The “risk free rate” is often thought of as the rate of interest paid on US government bonds. That interest rate is thought of as risk free because it is backed by the full faith and credit of the United States. Want to know where you can find that full faith and credit? Look in the mirror.

When you ask around about what collective management organizations do with their “black box” monies while they are waiting to match money with songwriters or at least copyright owners, you often hear that the money is invested in very safe instruments, like U.S. treasury bonds. This might be particularly true of CMOs that are required to pay interest on black box because that interest has to come from somewhere.

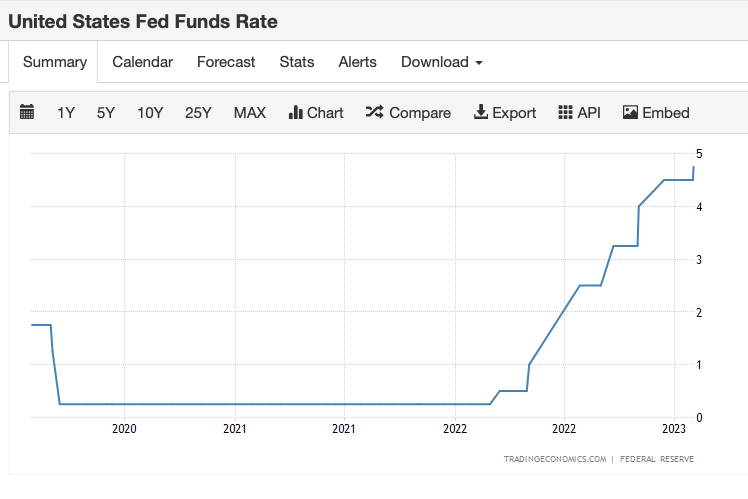

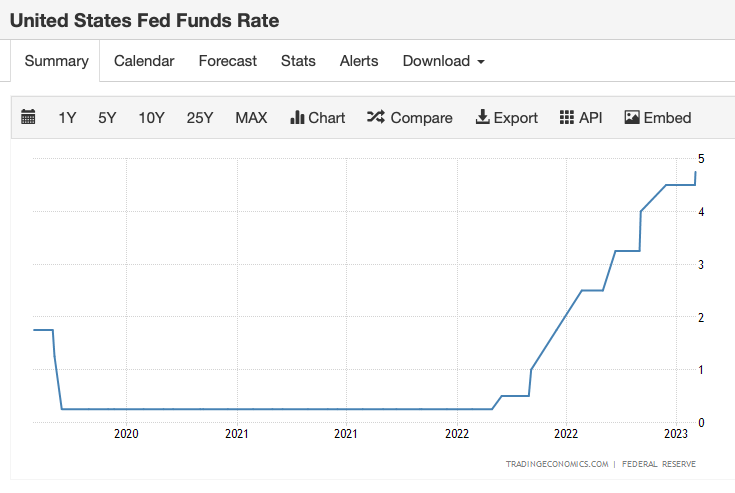

But–and here it is–but, as we have learned from the Silicon Valley Bank collapse and the number of federal government officials in the mumble tank about why these banks are failing and why they are getting bailed out by, you know, the full faith and credit of the United States, “risk free” seems to be a relative concept. When you buy US government bonds, there are a number of different maturity dates available to you, kind of like buying a certificate of deposit. A common maturity date is the 10-year bond and the two-year bond, both of which were recently down sharply.

But–there is a connection between the interest rate that the bond pays, the price of the bond, and the maturity date of that bond. When bond interest rates increase, the face price tends to decrease. So if you paid $100 for a bond with a interest rate of say .08% and that rate then increased to say 4.5%, the face price of that bond will no longer be $100, it will be less. If that increase happens fairly quickly, you can have difficulty finding a buyer. The good news is that when the Federal Reserve raises the interest rate, there is about as much news coverage of the event as it is theoretically possible to have, both before during and after the rate increase, not to mention the Federal Reserve chair testifying to Congress. It’s very public. Closely watched doesn’t really capture that level of attention.

When bond prices decline, holders only “realize” the loss or gain if they sell the bond unless the bond is marked to market so the firm has to disclose the amount of what the loss would be if they sold the bond. Hence the concept of “unrealized losses,” “maturity risk,” or “interest rate risk.” Some think that US banks currently have $620 billion in unrealized losses due to interest rate risk. And don’t forget, these are your betters. These are the smart people. These are the city fellers.

This interest rate risk issue is not limited to banks, however. It is also present anytime that an entity tasked with caring for other people’s money invests that money in treasury bonds, crypto, or whatever. You don’t have to be Wall Street Bets to end up losing your shirt or something in this environment.

So the point is that the same problem of interest rate risk and unrealized losses could apply to CMOs, such as The MLC, Inc. because of their undisclosed “investment policy” of investing the $424 million of black box they were paid by the services. They don’t disclose what the investment policy is and they don’t disclose their holdings so we don’t really know what has happened, if anything. The money could be perfectly safe.

Or not.