It’s becoming more obvious that the Mechanical Licensing Collective is not succeeding in its Congressional mandate to build the definitive music rights database so that all songwriters get paid. We often hear about MLC match rates being consistent with the “industry standard,” but this is pre-MMA thinking and is no longer relevant in a post-MMA world. (Not to mention the fact that it was these very “industry standards” that produced gigantic levels of unmatched payments that the MLC is mandated to fix.) As we will see, any match rate less than 100% is inconsistent with the MLC’s Congressional mandate which will be relevant when those in control of the MLC’s operations are reviewed by Congress in the not too distant future. Remember, The MLC, Inc. may be a private company in the traditional sense, but the MLC (different than The MLC, Inc.) is a statutory creation whose functionality is awarded to the current operators if they do a good job giving effect to the Congressional mandate. Congress can take that deal away and essentially “fire” The MLC, Inc.

It’s also becoming increasingly apparent that the Copyright Office has no stomach for its Congressionally mandated oversight role as they have been silent as the tomb so far no matter how absurd the results coming from MLC. The difference in post-MMA planning is that every royalty audit of MLC should be accompanied by a FOIA request to the Copyright Office regarding what they knew and when they knew it. Neither of those remedies were available in combination to songwriters in a pre-MMA environment. (If you took the king’s shilling and signed up for HFA you got a piece of an audit recovery of unknown providence for the most part often based on projections.)

Thankfully, due to the services paying for MLC operations as well as cost-shifting combinations of direct licensing, modified compulsory and service-supported blanket (and significant non-blanket) licensing, cost will never be a factor for The MLC, so the only consideration should be the benefit to all songwriters from getting it right.

Not everyone sees it that way. I raised this point on a Copyright Office roundtable about the MLC and was immediately jumped on by both the Head of Government Relations for Spotify and the head of the Digital Media Association (neither of whom have rendered a royalty statement in their lives in all likelihood). They rejected my position that the MMA requires that there should be no cost benefit analysis in matching–remember, the services are supposed to pay for that matching functionality as part of their deal for the MMA safe harbor giveaway.

Now I’m sure that these DIMA companies are perfectly capable of getting a match rate that’s in the limit. Just because they’ve never done it before doesn’t mean they can’t ever do it. They just need a little guidance.

Fortunately we have Congressional guidance on this issue in the legislative history of Title I of the Music Modernization Act which states:

Testimony provided by Jim Griffin at the June 10, 2014 Committee hearing highlighted the need for more robust metadata to accompany the payment and distribution of music royalties….In an era in which Americans can buy millions of products via an app on their phone based upon the UPC code on the product, the failure of the music industry to develop and maintain a master database has led to significant litigation and underpaid royalties for decades. The Committee believes that this must end so that all artists are paid for their creations and that so-called ‘‘black box’’ revenue is not a drain on the success of the entire industry.

H. Rep. 115-651 (115th Cong. 2nd Sess. April 25, 2018) at 8. (my emphasis)

I realize that the Head of Government Relations for Spotify would want to protect her employer as would the head of DIMA and immediately try to kill the idea that the MLC had to set new industry standards and that the services would pay for it. And that’s a reasonable deal in exchange for the safe harbor giveaway.

But that wasn’t the deal they made. Now you can well say that the services are not required to give a blank check, that the costs should be reasonable, and that the services have something to say about how the money is spent particularly given their expertise with supporting the world’s intelligence agencies in finding things and people, or so says Mr. Snowden. But we already see that the services got a rube deal for their tens of millions in MLC costs if the match rate is simply as bad as it was before MMA (or worse). That wasn’t their deal, either.

The deal they made was to see to it that “all artists are paid for their creations”. No qualifiers.

If you’ve tried to get a vinyl record pressed in the last few years, one thing is very obvious: There is no capacity in the current manufacturing base to accommodate all the orders–unless your name is Adele or Taylor Swift, of course. If that’s your name, as if by magic you get your vinyl orders filled and shipped on time.

Jack White spotted the vinyl trend early on–in 2009–and is filling the gap through his Third Man pressing operations. But Jack is calling on the major labels to please compete with him–rather unusual–because it’s the right thing to do in order to meet the demand for the benefit of the consumer. And the elephant in the room of this discussion is that we don’t really have any idea what the vinyl sales would be because demand is not being met by supply.

Not even close.

When a major label abandons a configuration, it’s not really abandoned. It gets outsourced to an independent and as long as there are manufacturing capacity in the system, that independent still takes orders and fulfills those orders by using that manufacturing capacity. The titles still appear in the sales book, orders get taken and returns accommodated.

Major labels also hand off vinyl manufacturing to their “special markets” divisions. For example, if you have ever tried to get vinyl manufactured in a limited run for venue sales on a major label artist (or former major label artist) you will get put through the bureaucratic torture gauntlet for the privilege of paying top dollar on a product that the label will have nothing to do with selling.

But even so, at some point that manufacturing capacity begins to shrink because the majors are getting out of the configuration and they will eventually get out of the manufacturing business altogether. And that creates a great sucking sound as capacity tanks.

I raised this problem in comments to the Copyright Royalty Board about the frozen mechanicals debacle where the smart people have tried to extend the 2006 songwriter rates on vinyl and CDs without regard to rampant inflation and simply the value of songs to sell millions of units. Why? Because vinyl and CDs don’t matter according to the lobbyists. This is, of course, bunk.

The fact is–and Jack White’s plea illuminates the issue–we don’t know what the sales would be if the capacity increased to meet demand. But we do know that sales would be higher. Probably much higher.

You do see entrepreneurs entering the space using new technology. Gold Rush Vinyl in Austin is a prime example of that phenomenon. The majors need to reconsider how to meet demand and keep the consumer happy. They also need to clean up the sales and distribution channel so that it’s easy for record stores to actually get stock, which, frankly is a joke.

Why anyone wants to substitute away from high margin physical goods to low margin streaming goods with a “rich get richer” financial model is a head scratcher. Although maybe I answered my own question.

Today, for the first time I cried during my speech, when I was asking – for only one thing – closed skies for Ukraine. #StopWarpic.twitter.com/E0X1tIC6lu

Kira Rudik is a member of the Ukrainian Parliament and a leader of one their political parties. Today she made a speech to the Henry Jackson Society in the UK asking for a no-fly zone over her country. Not the blood of our treasures on the ground, just a little American air power. And I promise you that if anyone asked for volunteers to step across a line in the sand, you’d have enough pilots to blanket the airspace from the Ukraine to the UK.

If you recall Churchill’s asks of Franklin Roosevelt before Pearl Harbor, Kira Rudik’s ask should sound familiar. That’s how we got lend/lease before America entered WWII: Roosevelt found a way to do the right thing, and his December 29, 1940 fireside chat is where we got the phrase “arsenal of democracy.” And this passage:

The Nazi masters of Germany have made it clear that they intend not only to dominate all life and thought in their own country, but also to enslave the whole of Europe, and then to use the resources of Europe to dominate the rest of the world.

But what may not be obvious to a contemporary audience is that the venue where Kira Rudik spoke is the Henry Jackson Society, named after the great American Congressman Henry “Scoop” Jackson. Scoop was a major influence in building Congressional support for the Polish Solidarity movement and a host of other freedom fighters in the Cold War.

I knew Scoop, and I can also promise you that if he were with us today there would already be a no-fly zone over Ukraine or he’d know the reason why.

If you’ve been pitched to lend your name to an NFT platform or promotion, or if you are an NFT promoter who wants to attract artists to your program, there are some issues that should get addressed. Obviously, discuss all this with your lawyers since this isn’t legal advice, but the following are some issues that you may want to consider before you commit to anything.

1. What artist rights are being granted and to whom?

2. Does grant of rights match the project summary and are license agreement, smart contract, marketplace/auction TOS and cryptocurrency rules all consistent? Has a subject matter expert been engaged to produce a report stating and certifying that the smart contract code implements the actual deal or needs to be revised?

3. What royalty is paid and to whom and when? Does artist, previous owner or charity participate in resale revenue after initial sale? Are any state or federal relevant tax rules implicated? What have you done to keep NFT revenue as far away from MLC as possible?

4. Are there exploitation or marketing restrictions on the NFT that would prevent the NFT and artist name being used in ways that are offensive to the artist, at least during the artist’s lifetime? Could heirs enforce these rights?

5. Are there any third party payments involved like producer payments, production company overrides, or any third party rights involved, re-recording restrictions. Will any letter of direction be required, e.g., for producers?

6. Are you being asked to clear publishing? If someone is telling you that they have cleared publishing, has the publisher confirmed the license and are individual songwriters actually receiving a share of revenue? The tendency is that the major publishers “settle” these kinds of cases for a lump sum and prospective royalty, which may or may not be received by individual songwriters after multiple commissions being siphoned off the top.

7. When does NFT terminate? (On resale, transfer by owner, term of years)

8. What is the governing law and venue? (And how to enforce)

10. Is artist asked to make representations, warranties and indemnity? Can the artist make such reps and warranties?

11. Is indemnity capped?

12. Are there any active disputes among anyone in the chain on the NFT promoters’ side? (“Disputes” is any disagreements, including, but not limited to, litigation or threatened litigation.) Who will cover artist’s costs of defense?

13. Is there insurance on chain of title, failure to enforce the smart contract, nonpayment, business risk?

14. Can license agreement or smart contract be revised unilaterally?

15. Is the NFT or NFT collection comprised of “generative art” or artwork created by machines, algorithms, artificial intelligence, and related technologies (i.e., potentially not capable of copyright protection)? What are implications for name and likeness rights.

16. What assurances have been given to identify purchasers of NFTs to enforce terms or prosecute breaches for first or subsequent sales?

18. Is NFT or any NFT cash flows implicated in any sanctions placed on persons related to the Russian Federation?

19. Has NFT seller or marketplace obtained legal opinion regarding whether the NFT constitutes a “security” that would require sale by a registered securities broker-dealer or other regulatory oversight?

20. Are any state securities laws, tax laws or regulations, or “doing business” laws implicated or reporting obligations triggered?

Each NFT raises its own questions, so this checklist is just a starting point.

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

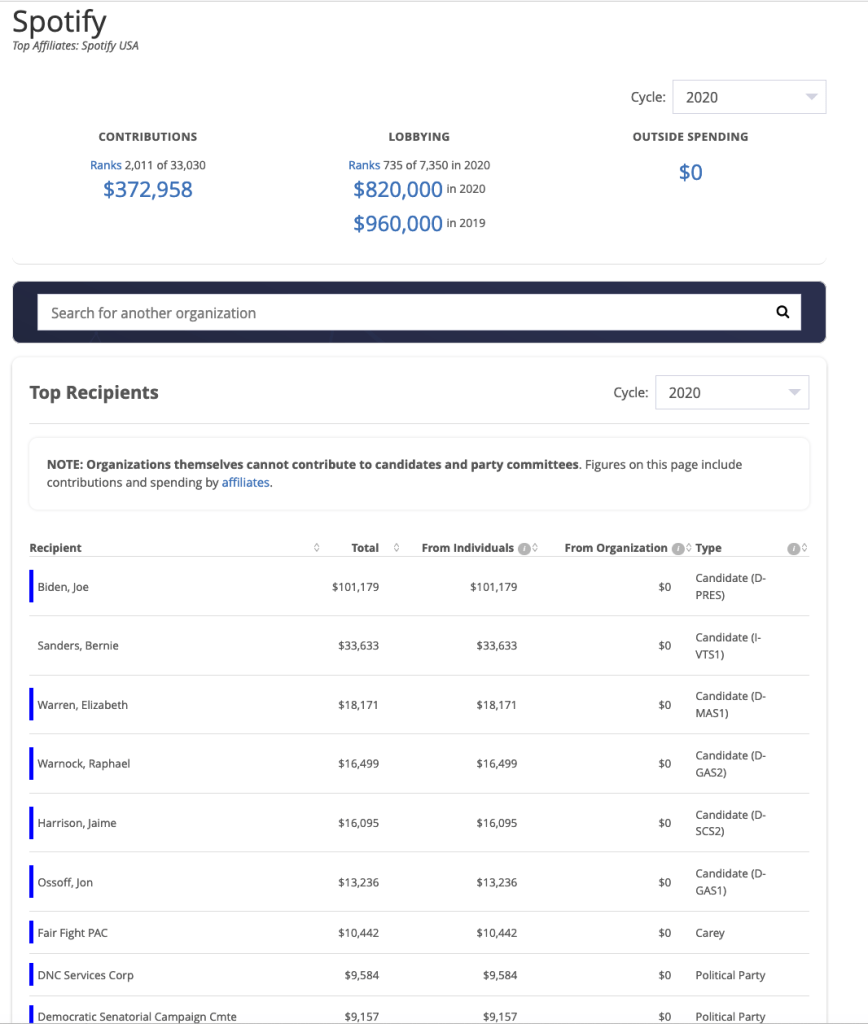

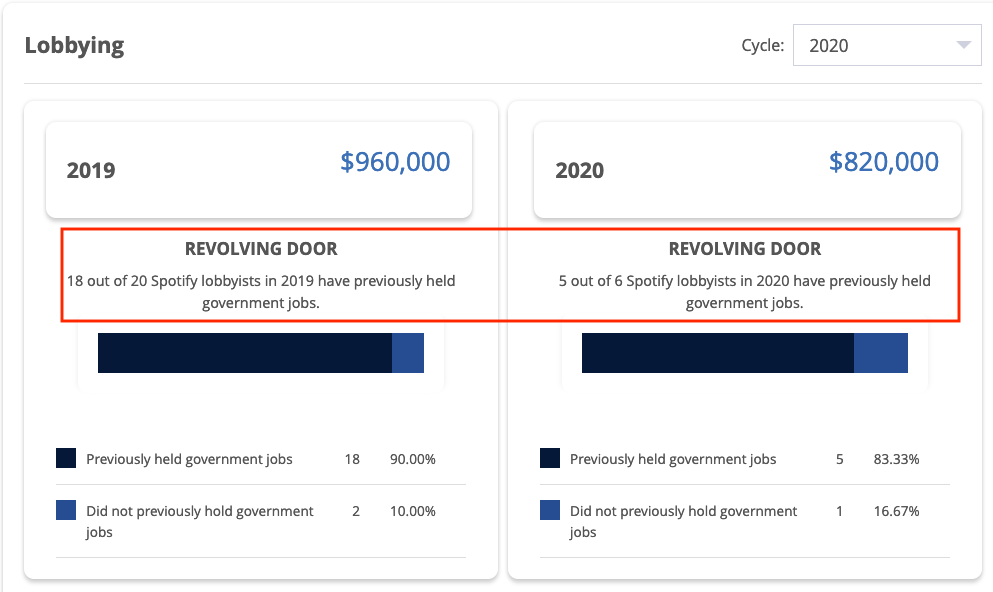

On the political side, let’s see what the company’s campaign contributions tell us:

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score.

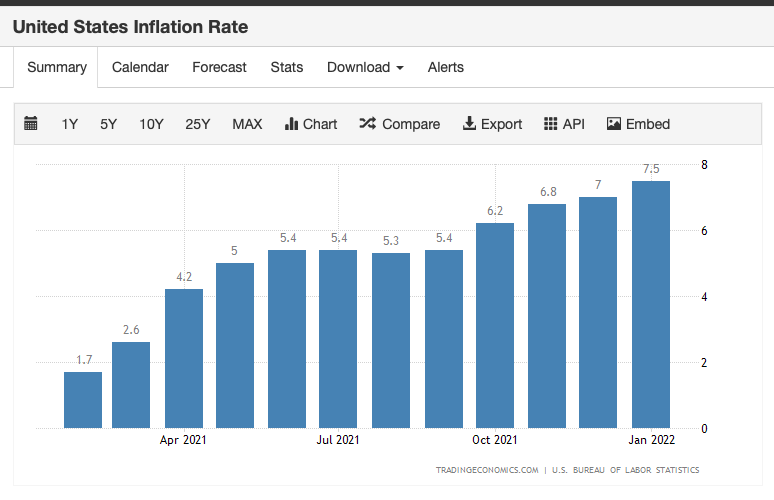

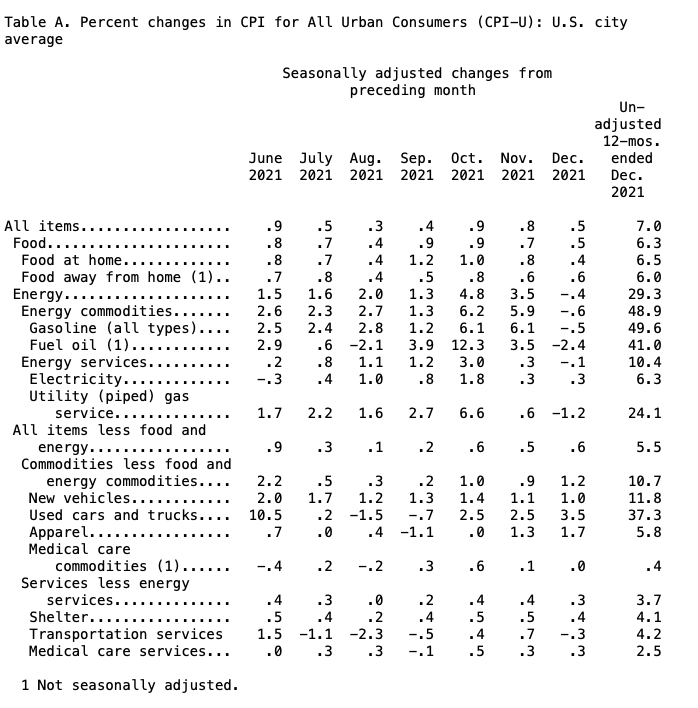

Both the consumer price index and the producer price index increased this month and the Federal Reserve is making noises like it intends to increase interest rates and reduce what is called the Fed’s “balance sheet”. Once again, the freeze on mechanical royalties for physical records like CDs and vinyl and failure to index to the consumer price index looks increasingly irresponsible if not downright antagonistic. If you agree that songwriters need to have a cost of living adjustment permanently built into all statutory rates, we have to also recognize that may be a heavy lift and needs to be supported by evidence. Here’s a few ideas.

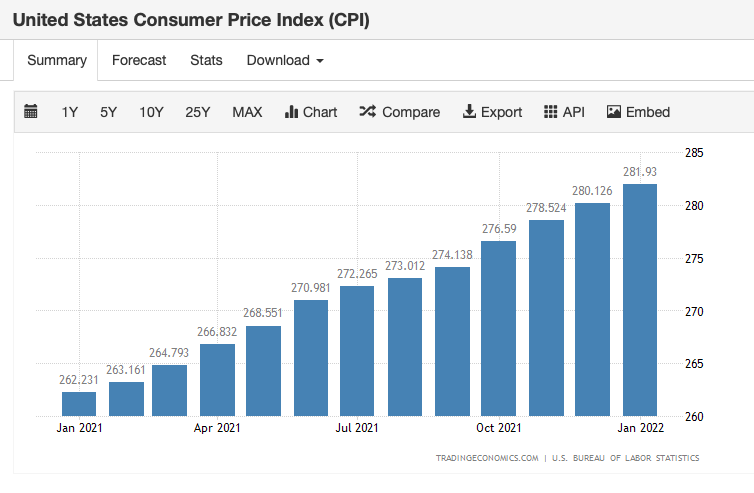

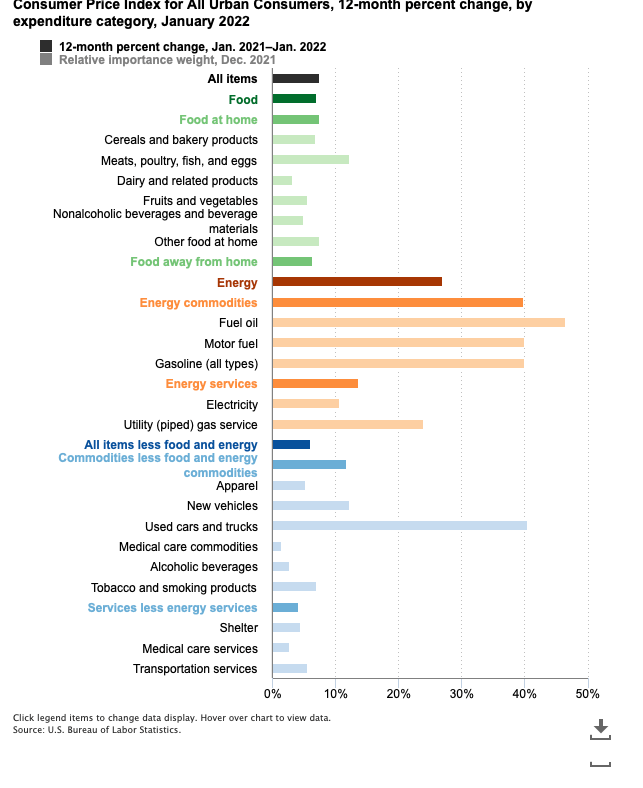

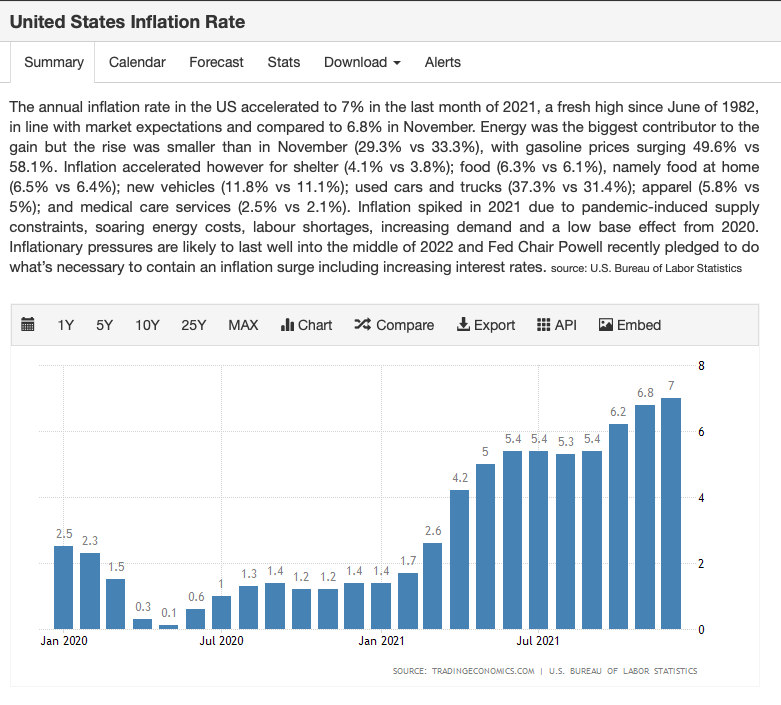

Consumer Price Index

US Inflation Rate Jan 2020-Jan 2022

The Consumer Price Index tracked a 7.5% increase in inflation, and even excluding energy and food prices the CPI rose 6% (which applies to all those who don’t drive and don’t eat).

The next chart shows increases in the categories of goods that make up the CPI.

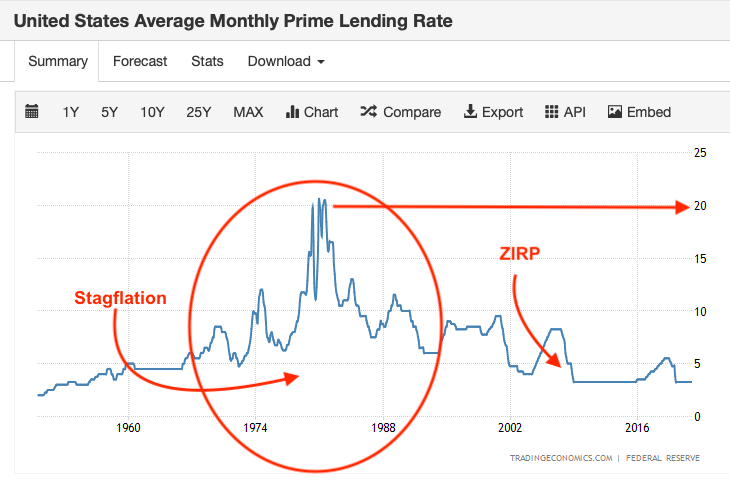

The January inflation rate is the highest since February 1982. If you don’t remember what was happening in February 1982, it was the end of the 1970s stagflation with supply side “exogenous” shocks to a number of sectors including energy. The other hallmark of the 1970s and early 1980s corresponding to the staglation is a black swan (we hope) increase in the prime rate of lending. The prime rate exceeded 20%.

One could say that the only reason that the prime rate is not much higher today is because the Federal Reserve adopted a zero interest rate policy (or “ZIRP”) in response to the 2008 financial crisis as did other central banks in other countries. The idea was that cheap money would encourage banks to make loans to borrowers as well as other banks and more debt would stimulate the economy. That’s why interest rates have been at or near zero for so long. (Not everyone thought this was a good idea, including me.) The truth is we don’t really know what interest rates would be absent the central banks’ distortion of the credit markets–perhaps for all the right reasons, but distortions nonetheless.

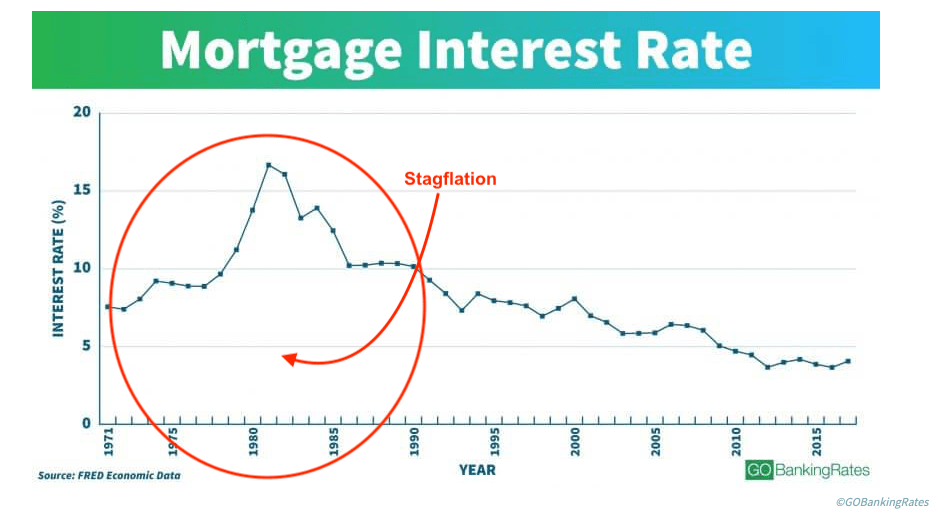

Increases in the 1970s prime rate caused all interest rates to increase, including credit card rates and mortgage rates. We are accustomed to seeing mortgage rates around 5% partly due to ZIRP, but mortgage rates were much higher in the 1970s. This caused a contraction in the number of people who could qualify for a mortgage and extremely high mortgage payments for those who could (not to mention “points” paid to compensate for the credit risk).

Remember the Federal Reserve’s mission is to use monetary policy to keep inflation under control and unemployment low. There are two policy “weapons” the Fed has to accomplish its mission: interest rates and the money supply. When the Fed adopts a ZIRP, what happens if those low rates don’t have the desired stimulus? That just leaves the money supply when zero interest rates lead to a “liquidity trap.”

With interest rates at their lower range (or “lower bound”) the Fed stimulated the money supply in a particular way called “quantitative easing” which involved increasing the money supply by creating money to buy treasury notes in a special way (not exactly printing money, but effectively similar) and also buying mortgage backed securities and other bonds in the open market. This was especially true in “busted offerings” when the government financed deficits with Treasury notes purchased by the Federal Reserve. And yes, that does sound rather hinky.

We’ll come back to that ZIRP policy and quantitative easing in another post, but let’s just say for now that the Federal Reserve provided more money to certain kinds of banks than they’d ever seen before in an effort to stimulate the economy without raising inflation. Yet they must have always known that an easy money policy was inflationary and due to ZIRP they had limited options–to kick the can down the road. Like a balloon payment in a mortgage, the devil would come for his due at some point. That time may be now.

Whenever inflation goes up, there is an assumption–fueled by those who wish to avoid blame–that inflation is just transitory and will recede if the central banks take anti-inflation steps, such as raising interest rates by targeting even higher interest rates on Federal Funds (currently 0.25%) on top of an already higher 10 Year Treasury Bond.

If the Fed raises rates by .25% five times this year as projected by banks like Goldman Sachs, that will essentially double the interest payment on government bonds which fuels both federal spending and the national debt. The problem with that is the higher interest rates proposed by the central bank also affect government borrowing to service the $30 odd trillion dollar national debt. Maybe you can withstand your credit card rate increasing by five percent, but the government cannot.

As you can see from the charts above, some of this inflation is increasing at an increasing rate. It is going to take time to recede. Energy markets are fluid, for example, but rents are not. The conventional wisdom is that mortgage rates and home prices vary inversely to each other. Mortgage rates can also have an effect on rental prices, too; the harder it is to qualify for a mortgage, the more people have to rent, so rental prices go up. Rental prices are also sticky, meaning that once they go up, they don’t decline very rapidly or at all. Ask yourself the last time a landlord cut your rent?

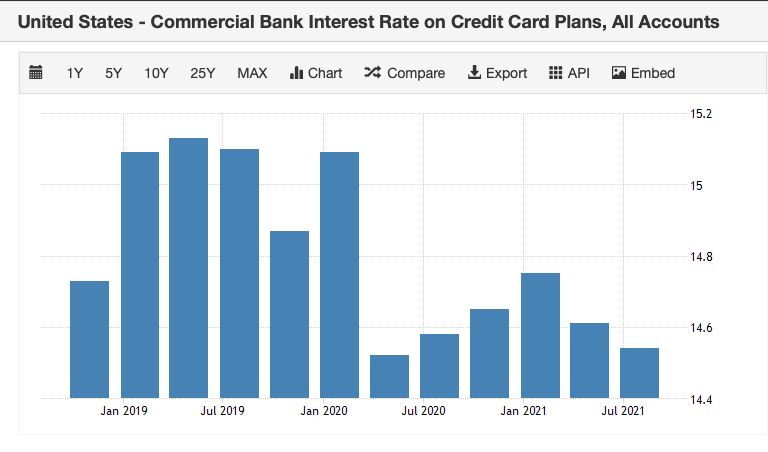

Speaking of the government’s credit card, it is important to look at the effect that inflation has on interest rates for another reason: many people have been dealing with the cost of inflation is by putting it on the credit card. Not everyone has a seven figure base salary.

Credit card interest rates are currently averaging around 14.5%, which means that if you don’t have a good credit score, you’ll probably pay closer to 20%. Bear in mind that the Federal Reserve has announced its intention to hike interest rates multiple times this year, so if that happens those in the riskier tier will be paying closer to 25% by December and people with “good” credit will be paying closer to 20%. Both of which are loan shark rates.

Bands are prone to maxing out credit cards in the best of economic times so are likely to be especially hard hit just with increased interest payments on existing balances. This multiplier effect is important because on top of everything else the cost of inflation for people who have been putting it on the credit card is going to be many times worse than it is for people who have been paying cash. This is not something that you really wanna mess with, so if there’s any possible way and I mean any possible way you can either stop making it worse or start paying down that credit card do it because this is going to get very weird.

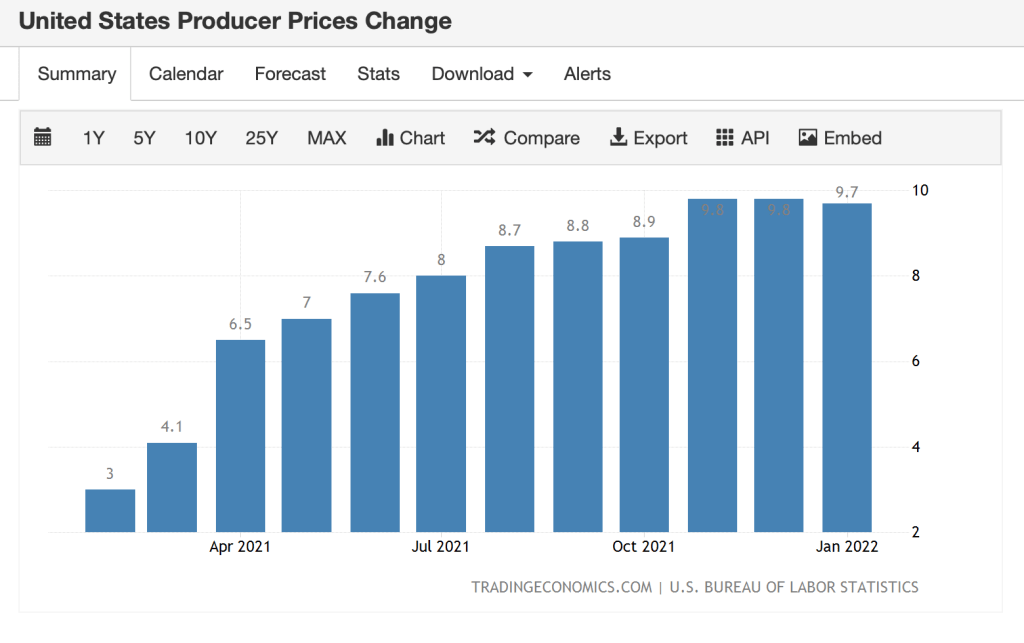

Producer Price Index

The Producer Price Index rose 1.9% in January to 9.7%. Remember, the PPI is a leading indicator of future inflation because producer prices foreshadow increases in future goods as lower priced inventories decline and price increases are in part passed through to consumers (or are in part absorbed by firms to sustain demand).

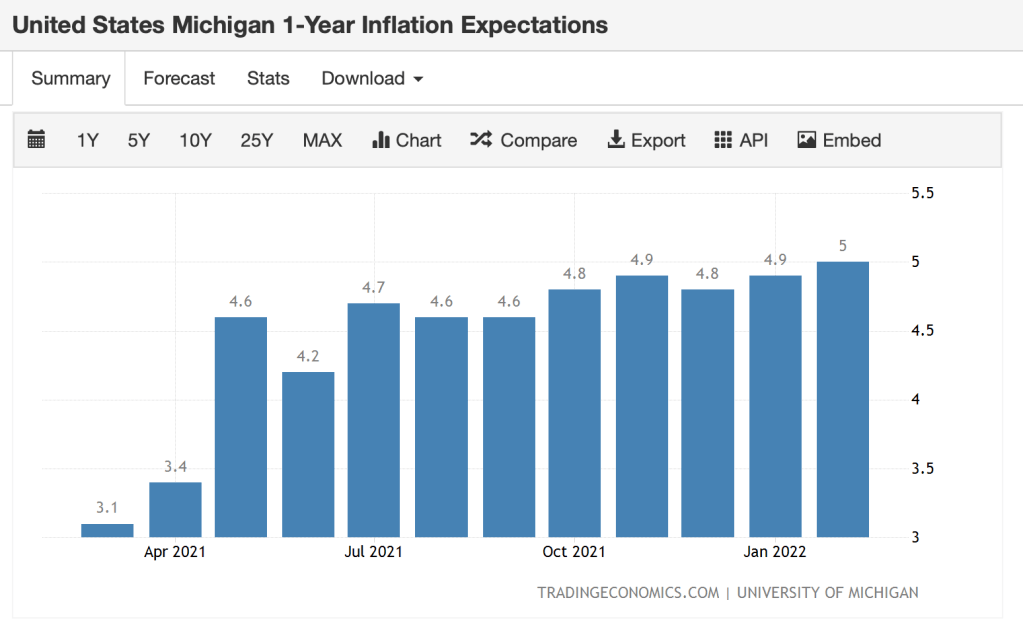

Inflation Expectations

Should songwriters expect inflation rates will effect the statutory rates in the coming years? Remember that inflation expectations can have a direct effect on actual inflation because those expectations determine wages–if you think inflation will rise, you ask for higher wages. You see this on the interactive streaming mechanical rates (which recently were amended to include a cost of living adjustment), but for some reason not on the physical.

Determining inflation expectation requires survey data, and the benchmark surveys of consumer sentiment and inflation expectations are conducted by the University of Michigan. US inflation expectations for the next 12 months rose to 5% in February of 2022 from 4.9% in January. That is the highest level of 1-year Inflation expectations since July of 2008.

Conclusion

All this confirms again that inflation for the foreseeable future is not and will not be “transitory.” Statutory rates should be indexed to inflation for the foreseeable future. This should not even be a question (and was the rule in the latter half of the 1970s, and all of 80s and 90s). If the Copyright Royalty Board will not include a cost of living adjustment in all statutory rates, perhaps it should be imposed on them.

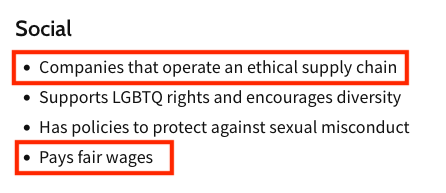

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.

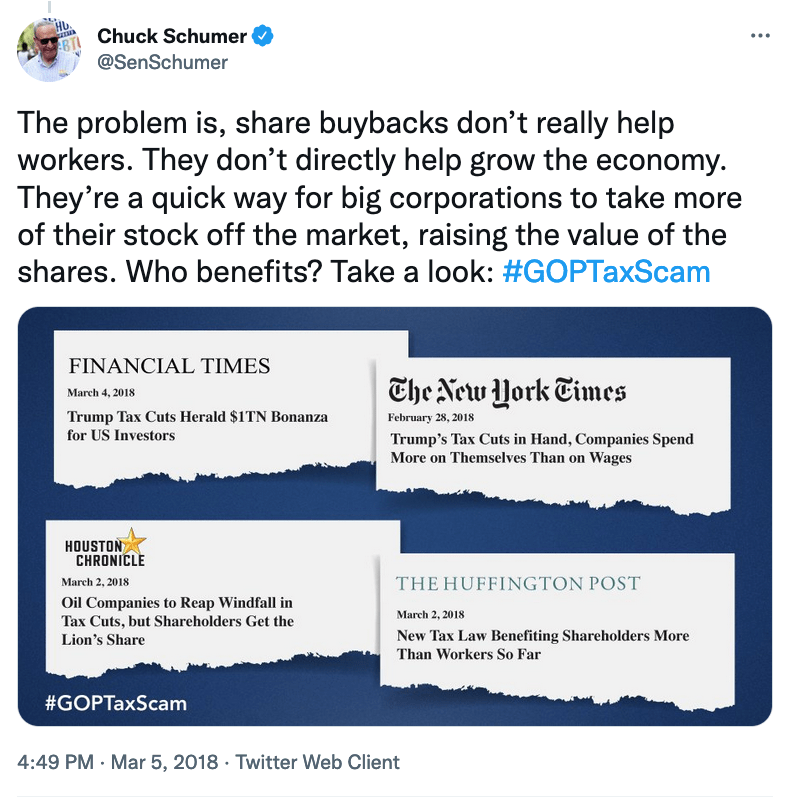

Spotify closes $24 higher than its first day of trading after destroying the incomes of thousands of artists and even more songwriters. pic.twitter.com/HeHXnEXVHh

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole. If a decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum.

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves running on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? Guess who hasn’t signed up to the MCP? Any streaming service. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to.

Next: Spotify’s “Social” Fail: Rogan, Royalties and The Uyghurs

We hear from an increasing number of songwriters who are learning about what is going on in the current rate fixing movements at the Copyright Royalty Board, some for the first time. In a nutshell, the Copyright Royalty Board rate fixing is a hugely expensive process that puts generations of children through university among the participating lawyers and lobbyists. By the time the money gets through the snake, so to speak, that process results in what are, frankly, scraps delivered to the kitchen tables of songwriters at the end of the day.

The rate fixing proceeding sets the statutory rate for certain times of song uses that are mandated by the federal government. There are two main categories of statutory rates under that compulsory mechanical license: physical (sometimes called “Subpart B” rates) typically paid by record companies, and interactive streaming (sometimes called “Subpart C” rates) typically paid by services like Spotify. (At least theoretically paid–often not judging by the size of the $424 million black box that is still just sitting under the collective’s five year plan.)

We all know that songwriters have been crushed by the failure of streaming mechanical rates to keep pace with streaming’s cannibalization of physical carriers. What many songwriters do not know is that one reason why their mechanical royalty income has dropped is due to an agreement among the major players to freeze the physical mechanical rates at the 2006 level of a minimum rate of $0.091 (currently worth approximately $0.06), and then to extend that freeze several more times for a total of 15 years so far. (The freeze essentially codified the controlled compositions rate but applied to all songwriters in the world.) There is a current proceeding at the Copyright Royalty Board in which the major players have reached an agreement to extend that 2006 freeze for another five years starting in 2023 and running to 2027. Shocking, I know.

In fact, the majors have now got themselves boxed into a corner on the interactive streaming rates that they are trying to increase. Why boxed? Obviously because the services are not stupid and if they see physical mechanical rates frozen when the record companies are paying, they ask why should the streaming rates increase when the services are paying? (And before you ask, this bid rigging is “legal” because everyone gets an antitrust exemption (17 USC §115(c)(1)(D). Cute.)

There is, of course, an unholy connection between statutory rates, controlled compositions clauses in record deals and mechanical royalties–see this post for the history. Let’s just say for this post that a page of history is worth a volume of logic.

The point I want to make to you in this post is that time is going by and no progress is being made in the current proceeding (styled “Phonorecords IV“) just like there’s no progress being made in the last proceeding (styled “Phonorecords III“); some people ask why these rates and appeals were not resolved in the giveaway that was part of Title I of the Music Modernization Act (aka the Harry Fox Preservation Act) which created the Mechanical Licensing Collective. If you’re going to make a major change to collectivize songwriters and vastly expand the scope of the compulsory mechanical license, shouldn’t you have gotten something for it? I’d count myself in the group that’s asking those questions so you know my bias. In a recent comment, I called the Copyright Royalty Board the “cornucopia of chaos,” which it is at least on the mismanaged mechanical royalty rates.

Inflation and Mechanicals

One thing that everyone should be able to agree on is that inflation is a major factor in determining any statutory royalty rate. This is certainly standard with the webcasting rates negotiated by SoundExchange with the same Copyright Royalty Board. It seems that if someone just asked for “indexing” the rates to inflation, the CRB just might give it. But no one is pushing on that open door except the songwriters and publishers who commented on the majors proposed settlement but who cannot afford to be part of the Phonorecords IV proceeding itself.

So leaving aside an increase in all of the actual rates that would reflect the value of songs, it does seem that we must accept the thinking of many economists that inflation is here to stay for a while and will surely extend into the 2023-27 rate period of Phonorecords IV. I’ve posted about these indicators before, but here’s some additional information. A cost of living adjustment seems like it should be a pro forma request–it only increases the rates if there is an actual increase in the cost of living as measured by an objective standard, typically the CPI-U (Consumer Price Index-Urban) measured by the government’s Bureau of Labor Statistics.

Since we are projecting at least two years into the future, let’s consider a few metrics that measure two years into the past. What is the trend line for inflation? Up and to the right, as they say.

US Inflation Rate

Equity Markets

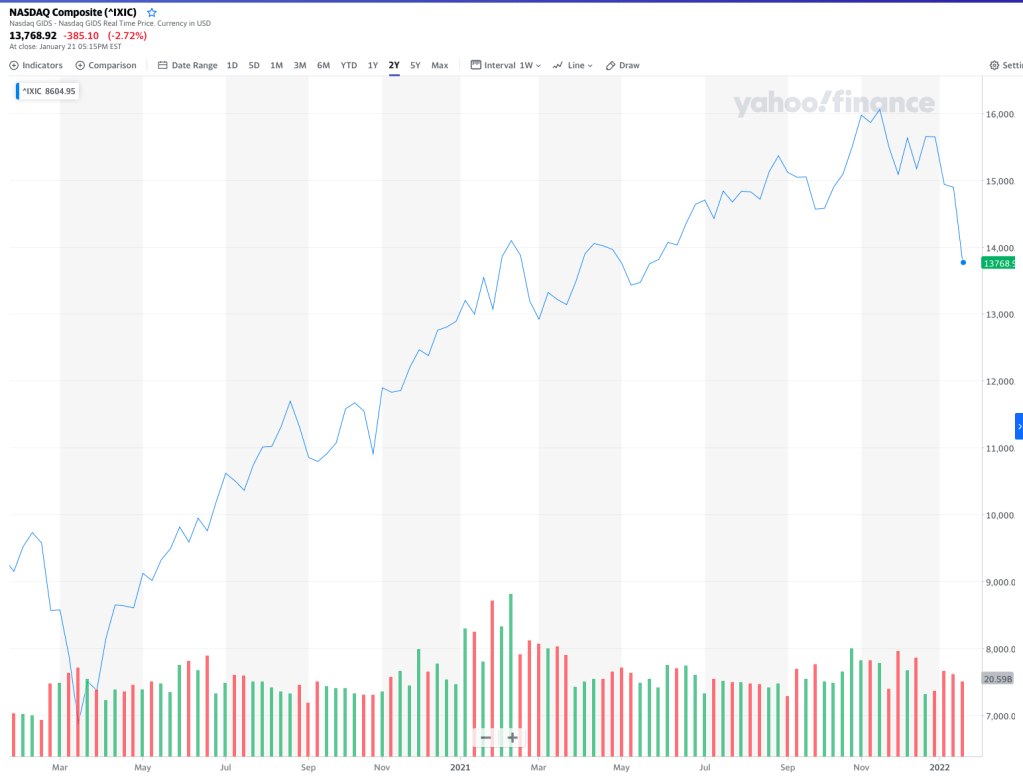

We normally don’t spill much ink on the stock market because markets go up and down, can’t pick a top and can’t pick a bottom. But–stock markets are often a leading indicator of the direction of growth in the broader economy so let’s look at what’s been happening in a few different measures. Remember–the conventional wisdom is that a 20% correction to the downside is the definition of a bear market.

I have been beating the stagflation war tocsin for quite some time now (since May 2021), and unfortunately I think the markets are waking up to the true-1970s style stagflationary environment we may be entering. This means lower growth combined with surging prices for consumers and producers. And that is truely bad news bears. (If you don’t know about 1970s stagflation, take a few minutes and read up on it. And even if you don’t, the negotiators of the statutory mechanical rates really should know. Some of them may have lived through it the first time around.)

The tech-heavy NASDAQ index has dropped about 14% since November, returning to February 2021 levels with no end in sight.

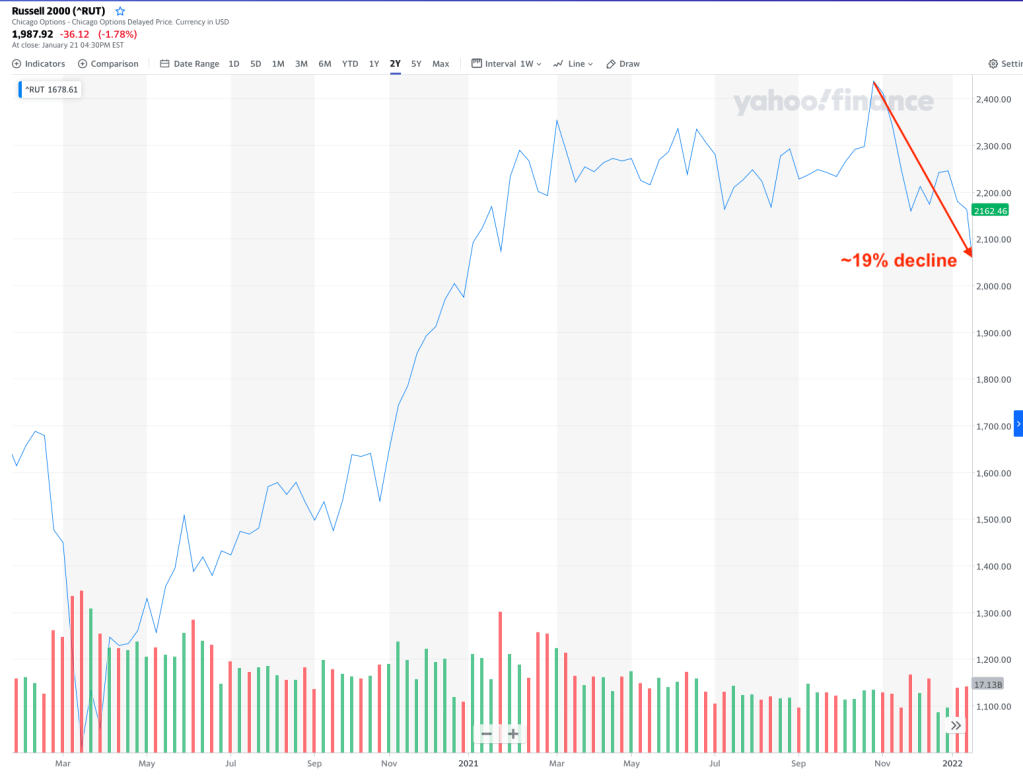

The broader Russell 2000 is more revealing with a 19% decline over a few weeks as more inflation/stagflation confirmation data comes in:

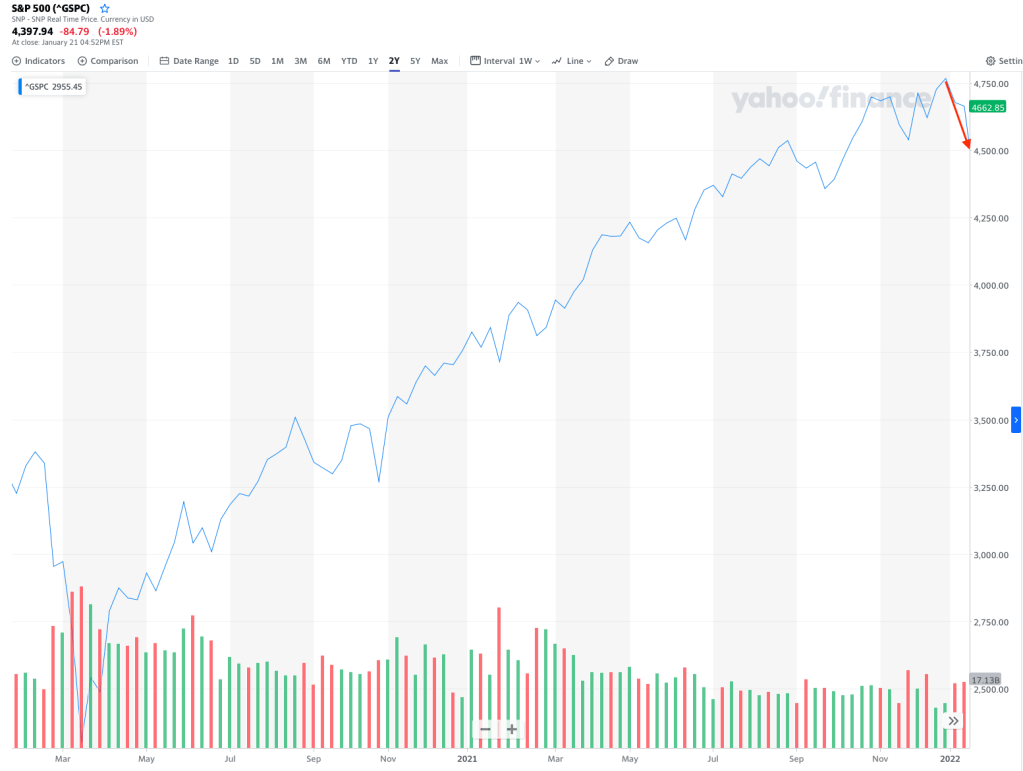

This broader decline is confirmed by the S&P 500:

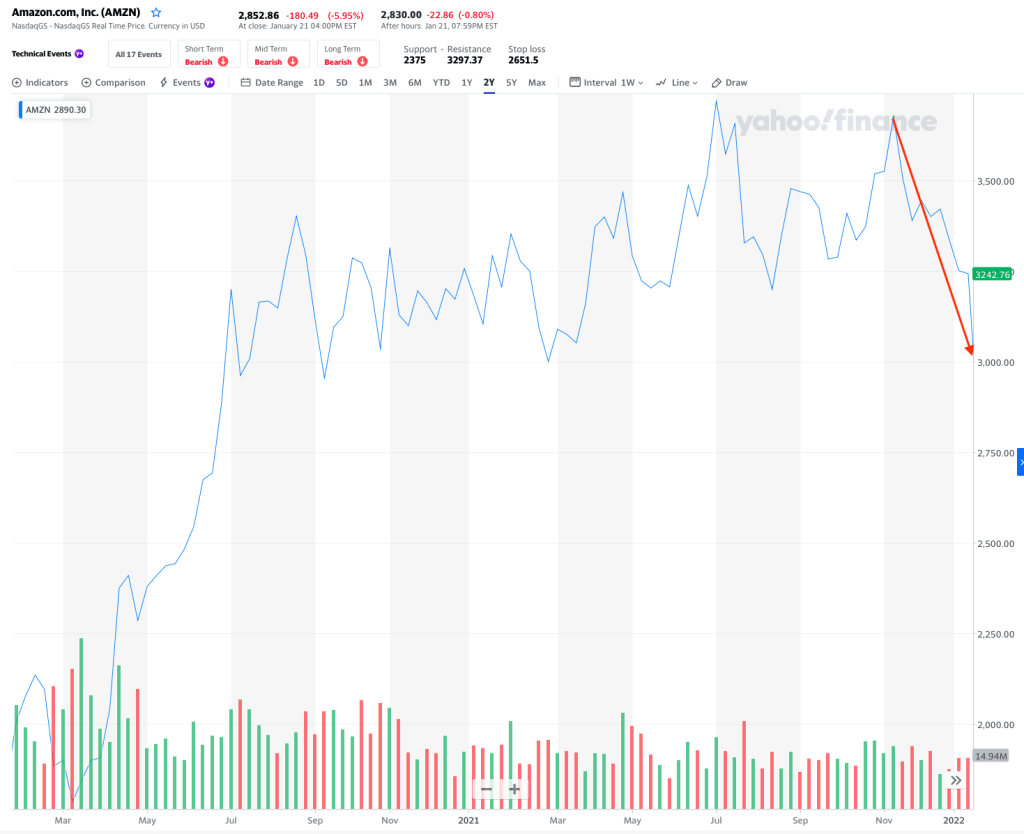

And if you were looking for confirmation of declining retail sales as a measure of growth, consider Amazon’s stock performance:

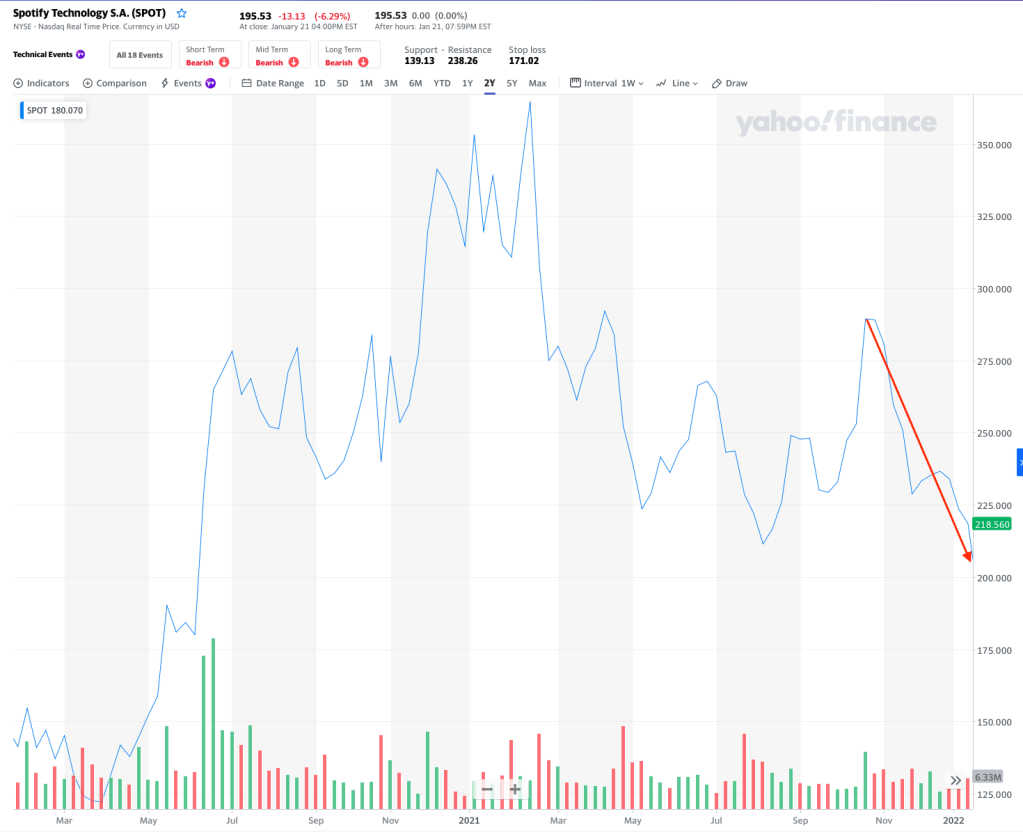

A little closer to home, consider Spotify’s recent stock performance which shows its pandemic-fueled riches coming back to reality (although not so good for any employees who got a stock option grant in the last 18 months or so):

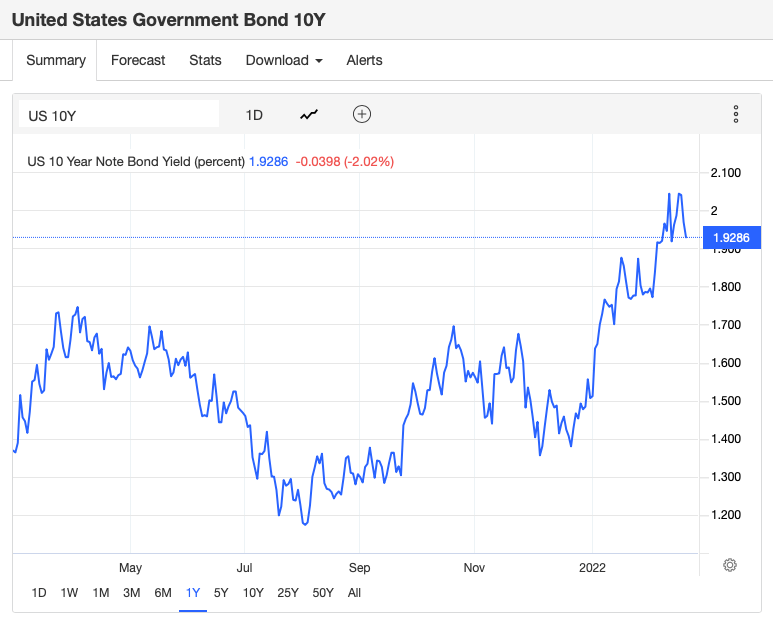

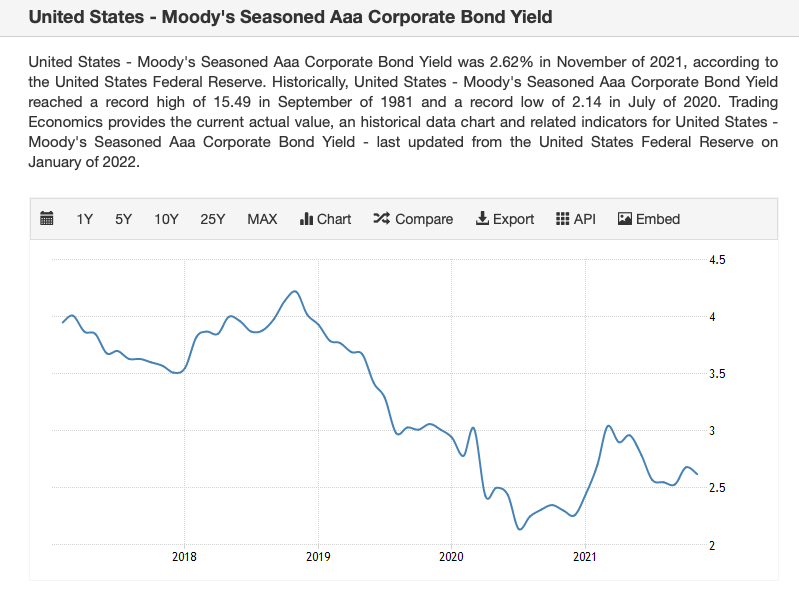

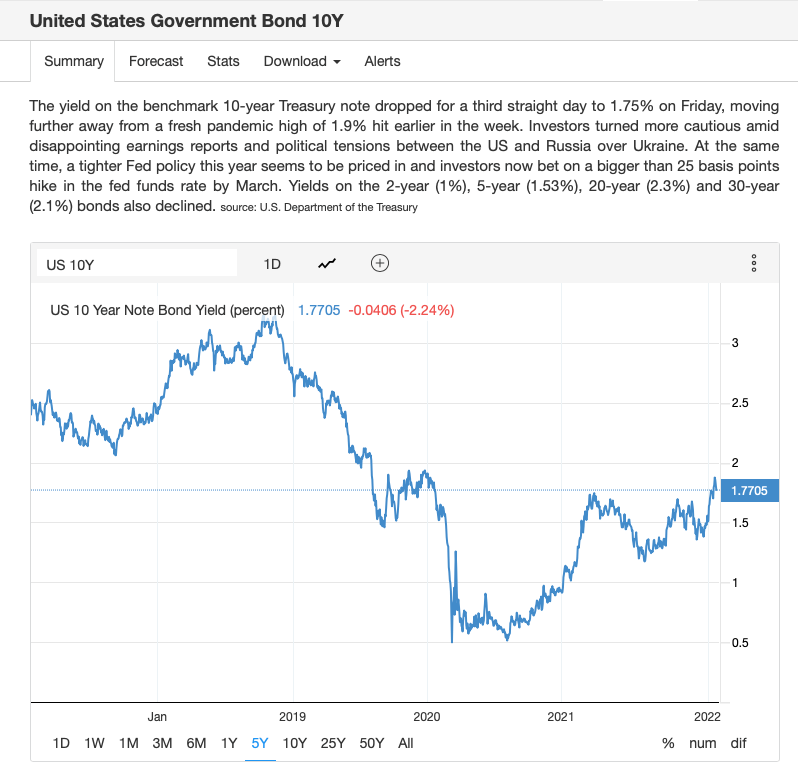

Bond Yields

Remember, the bond market is exponentially larger than the stock market. We’ll come back to this, but consider what is happening in the bond market and think about this question: what could cause both the stock market and the bond market to decline?

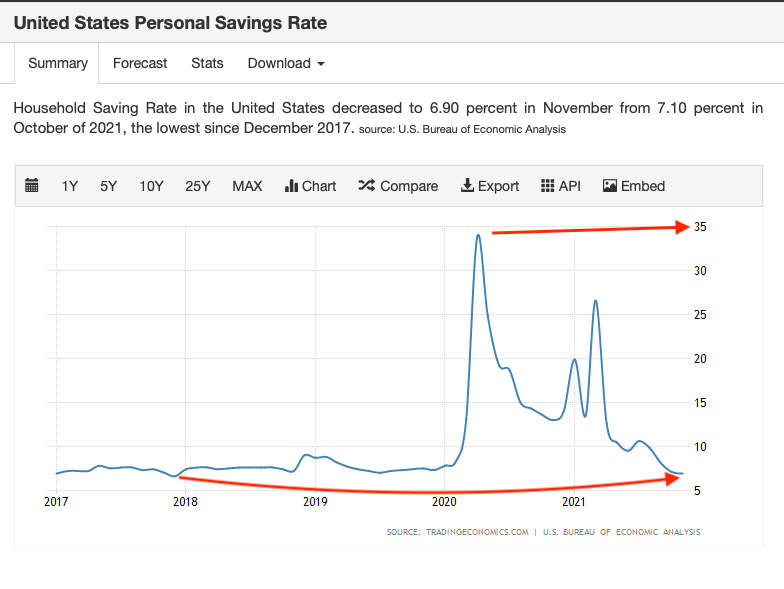

US Savings Rate

The savings rate shows a couple of anomalies where the savings rate spiked to unnatural highs of 34% in a lockdown era and again to 27% after government stimulus, but–the savings rate has sharply declined to pre-pandemic 2018-ish levels Why? I would speculate that this is partly due to rising prices of goods to consumers, particularly energy, rent and food and the decline of “real” wages (nominal wages less inflation).

Commodities

Consider a couple of inputs–there are many–but note for our purposes that these commodity prices are at or near recent highs, or are retracing recent highs. The trend line is up and to the right, which suggests that these prices are likely to continue upward into at least the first year of the Phonorecords IV rate period (2023) and potentially beyond.

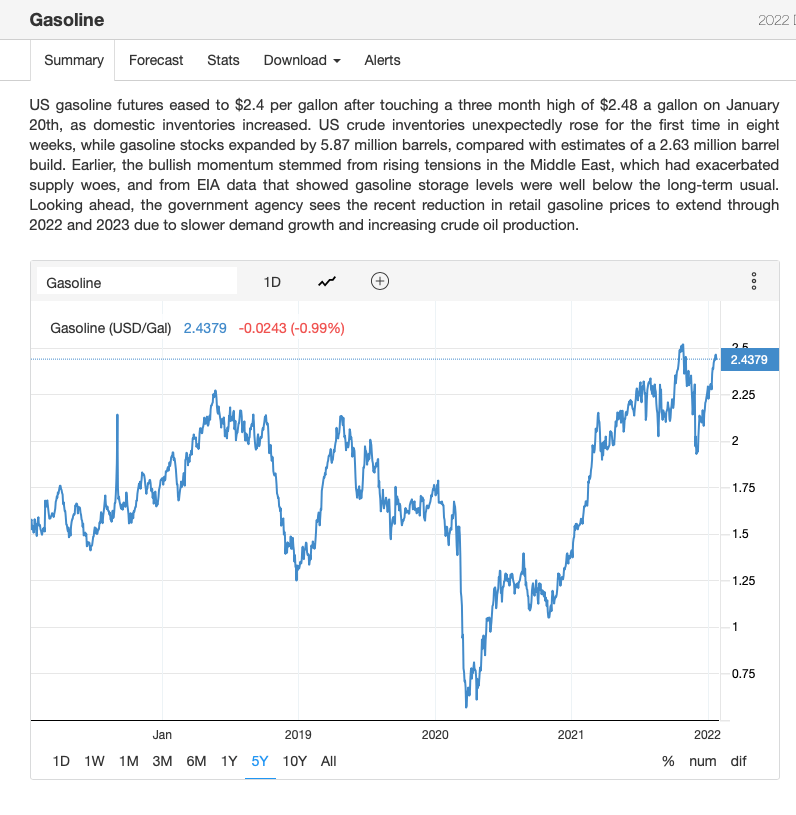

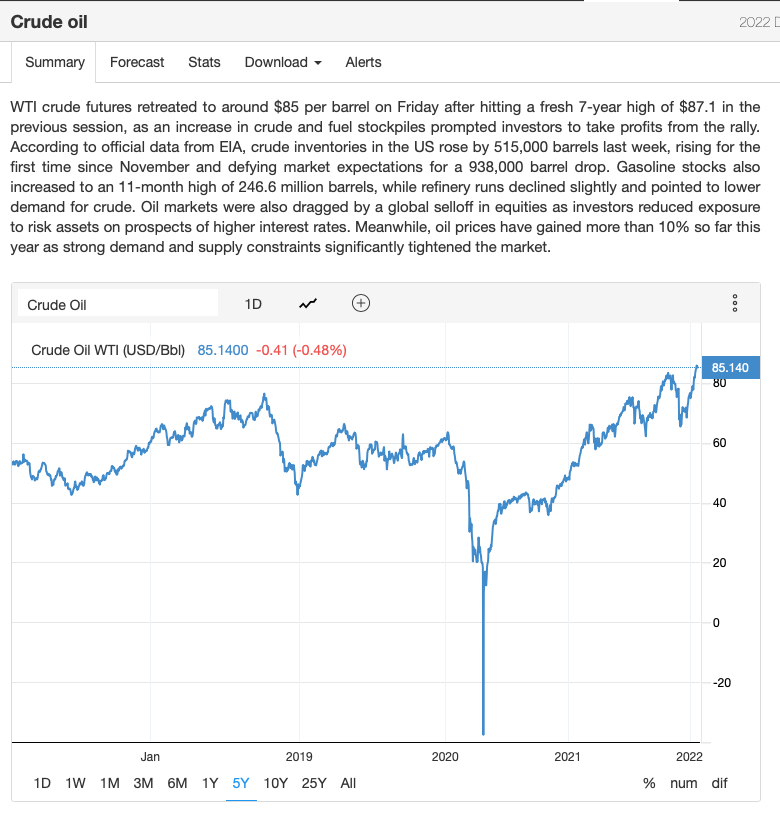

Energy

However you feel about fossil fuels, the reality for singer/songwriters or bands is that the way they try to supplement their declining songwriting income is by touring and for almost everyone, touring means gasoline. I don’t have to tell you what gasoline prices are doing–you know whenever you fill up the van. This chart is a measure of gasoline futures, which is the bet that the commodity traders are making on the future price of gasoline (not the price at the pump where you live). Again, the trend line is up and to the right.

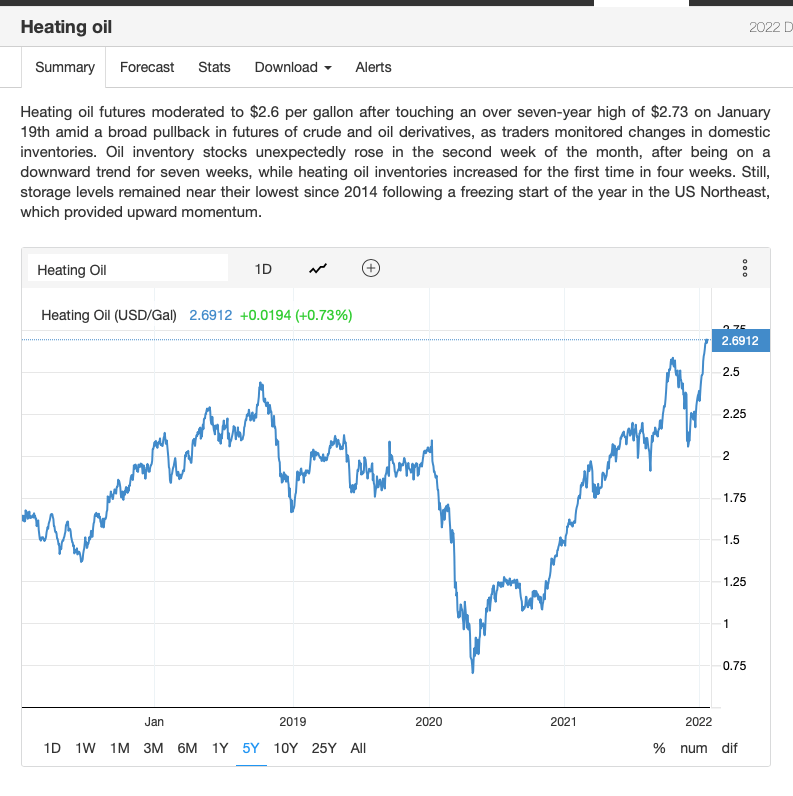

And of course if you’re going to make it to the gig or the writer room you’ll need to avoid that freezing to death thing and you’ll care about heating oil prices, up 70% year over year:

To take it a step back, crude oil is closing in on $100 a barrel due in part to exogenous supply side shocks and contractions. If crude goes over $100, we are in a whole new world that we have not seen since 2014.

Conclusion

So you get the idea, right? This is all evidence supporting a cost of living adjustment for mechanical royalties. When the stock market declines, particularly declines sharply as it is currently performing, that is largely to do an expectation of slower growth in the economy as a whole. They’ve been wrong before, but the market is actually a pretty good leading indicator of the direction of growth.

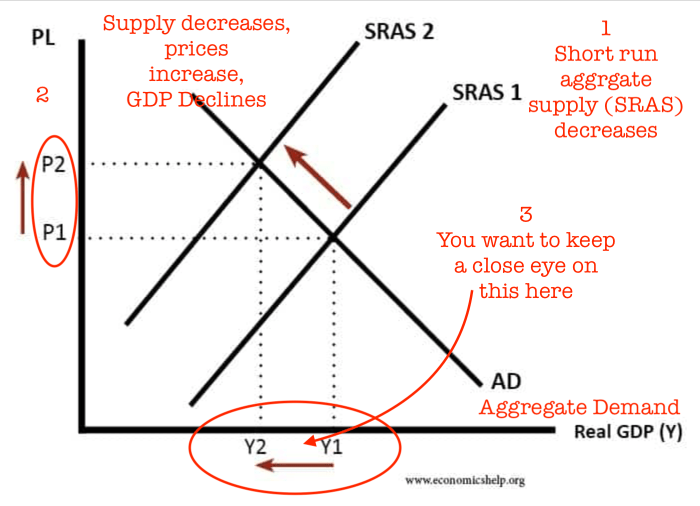

Declining stock prices foreshadow declining earnings which foreshadows declining economic growth. What happens when growth decreases? Inventories may drop, and supply declines (which is already happening and you know that if you’ve been to the grocery store lately). GDP may also decline.

Remember the stagflation three point play? In this chart, Y1 GDP declines in Y2.

Lower growth or economic stagnation is the “stag” part of stagflation.

When bond prices go down, typically interest rates are trending up, which signals an inflationary outlook. If current bond prices decline because interest rates are increasing (or are anticipated to increase), that is most likely anticipating the Federal Reserve’s announced rate increases in 2022. The number of rate increases is anticipated to be somewhere between three and five (some say even six) in 2022. The Fed increases interest rates to tamp down inflation, so you can say that lower bond prices (which vary inversely to interest rates) is anticipating the “inflation” part of 1970s-style stagflation. Just to be clear, this is all readily available public information.

It’s becoming more obvious that we are watching a slow moving train wreck (cynics like me might say we’re beginning to get hit with the balloon payment for 2008 after 15 years of quantitative easing, but that’s a story for another day). The slower the train wreck, the more likely the wreck will occur during the Phonorecords IV rate period. Since the Federal Reserve is still busily printing money, these metrics are all leading indicators of how much blood will be left on the floor starting around March 2022 or so. And we haven’t even talked about what the announced Federal Reserve rate hikes will do to the housing market even if each one is a relatively small increase.

You don’t need an expert economist to produce any original research on this for the CRB–the question for songwriters is why don’t we already have a government rate indexed to inflation? The indexed rate is only paid if you actually get an increase in the CPI, which even then only preserves the value of whatever nominal rate you do have–it’s not a “real” rate increase. So why not at least try to get a cost of living adjustment? There’s no reason not to at least try to get indexing on every statutory rate which was the standard approach on mechanicals for many years after 1978 until the 2006 freeze. Unless your bonus is tied to a big percentage increase in the headline rate rather than the less obvious indexing that would actually protect the value of songs.

Which all seems to be to be so obvious that if you don’t have it you’d have to ask yourself, do I feel lucky? The odds are all on the house.

Among the supporters of the American Music Fairness Act (AMFA) is bassist Ken Casey, member of Local 9-535 (Boston, MA) and longtime frontman of the Celtic punk band the Dropkick Murphys. Photo: Ken Susi

On June 24 of last year, a group of legislators and musicians gathered on Capitol Hill to introduce the American Music Fairness Act (AMFA). The AFM and the MusicFIRST Coalition worked closely with members of Congress to help craft the AMFA. If adopted, the bipartisan bill will establish a performance right for sound recordings, ensuring that all of the performers, musicians, and others involved in the creation of a recording will receive fair compensation for its broadcast on AM/FM radio. Among the supporters was bassist Ken Casey, member of Local 9-535 (Boston, MA) and longtime frontman of the Celtic punk band the Dropkick Murphys. It was hardly the first time Casey has lent his voice to a cause.

Together for more than 25 years, the Dropkick Murphys originated in 1996 when Casey, then a bartender at Symphony Hall in Boston, accepted a bet from a co-worker. He’d never played an instrument before, but he vowed he could win the bet by starting a band, and soon they were rehearsing in the basement of a nearby barbershop.

Despite the hundreds of billions of dollars large media corporations like iHeartRadio make from advertisers, they never share a penny of that with the musicians who create the music. Musicians deserve compensation for work—just like everyone else. Sign the American Music Fairness Act petition, visit https://bit.ly/AMFA-fairpay