persuaded that the project is privately financed. Likewise, a rancher confronting eminent domain does not care whether the transmission costs appear on a utility bill, a corporate balance sheet, or a tax-abatement agreement. The injury is the same: the family home, ranch, or farm is permanently altered to support infrastructure serving distant customers—who are often anonymous.

In the Texas Hill Country, landowners have mobilized against new transmission corridors intended to serve future electric demand, including AI-related growth. In Coweta County, Georgia, residents organized after learning that transmission infrastructure associated with large-scale data-center development could cut through long-held family properties. The debate quickly ceased being about economics and became about land, community, and the limits of eminent domain.

This is where many elected officials have found themselves trying to have it both ways. They assure taxpayers that private investment will shoulder the costs while simultaneously offering substantial tax abatements, infrastructure incentives, expedited permitting, and other forms of public support. Then, when opposition emerges, they discover that the political issue is no longer who pays for the infrastructure—it’s who lives with it.

For families whose property lies in the path of a transmission corridor, ‘the data centers will pay for themselves’ is not an answer. Their concern is not the financing model. Their concern is keeping the home that has been in the family for generations.

None of this means AI is a passing fad. Transformative technologies often survive speculative bubbles. The internet certainly did. But many companies that financed the dot-com boom did not survive intact, and many investors paid dearly for assuming that technological transformation automatically translated into sustainable profits.

Today’s AI investment cycle rests on multiple pillars: inexpensive capital, robust enterprise demand, premium pricing, abundant electricity, and political support for rapid infrastructure expansion. Gary Marcus questions the durability of the competitive moat. Goldman Sachs questions whether the economics can support the investment. Communities across America are questioning whether they should bear the physical burdens.

Those three conversations are converging. The story is no longer simply about faster models or larger training runs. It is about economics, infrastructure, and public acceptance. The market has spent the last two years pricing AI as though all three will remain aligned indefinitely. History suggests that is a very demanding assumption.

The most important data center story today wasn’t a zoning hearing, a transmission line fight, or a new hyperscaler valuation announcement.

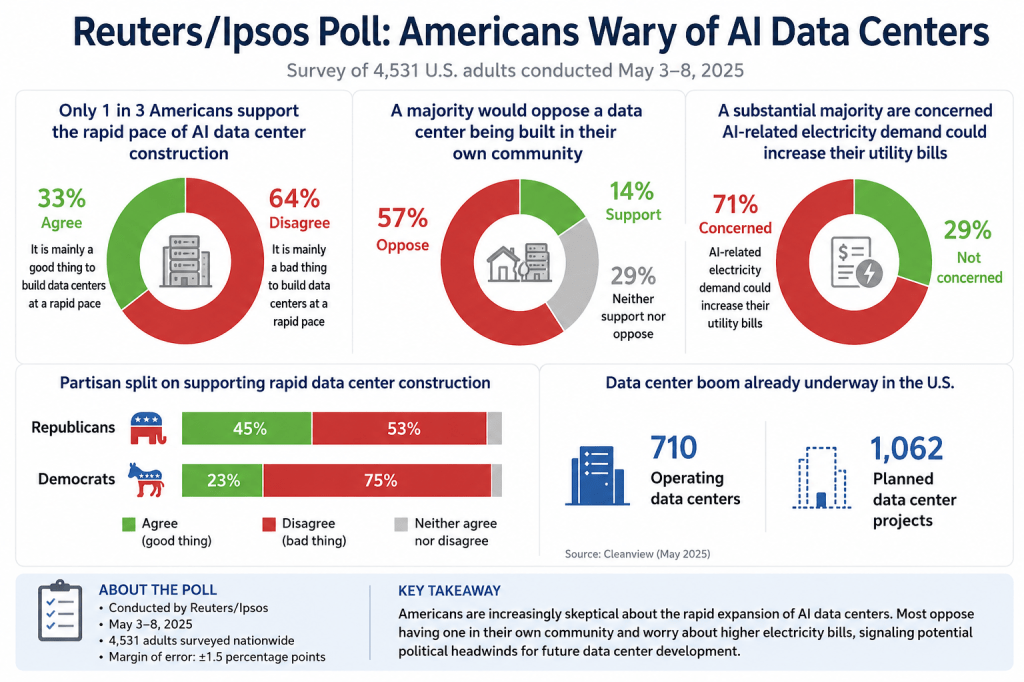

The most important story is a poll. And that poll may not only capture the sentiment of the public, it may also indicate which way elected officials and financiers are leaning, too.

A new Reuters/Ipsos survey found that only one-third of Americans support the current pace of AI data center construction, while nearly two-thirds oppose it. More than half said they would oppose a data center in their own community, and a substantial majority expressed concern that AI-related electricity demand could increase their utility bills.

The six-day poll, which surveyed 4,531 people across the country and closed on Monday, showed just 33% of Americans agreed with a statement that it was mainly a good thing to build data centers at a rapid pace. Some 64% disagreed….Some 57% of people surveyed – including two-thirds of Democrats and half of Republicans – also said they would oppose a data center being built in their community. Just 14% of survey takers said they were okay with a center being built near them, according to the Reuters/Ipsos poll.

The lopsided result should not be surprising.

For the past two years, the public conversation around data centers has focused on American AI leadership (“because China”), economic development, and technological competitiveness. But many communities are experiencing something very different: transmission line easements criss-crossing private property, industrial-scale facilities near homes, rising utility concerns, water consumption, noise, and tax incentives for some of the world’s largest companies. It may be starting to dawn on the public why the White House AI Czar David Sacks was so obsessed with blocking any state laws that got in the way of AI.

In some cases, the issue goes even further. Landowners are being asked to surrender property rights through eminent domain—or the threat of eminent domain—so that transmission infrastructure can be built to serve facilities whose ultimate beneficiaries are among the wealthiest technology companies in the world.

Imagine you were the man who fell to earth and you knew nothing about AI workflow. Would you look at all these data centers, substations, behind the meter nuclear reactors and transmission lines and say “oh, that makes total sense”? Or would you ask what are these people thinking building a supply chain this kludgy with myriad points of failure? Data centers in space? Really? What could possibly go wrong?

That is where the national security narrative begins to collide with local reality. “We have to do this because China” is a powerful slogan in Washington. For many landowners outside the Imperial City, however, it begins to ring hollow when the immediate consequence is a transmission easement across family property that will never happen in an urban setting.

This is particularly true when the economic justification depends on AI demand forecasts that may not even be tested—much less achieved—for years. Viewed from a kitchen window looking out at a new transmission corridor in what used to be your vegetable garden or a pasture for livestock, the sacrifice is immediate and personal, while the promised strategic benefits remain abstract and distant.

We’ve already seen an econometric study from Professor Michael Hicks at Ball State University showing that all the hundreds of data centers in Texas have led to pretty much a wash in job creation, a major selling point that few ever believed. A University of Texas study shows that data centers could potentially account for 3% to 9% of Texas’ water use by 2040, according to a new white paper. In other words, Big Data has largely been talking about the benefits of AI while residents have been living with the costs of that infrastructure.

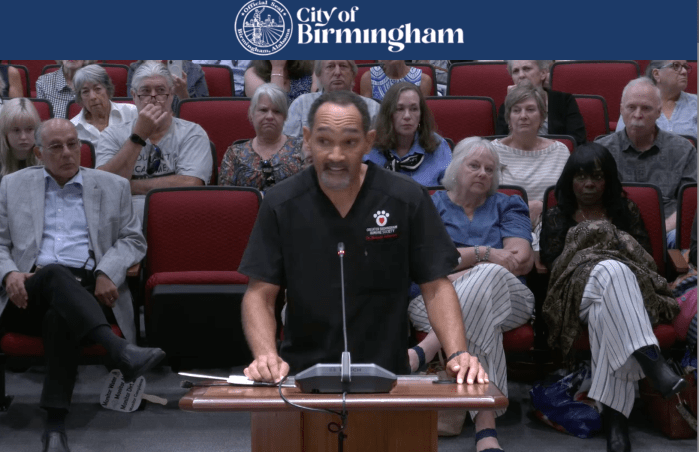

Chief Veterinary Officer for Greater Birmingham Humane Society Testifying against data center

Reverse Angle Showing City Council Left the building

The Reuters/Ipsos poll suggests the issue may be evolving from a collection of local land-use disputes into a national political movement. Historically, that is the point where elected officials begin to change their behavior. Local opposition can often be dismissed as isolated resistance. National polling is harder to ignore and could be the harbinger of somebody getting unelected.

The challenge for policymakers, utilities, and developers is that public concerns are becoming increasingly tangible while many projected benefits remain tied to forecasts extending years into the future with no current evidence. Voters tend to react more strongly to immediate and permanent impacts than to promised future gains that may never come to pass, particularly gains to other people who don’t have a transmission line in their garden or who were not forced to sell their family home to a power company.

That leads to a data center mobilization question that has received far less attention than corrupting farm land, water use, noise, or electricity rates: what happens if the forecasts are simply wrong?

Communities are being asked to accept transmission corridors, substations, power plants, and massive industrial facilities today based on projections of future AI demand that may extend a decade or more into the future. Yet the economics of AI remain highly uncertain as this week’s Google $85 billion equity round confirms. When Google’s AI capital expenditures exceeded even Google’s free cash flow, the Leviathan of Mountain View turned to a Silicon Valley favorite: Other people’s money. Revenue models are still evolving, competition is intense, and many of the assumptions underlying today’s infrastructure buildout have not yet been tested through a full business cycle.

Crucially, Investors are funding unprecedented AI capex on the assumption of durable competitive advantages, yet the underlying LLM asset increasingly exhibits commodity characteristics. Meaning the models are all very similar in the fundamental components. As hyperscalers converge on functionally similar models, infrastructure, and services at extraordinary cost, there is less and less that distinguishes one from the other. When Google chooses to finance capex out of equity rather than continue financing from free cash flow and debt, that may also tell us something about the appetite of lenders getting a little skeptical.

It’s not just Google. Consider the implications of the recent reports surrounding SoftBank’s OpenAI investment. SoftBank participated in OpenAI’s February 2026 funding round at a valuation of approximately $840 billion and emerged with roughly 13% ownership. On paper, SoftBank’s stake in OpenAI carried an implied value of approximately $109 billion.

Yet when SoftBank reportedly sought to get a margin loan on those same shares a few weeks ago (three months after the $840 billion valuation was set) using that position as collateral, lenders appear to have viewed the value of the OpenAI shares very differently. The company initially sought a $10 billion loan secured by its OpenAI shares, later reducing the request to approximately $6 billion after lender interest reportedly proved limited. Even at the lower amount, loan negotiations have reportedly stalled.

The significance is not just that SoftBank’s OpenAI position is worth only $6 billion (implied $46B valuation) or $10 billion as margin loan collateral, if that. Rather, it highlights the distinction between venture valuation, financing valuation, and realizable value. An $840 billion venture valuation reflects what investors were willing to pay in a private financing round under specific assumptions about future growth, profitability, and market structure.

A margin lender asks a different question: if the collateral must be liquidated under adverse circumstances like a bubble burst or the recent semiconductor crash, what is it actually worth? The resulting margin discount can be substantial, even taking into account the usual 50%-ish haircut on marginable securities. For AI investors, this episode may be one of the first visible indications that sophisticated credit markets are assigning materially different risk assessments to AI assets than those implied by headline-grabbing private-market valuations fueled by cheerleading from the financial press and, it must be said, the Oval Office.

Similar valuation disconnects have appeared before other major public offerings, including Spotify’s direct listing, WeWork’s failed IPO, and several high-profile technology listings where private-market expectations ultimately confronted public-market price discovery. For AI investors, the significance is less about OpenAI itself than what the episode may reveal about the difference between AI forecasts and the willingness of sophisticated creditors to finance those assumptions with actual cash.

Homes will be sacrificed – said Holly Lovett, spokeswoman for @GeorgiaPower this article is our local newspaper from November of last year. https://t.co/VsVNDg8P05

If those forecasts prove overly optimistic, the result may not simply be disappointed investors. The result could be stranded assets: transmission lines cutting across ranches and farms, substations occupying valuable land, and industrial facilities looming over communities long after the expected economic justification has faded. That burden may ultimately become the defining political challenge of the AI infrastructure era. People are not merely being asked to tolerate temporary construction. They are being asked to accept permanent changes both to their homes, to their property ownership, and to their communities in support of forecasts that may or may not materialize. If a ranch is involuntarily divided, a neighborhood industrialized, or a home taken for infrastructure justified by projected future AI demand, the consequences are real regardless of whether the forecast is ultimately correct.

The Reuters/Ipsos poll suggests that the next phase of the debate may be less about artificial intelligence itself and more about who bears the risks, costs, and consequences of the infrastructure being built to support it—and who bears the consequences for an unpopular mobilization if those forecasts turn out to be wrong.

That conversation—and the inevitable litigation—is only beginning.

2 LOCAL ENGINEERS refute the @DCBLOXinc rep’s claims: “Waterless cooling does not mean more environmentally-friendly… they are going to continually burn fossil fuels and pollute our communities… not just the one @NashvilleZoo, the one at @Fisk1866 too.” pic.twitter.com/MpZuqYEQ4j

For years, the political conversation around AI data centers followed a familiar script that was straight out of the Chamber of Commerce. Governors competed to announce the next hyperscale campus. Counties rezoned farmland and conservation land into heavy industrial corridors. Legislatures approved enormous tax abatements with little debate. Utilities promised “economic development.” And local officials were told that if they moved too slowly, some other state would take the project instead. Kind of like because China.

Data centers are receiving billions in tax breaks from the state of Georgia and they’re using eminent domain to take people’s family homes.

I’m the only candidate for Lt. Gov talking about this because I’m the only one who voted against it. pic.twitter.com/4jwIQJdVqF

— Senator Greg Dolezal (@DolezalForGA) May 23, 2026

Residents in Crowell, Texas are being forced to live with constant artificial daylight because of Google’s AI data center that is being built right next to them. Residents report severe 24/7 light pollution that creates artificial daylight at night (photo proof shown)

Why? Because even 10 years ago it was self-evidently true that there was no political opposition to Big Tech and nobody looked too hard at the reality of data centers in the places we had observable data like Oregon, for example. If they had, they would have known there was one thing that was absolutely true—data centers were not factories and they produced higher electric bills and fewer jobs. At least once the sugar high of construction had passed.

And speaking of jobs, in a November 2025 difference-in-differences study, economist Michael J. Hicks examined every data center opened in Texas and found zero statistically significant net employment effect — job gains in the data center sector were fully offset by losses in other industries, yielding an average treatment effect of roughly 46 workers per facility that the author concludes is “correctly interpreted as zero,” less than one-tenth the jobs generated by a single Walmart Supercenter.

Good Jobs First has found that the three states that have measured their data center return on investment lose 52 to 91 cents on the dollar, and in Virginia alone, the sales and use tax exemption for data centers consumed 81.3% of the state’s entire economic development incentives budget in FY 2024.

But it’s not just light pollution. Even though it was patently obvious that the massive data centers that were getting built in Louisiana, Georgia, Utah and Nevada were vastly larger than the already operating data centers in Oregon and were guaranteed to chew up the environment way more, nobody bothered to put 2 and 2 together and check how deep the foundations were compared to local aquifers.

Just because she’s a socialist, doesn’t mean she’s wrong.

That script is now breaking down. I’m shocked, said no one.

As we told the UK Intellectual Property Office:

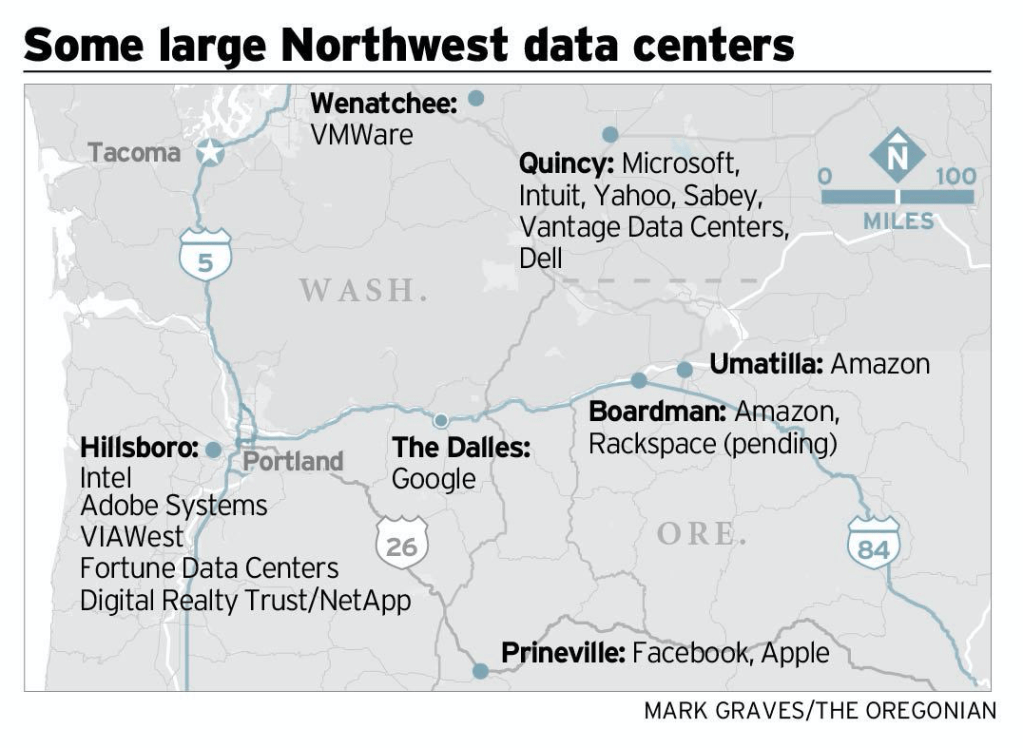

We call the IPO’s attention to the real-world example of the U.S. State of Oregon, a state that is roughly the geographical size of the UK. Google built the first Oregon data centre in The Dalles, Oregon in 2006. Oregon now has 125 of the very data centres that Big Tech will necessarily need to build in the UK to implement AI. In other words, Oregon was sold much the same story that Big Tech is selling you today.

The rapid growth of Oregon data centres driven by the same tech giants like Amazon, Apple, Google, Oracle, and Meta, has significantly increased Oregon’s demand for electricity. This surge in demand has led to higher power costs, which are often passed on to local rate payers while data centre owners receive tax benefits. This increase in price foreshadows the market effect of crowding out local rate payers in the rush for electricity to run AI—demand will only increase and increase substantially as we enter what the International Energy Agency has called “the age of electricity”.

Portland General Electric, a local power operator, has faced increasing criticism for raising rates to accommodate the encroaching electrical power needs of these data centers. Local residents argue that they unfairly bear the increased electrical costs while data centers benefit from tax incentives and other advantages granted by government.

This is particularly galling in that the hydroelectric power in Oregon is largely produced by massive taxpayer-funded hydroelectric and other power projects built long ago. The relatively recent 125 Oregon data centres received significant tax incentives during their construction to be offset by a promise of future jobs. While there were new temporary jobs created during the construction phase of the data centres, there are relatively few permanent jobs required to operate them long term as one would expect from digitized assets owned by AI platforms.

Of course, the UK has approximately 16 times the population of Oregon. Given this disparity, it seems plausible that whatever problems that Oregon has with the concentration of data centers, the UK will have those same problems many times over due to the concentration of populations.

This message is getting through to elected officials around the world because citizens are freaking out.

Quietly at first, and then all at once, states and local governments across the country began pushing back. Some are freezing approvals entirely. Others are reconsidering billions in tax incentives. Some are demanding that data centers pay the real cost of the transmission infrastructure they require instead of socializing those costs onto ordinary ratepayers and anyone else who drinks water and breathes air.

This is no longer a niche zoning issue in Northern Virginia or some European bureaucratic nonsense. It is becoming a national political movement that has some real populist overtones worthy of a Brexiteer. According to the National Conference of State Legislatures (NCSL), at least 11 states have introduced statewide moratorium or ban legislation targeting data centers. Meanwhile, Good Jobs First reports more than 60 local moratorium efforts nationwidethat at least 14 states and scores of localities are failing to disclose tax abatement revenue losses they are suffering to data centers — even though they have been required to do so under Generally Accepted Accounting Principles (GAAP) since FY 2017.

The reasons vary by region as you’d suspect, but the themes are becoming remarkably consistent, many of which Artist Rights Institute raised in our comments on the US AI Action Plan and the UK IPO AI consultation:

• massive electricity demand; • water consumption; • transmission line expansion; • opaque tax subsidies; • industrialization of rural communities; • secrecy surrounding the ultimate hyperscale users; • and growing fear that ordinary households will subsidize AI infrastructure through higher utility bills.

What is striking is not merely the existence of resistance. It is the geographic breadth of it.

In Texas, lawmakers enacted new large-load interconnection rules while Hill County adopted a temporary construction pause and Agriculture Commissioner Sid Miller publicly called for broader scrutiny of data centers. In Virginia, long considered the unquestioned capital of the data center industry, legislators are openly debating whether to scale back tax exemptions that helped fuel “Data Center Alley.” In Illinois, Governor Pritzker proposed suspending new tax incentives entirely for two years.

Even places that aggressively courted data centers are beginning to hesitate.

In Reno, Nevada, officials adopted a pause on approving new data centers while they reevaluate land-use and infrastructure impacts. Duh. Ya think?

The Reno–Tahoe industrial corridor became a symbol of how quickly hyperscale development can transform an entire region once incentives and transmission infrastructure align. Nevada approved hundreds of millions in projected abatements over the last decade. Now local officials are asking whether the public actually understood the scale of what was being built. If you build it they will come, and they will take a huge dump in your backyard.

That same questions are emerging everywhere else: Who is the real end user? Who pays for the substations and 765-kV transmission lines? What happens if AI demand projections collapse halfway through construction? And why are local taxpayers subsidizing facilities that often employ surprisingly few permanent workers once operational? Well…not really surprisingly, but surprisingly if you believed the Chamber of Commerce hoorah.

The politics are changing because the physical footprint of AI is no longer abstract. The cloud is becoming visible. And you cannot bribe your way out of that one.

Pour some Sucre on them….

Residents now see the cooling towers. They see the transmission corridors. They hear the backup generators. In some communities they are learning about low-frequency industrial noise and infrasound issues that do not show up on ordinary decibel measurements. They see conservation land rezoned into industrial districts almost overnight. They see shell companies quietly assembling land while refusing to identify the ultimate hyperscale beneficiary.

Most importantly, they are beginning to understand that these projects are not temporary construction booms. They are permanent industrialization decisions. A 765-kV transmission corridor is not a pop-up startup. Neither is a hyperscale campus consuming as much electricity as a mid-sized city. And once the infrastructure is built, communities live with the consequences for generations.

The result is a new kind of political coalition that cuts across ideological lines. Environmental advocates, fiscal conservatives, rural landowners, grid-reliability hawks, and anti-subsidy activists are increasingly finding themselves on the same side of the debate. That does not mean the data center industry is stopping. Far from it. Billions are still flowing into AI infrastructure. Utilities continue planning enormous generation and transmission expansions. States remain eager for construction spending and property tax growth.

But the era of automatic approval is ending. The central political question is no longer whether AI infrastructure will expand. It is who bears the cost.

And there is another revealing development occurring at the federal level. What does it tell you that President Trump reportedly pulled back an executive-order framework that would have required certain AI labs to obtain government cybersecurity approval or clearance before launching advanced systems?

Whatever one thinks of the policy itself, the episode suggests intense behind-the-scenes conflict inside the administration and the AI industry over whether any meaningful federal guardrails should exist at all. Sources around Washington describe the push as a last-ditch effort by what critics derisively call the “Zombie AI Viceroy” David Sacks, the lobbyist who seemingly cannot be fired because the entire AI infrastructure race has become too politically and financially entangled. We will see whether federal safeguards reappear in another form. But at this moment, the practical reality is striking: the only governments actively imposing meaningful friction on AI infrastructure expansion are states, counties, and local municipalities.

State and Local Data Center Restriction / Tax Rollback Tracker (May 2026)

Alabama — Considering rules requiring data centers to bear infrastructure/grid costs

Arizona — Chandler pause; grid-cost proposals under consideration

California — Bills addressing ratepayer and environmental protections

Colorado — Denver moratorium; Larimer County pause; Logan County restrictions

Florida — Enacted protections for local zoning authority and ratepayer safeguards

Georgia — HB 1059 introduced forbidding local permitting until December 2028; local pauses; estimated $2.5 billion per year in tax abatement revenue losses (highest in nation)

Illinois — Governor called for two-year pause of data center tax incentives

Indiana — Considering restructuring of tax incentive revenue sharing; fails to disclose data center costs despite ranking fifth-best in subsidy transparency nationally

Louisiana — New Orleans temporary moratorium

Maine — LD 307 moratorium on data centers over 20 MW (vetoed by Governor); local moratoria

Michigan — State moratorium proposals; Ypsilanti pause

Minnesota — Removed electricity sales tax exemption; created new annual energy-use fee; Minneapolis moratorium discussions

Nevada — Reno approval pause; growing tax-abatement controversy; Controller issues exemplary annual report of local revenue losses from state-awarded abatements

New Hampshire — HB 1265 one-year moratorium on data center construction (failed)

New Jersey — Millville ban/restrictions; prevailing wage requirement for data center construction (enacted February 2026)

New York — AB 10141 / SB 9144 statewide moratorium and Public Utility Commission rulemaking (introduced); Athens/Dryden/Mount Morris local restrictions

North Carolina — Chatham County moratorium; additional local reviews

North Dakota — Oliver County temporary moratorium activity

Ohio — Numerous local pauses; growing subsidy backlash

Oklahoma — SB 1488 moratorium until November 2029 (introduced); incentive rollback proposals

Oregon — Affordability/reliability proposals tied to large-load users

Pennsylvania — Moratorium discussions underway (HB 1370 introduced per NCSL)

South Carolina — SB 567 proposal to restrict approvals pending oversight framework (introduced)

Texas — Large-load legislation; local moratoria and review fights; estimated $1 billion or more per year in tax abatement revenue losses; Hicks (2025) causal study found zero net job growth from data centers statewide

Vermont — S 205 proposed moratorium through 2030 with impact study requirement (introduced)

Virginia — HB 1515 prohibiting new approvals until interconnection requests fulfilled or July 2028 (continued); major debate over scaling back tax exemptions; estimated $1.94 billion per year in revenue losses; data center exemptions consumed 81.3% of state’s entire incentive budget in FY 2024

Washington — Restrictions tied to emissions-credit eligibility

Wisconsin — Moratorium proposal (status unverified; not listed in NCSL tracker)

The important point is not that every proposal will pass, which it may or may not. The important point is that resistance is no longer isolated. The backlash has become national. And resistance is not futile.

An important position paper from the Federal Trade Commission about AI (emphasis mine where indicated):

You may have heard that “data is the new oil”—in other words, data is the critical raw material that drives innovation in tech and business, and like oil, it must be collected at a massive scale and then refined in order to be useful. And there is perhaps no data refinery as large-capacity and as data-hungry as AI.

Companies developing AI products, as we have noted, possess a continuous appetite for more and newer data, and they may find that the readiest source of crude data are their own userbases. But many of these companies also have privacy and data security policies in place to protect users’ information. These companies now face a potential conflict of interest: they have powerful business incentives to turn the abundant flow of user data into more fuel for their AI products, but they also have existing commitments to protect their users’ privacy….

It may be unfair or deceptive for a company to adopt more permissive data practices—for example, to start sharing consumers’ data with third parties or using that data for AI training—and to only inform consumers of this change through a surreptitious, retroactive amendment to its terms of service or privacy policy. (emphasis in original)…

The FTC will continue to bring actions against companies that engage in unfair or deceptive practices—including those that try to switch up the “rules of the game” on consumers by surreptitiously re-writing their privacy policies or terms of service to allow themselves free rein to use consumer data for product development. Ultimately, there’s nothing intelligent about obtaining artificial consent.

The Securities and Exchange Commission is formalizing ESG disclosures for public companies like Spotify, stating that “[a]s investor demand for climate and other environmental, social and governance (ESG) information soars, the SEC is responding with an all-agency approach” and has taken many actions to require ESG disclosures. It was only a short step for the government to turn disclosure into violations and then turn violations into enforcement:

The Securities and Exchange Commission today announced the creation of a Climate and ESG Task Force in the Division of Enforcement. The task force will be led by Kelly L. Gibson, the Acting Deputy Director of Enforcement, who will oversee a Division-wide effort, with 22 members drawn from the SEC’s headquarters, regional offices, and Enforcement specialized units.

Consistent with increasing investor focus and reliance on climate and ESG-related disclosure and investment, the Climate and ESG Task Force will develop initiatives to proactively identify ESG-related misconduct. The task force will also coordinate the effective use of Division resources, including through the use of sophisticated data analysis to mine and assess information across registrants, to identify potential violations.

So how does streaming music score on the ESG scale? Let’s take Spotify as an example. (This post brings together several others that readers will recognize.). How bad is Spotify’s ESG competence? Seems pretty bad to me, but probably nothing that Spotify bankers at Goldman Sachs and Spotify’s never ending team of revolving door lobbyists and toadies in the Imperial City can’t get them out of with the right amount of campaign contributions.

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole or at least the streaming business that Spotify dominates. (Another 14% of market share and Spotify will hit that Herfindahl-Hirschman Index sweet spot for those keeping score at home–assuming there’s no change in the number of their competitors.)

If the Spotify decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum. They give a lot of happy talk about “net zero admissions” and their public messaging is full-on Davos as one would expect from a globalist like Daniel Ek, but streaming is their core business and streaming will only get so green. (It’s unlikely that the FAANG companies (Facebook, Apple, Amazon, Netflix and Google) will allow too much to be made out of the dirty data issue because it blows back directly on them. Neither will Senator Ron Wyden from Oregon the data center concierge–wonder why?)

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. While not as existential as Google’s streaming problems, Spotify is equally sanctimonious about how wonderful Spotify is.

It all comes down to this: The Internet in general and streaming in particular are huge electricity hogs.

Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves dancing on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? Guess who hasn’t signed up to the MCP? Any streaming service. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to because they are damn sure not signing up.

Spotify’s ESG Fail: Social

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

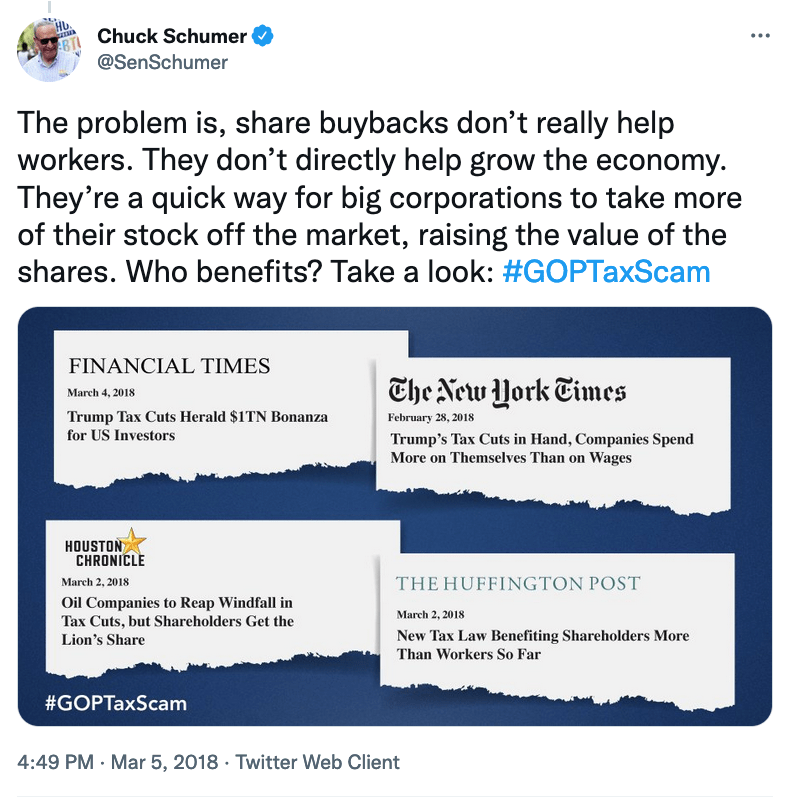

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor?

I think not.

Spotify’s ESG Fail: Governance

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

On the political side, let’s see what the company’s campaign contributions tell us:

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score.

What about the SEC investigation?

I suppose time will tell how the SEC handles its announced investigations into ESG “violations” whatever those might be (particularly in light of the SCOTUS West Virginia v. EPA holding and other “major questions” rulings recently).