[This is an extension of Spotify’s ESG Fail: Environment]

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

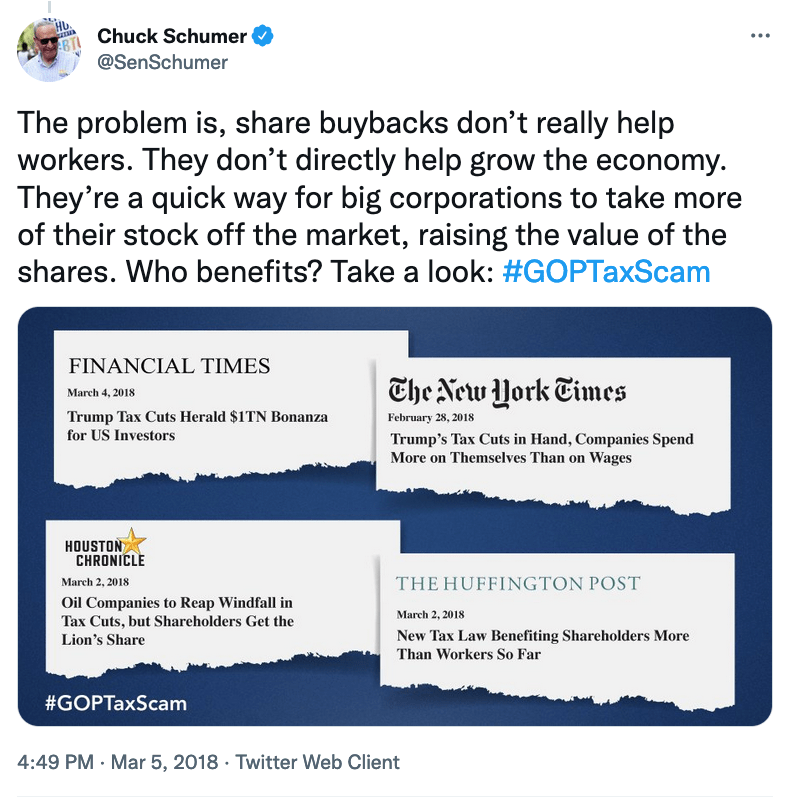

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

Vox’s Matt Yglesias sums it up nicely:

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.