Speculative ticketing is the practice of selling an option to maybe buy a popular ticket (often at an insane price) before the ticket goes on sale. You may not realize you are not buying a real ticket, although these tickets often come with fine print, and as Tom Waits tells us, the large print giveth and the small print taketh away.

There is an effort going on to specifically ban speculative ticketing at the state level which I applaud as I think speculative ticketing should be a crime. One reason I think this is because I think it already is a crime in most if not all states and possibly under federal law as well.

Think about it–do you think that if you before Blackstone and said to Sir William, My Lord, the defendant sold me a famous cow he didn’t own at a price he invented and promised to deliver the cow on law day. He took my money but delivered no cow (or delivered a different and unfamous cow). And the defendant said, perfectly legal My Lord.

What do you think My Lord Blackstone would say?

What would Billy do?

I don’t think the English common law would have just let the defendant walk out without at least compensating the buyer. Therefore, there’s probably a case that can be made out of existing law for selling stolen or counterfeit goods, or a host of other common law derivatives that would violate the charter of the land.

So as we try to get specific legal action to deal with speculative tickets, let’s not allow the lobbyists for Stubhub to negotiate the punishment that they want rather than the punishment that already applies under existing state civil or criminal law.

Ek’s New Iconography: Will the real Daniel Ek please stand up?

MTP readers will no doubt remember when Daniel Ek refused to be deposed in the latest Nashville case against Spotify for copyright infringement (Eight Mile Style). He eventually was deposed where he tried to say that he had no first hand knowledge of the facts or publishing practices at Spotify. Others did that for him after they got finished peeling his pears.

Ryan Hogg, writing in Fortune, published what I can only think is a puff piece on Ek trying to pass him off as a man of the people with a management style of just one of the team. Worth over a billion dollars and controlling voting stock.

And then there’s this:

What is Spotify’s contractual basis for their modernized free goods program?

There’s been a lot of discussion about Spotify’s new “modernized” free goods program aka Track Monetization Eligibility. It does raise the question of how they are getting away with this. Free goods, after all, were based on contract terms that the artist got to negotiate (and which, by the way, was passed along to songwriters through the artist’s controlled compositions clause for anyone not on a pure statutory rate and still is.

Who agreed to this? And why aren’t they stepping forward to claim their genius?

Spotify has announced they are “Modernizing Our Royalty System.” Beware of geeks bearing “modernization”–that almost always means they get what they want to your disadvantage. Also sounds like yet another safe harbor. At a minimum, they are demonstrating the usual lack of understanding of the delicate balance of the music business they now control. But if they can convince you not to object, then they get away with it.

Don’t let them.

An Attack on Property Rights

There’s some serious questions about whether Spotify has the right to unilaterally change the way it counts royalty-bearing streams and to encroach on the private property rights of artists.

Here’s their plan: Evidently the plan is to only pay on streams over 1,000 per song accruing during the previous 12 months. I seriously doubt that they can engage in this terribly modern “stream discrimination” in a way that doesn’t breach any negotiated direct license with a minimum guarantee (if not others).

That doubt also leads me to think that Spotify’s unilateral change in “royalty policy” (whatever that is) is unlikely to affect everyone the same. Taking a page from 1984newspeakers, Spotify calls this discrimination policy “Track Monetization Eligibility”. It’s not discrimination, you see, it’s “eligibility”, a whole new thing. Kind of like war is peace, right? Or bouillabaisse.

According to Spotify’s own announcement this proposed change is not an increase in the total royalty pool that Spotify pays out (God forbid the famous “pie” should actually grow): ”There is no change to the size of the music royalty pool being paid out to rights holders from Spotify; we will simply use the tens of millions of dollars annually [of your money] to increase the payments to all eligible tracks, rather than spreading it out into $0.03 payments [that we currently owe you].”

Yep, you won’t even miss it, and you should sacrifice for all those deserving artists who are more eligible than you. They are not growing the pie, they are shifting money around–rearranging the deck chairs.

Spotify’s Need for Living Space

So why is Spotify doing this to you? The simple answer is the same reason monopolists always use: they need living space for Greater Spotify. Or more simply, because they can, or they can try. They’ll tell you it’s to address “streaming fraud” but there are a lot more direct ways to address streaming fraud such as establishing a simple “know your vendor” policy, or a simple pruning policy similar to that established by record companies to cut out low-sellers (excluding classical and instrumental jazz). But that would require Spotify to get real about their growth rates and be honest with their shareholders and partners. Based on the way Spotify treated the country of Uruguay, they are more interested in espoliating a country’s cultural resources than they are in fairly compensating musicians.

Of course, they won’t tell you that side of the story. They won’t even tell you if certain genres or languages will be more impacted than others (like the way labels protected classical and instrumental jazz from getting cut out measured by pop standards). Here’s their explanation:

It’s more impactful [says who?] for these tens of millions of dollars per year to increase payments to those most dependent on streaming revenue — rather than being spread out in tiny payments that typically don’t even reach an artist (as they do not surpass distributors’ minimum payout thresholds). 99.5% of all streams are of tracks that have at least 1,000 annual streams, and each of those tracks will earn more under this policy.

This reference to “minimum payout thresholds” is a very Spotifyesque twisting of a generalization wrapped in cross reference inside of spin. Because of the tiny sums Spotify pays artists due to the insane “big pool” or “market centric” royalty model that made Spotify rich, extremely low royalties make payment a challenge.

Plus, if they want to make allegations about third party distributors, they should say which distributors they are speaking of and cite directly to specific terms and conditions of those services. We can’t ask these anonymous distributors about their policies if we don’t know who they are.

What’s more likely is that tech platforms like PayPal stack up transaction fees to make the payment cost more than the royalty paid. Of course, you could probably say that about all streaming if you calculate the cost of accounting on a per stream basis, but that’s a different conversation.

So Spotify wants you to ignore the fact that they impose this “market centric” royalty rate that pays you bupkis in the first place. Since your distributor holds the tiny slivers of money anyway, Spotify just won’t pay you at all. It’s all the same to you, right? You weren’t getting paid anyway, so Spotify will just give your money to these other artists who didn’t ask for it and probably wouldn’t want it if you asked them.

There is a narrative going around that somehow the major labels are behind this. I seriously doubt it–if they ever got caught with their fingers in the cookie jar on this scam, would it be worth the pittance that they will end up getting in pocket after all mouths are fed? The scam is also 180 out from Lucian Grange’s call for artist centric royalty rates, so as a matter of policy it’s inconsistent with at least Universal’s stated goals. So I’d be careful about buying into that theory without some proof.

What About Mechanical Royalties?

What’s interesting about this scam is that switching to Spotify’s obligations on the song side, the accounting rules for mechanical royalties say (37 CFR § 210.6(g)(6) for those reading along at home) seem to contradict the very suckers deal that Spotify is cramming down on the recording side:

Royalties under 17 U.S.C. 115 shall not be considered payable, and no Monthly Statement of Account shall be required, until the compulsory licensee’s [i.e., Spotify’s] cumulative unpaid royalties for the copyright owner equal at least one cent. Moreover, in any case in which the cumulative unpaid royalties under 17 U.S.C. 115 that would otherwise be payable by the compulsory licensee to the copyright owner are less than $5, and the copyright owner has not notified the compulsory licensee in writing that it wishes to receive Monthly Statements of Account reflecting payments of less than $5, the compulsory licensee may choose to defer the payment date for such royalties and provide no Monthly Statements of Account until the earlier of the time for rendering the Monthly Statement of Account for the month in which the compulsory licensee’s cumulative unpaid royalties under section 17 U.S.C. 115 for the copyright owner exceed $5 or the time for rendering the Annual Statement of Account, at which time the compulsory licensee may provide one statement and payment covering the entire period for which royalty payments were deferred.

Much has been made of the fact that Spotify may think it can unilaterally change its obligations to pay sound recording royalties, but they still have to pay mechanicals because of the statute. And when they pay mechanicals, the accounting rules have some pretty low thresholds that require them to pay small amounts. This seems to be the very issue they are criticizing with their proposed change in “royalty policy.”

But remember that the only reason that Spotify has to pay mechanical royalties on the stream discrimination is because they haven’t managed to get that free ride inserted into the mechanical royalty rates alongside all the other safe harbors and goodies they seem to have bought for their payment of historical black box.

So I would expect that Spotify will show up at the Copyright Royalty Board for Phonorecords V and insist on a safe harbor to enshrine stream discrimination into the Rube Goldberg streaming mechanical royalty rates. After all, controlled compositions are only paid on royalty bearing sales, right? And since it seems like they get everything else they want, everyone will roll over and give this to them, too. Then the statutory mechanical will give them protection.

To Each According to Their Needs

Personally, I have an issue with any exception that results in any artist being forced to accept a royalty free deal. Plus, it seems like what should be happening here is that underperforming tracks get dropped, but that doesn’t support the narrative that all the world’s music is on offer. Just not paid for.

Is it a lot of money to any one person? Not really, but it’s obviously enough money to make the exercise worthwhile to Spotify. And notice that they haven’t really told you how much money is involved. It may be that Spotify isn’t holding back any small payments from distributors if all payments are aggregated. But either way it does seem like this new new thing should start with a clean slate–and all accrued royalties should be paid.

This idea that you should be forced to give up any income at all for the greater good of someone else is kind of an odd way of thinking. Or as they say back in the home country, from each according to their ability and to each according to their needs. And you don’t really need the money, do you?

By the way, can you break a $20?

The NO AI Fraud Act

Thanks to U.S. Representatives Salazar and Dean, there’s an effort underway to limit Big Tech’s AI rampage just in time for Davos. (Remember, the AI bubble got started at last year’s World Economic Forum Winter Games in Davos, Switzerland).

Chairman Issa Questions MLC’s Secretive Investment Policyfor Hundreds of Millions in Black Box

As we’ve noted a few times, the MLC has a nontransparent–some might say “secretive”–investment policy that has the effect of a government rule. This has caught the attention of Chairman Darrell Issa and Rep. Ben Cline at a recent House oversight hearing. Chairman Issa asked for more information about the investment policy in follow-up “questions for the record” directed to MLC CEO Kris Ahrend. It’s worth getting smart about what the MLC is up to in advance of the upcoming “redesignation” proceeding at the Copyright Office. We all know the decision is cooked and scammed already as part of the Harry Fox Preservation Act (AKA Title I of the MMA), but it will be interesting to see if anyone actually cares and the investment policy is a perfect example. It will also be interesting to see which Copyright Office examiner goes to work for one of the DiMA companies after the redesignation as is their tradition.

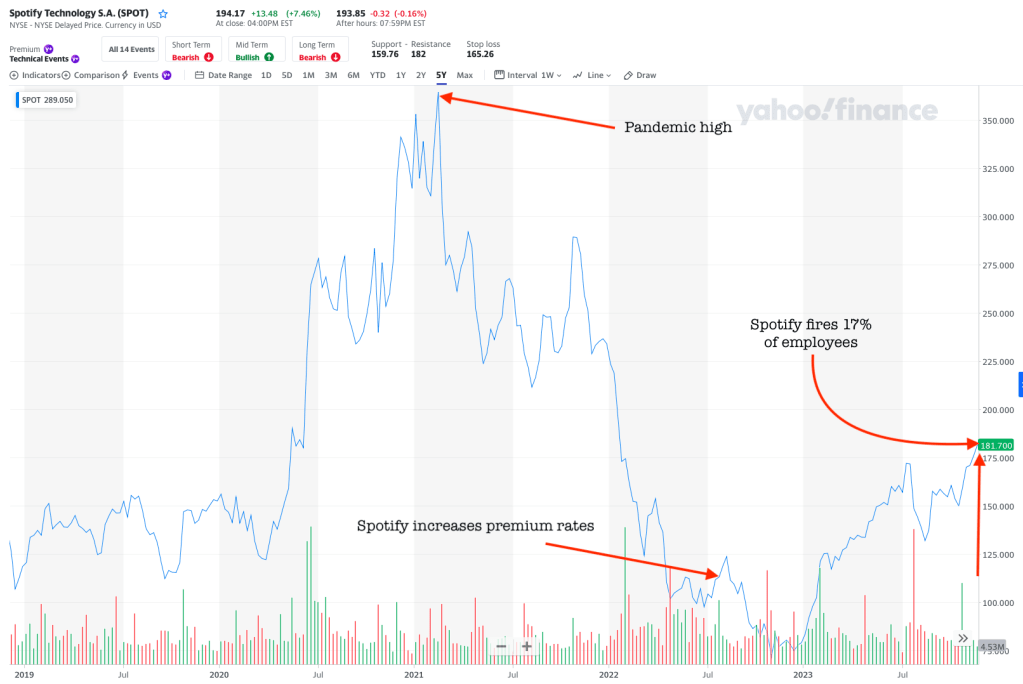

Harsh? Not really, at least not from a share price point of view. Spotify’s all time highest share price was during the COVID pandemic.

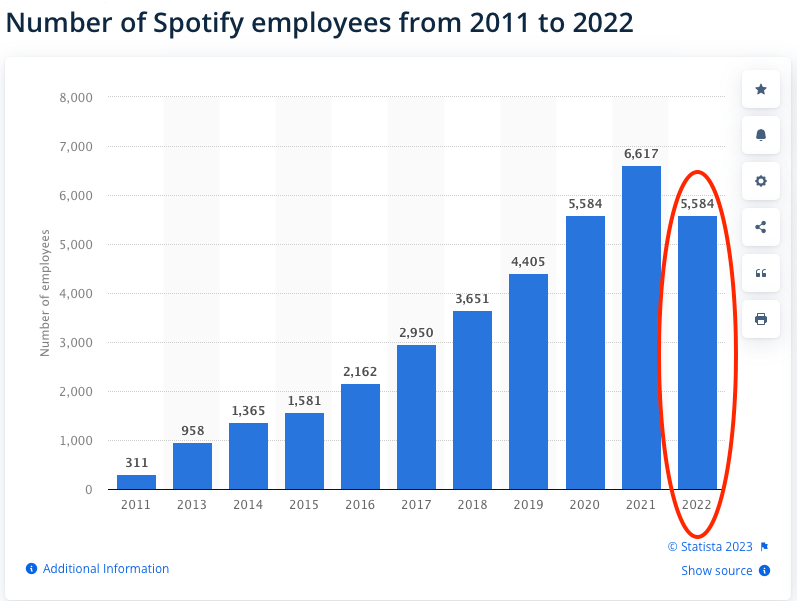

Spotify CEO Daniel Ek and the press tells us that Spotify is cutting 1,500 jobs which works out to about 17% of Spotify employees. Which works out to a pre-layoff workforce of 8,823. So let’s start there—that workforce number seems very high and is completely out of line with some recent data from Statista which is usually reliable.

If Statista is correct, Spotify employed 5,584 as of last year. Yet somehow Spotify’s 2023 workforce grew to 9200 according to the Guardian, fully 2/3 over that 2022 level without a commensurate and offsetting growth in revenue. That’s a governance question in and of itself.

Why the layoffs? The Guardian reports that Spotify CEO Daniel Ek is concerned about costs. He says “Despite our efforts to reduce costs this past year, our cost structure for where we need to be is too big.” Maybe I missed it, but the only time I can recall Daniel Ek being vocally concerned about Spotify’s operating costs was when it came to paying royalties. Then it was full-blown poor mouthing while signing leases for very expensive office space in 4 World Trade Center as well as other pricy real estate, executive compensation and podcasters like Harry & Meghan.

Over the last two years, we’ve put significant emphasis on building Spotify into a truly great and sustainable business – one designed to achieve our goal of being the world’s leading audio company and one that will consistently drive profitability and growth into the future. While we’ve made worthy strides, as I’ve shared many times, we still have work to do. Economic growth has slowed dramatically and capital has become more expensive. Spotify is not an exception to these realities.

Which “economic growth” is that?

But, he is definitely right about capital costs.

Still, Spotify’s job cuts are not necessarily that surprising considering the macro economy, most specifically rents and interest rates. As recently as 2018, Spotify was the second largest tenant at 4 WTC. Considering the sheer size of Spotify’s New York office space, it’s not surprising that Spotify is now sublettingfive floors of 4 WTC earlier this year. That’s right, the company had a spare five floors. Can that excess just be more people working at home given Mr. Ek’s decision to expand Spotify’s workforce? But why does Spotify need to be a major tenant in World Trade Center in the first place? Renting the big New York office space is the corporate equivalent of playing house. That’s an expensive game of pretend.

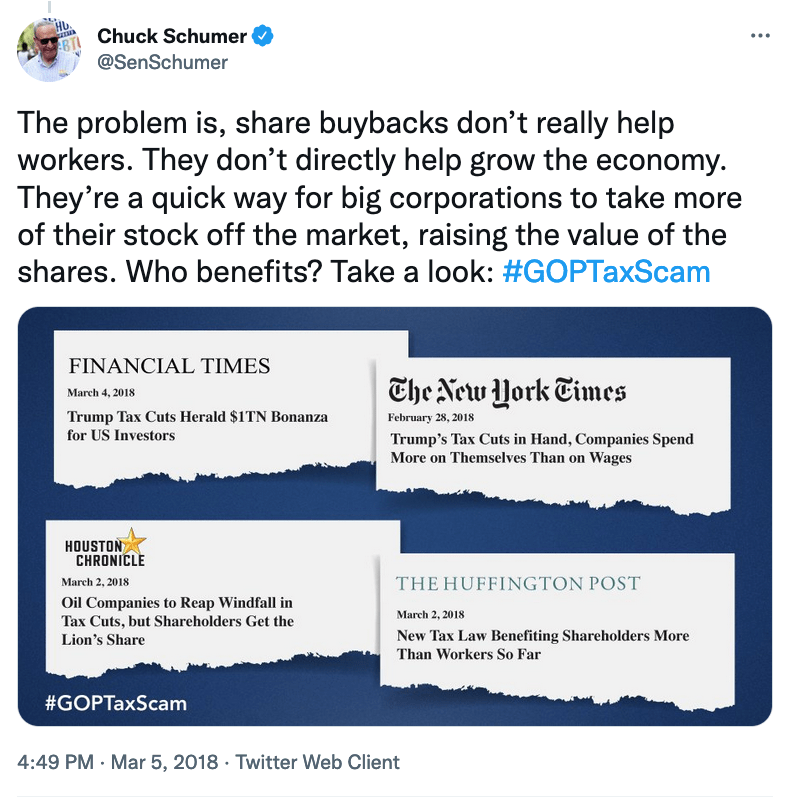

Remember that Spotify is one of the many companies that rose to dominance during the era of easy money in response to the financial crisis that was the hallmark of quantitative easing and the Federal Reserve’s Zero Interest Rate Policy beginning around 2008. Spotify’s bankers were able to fuel Daniel Ek’s desire to IPO and cash out in the public markets by enabling Spotify to run at a loss because money was cheap and the stock market had a higher tolerance for risky investments. When you get a negative interest rate for saving money, Spotify stock doesn’t seem like a totally insane investment by comparison. This may have contributed to two stock buy-back programs of $1 billion each, Spotify’s deal with Barcelona FC and other notorious excesses.

As a great man said, don’t confuse leverage for genius. It was only a matter of time until the harsh new world of quantitative tightening and sharply higher inflation came back to bite. For many years, Spotify told Wall Street a growth story which deflected attention away from the company’s loss making operations. A growth story pumps up the stock price until the chickens start coming home to roost. (Growth is also the reason to put off exercising pricing power over subscriptions.) Investors bought into the growth story in the absence of alternatives, not just for Spotify but for the market in general (compare Russell Growth and Value indexes from 2008-2023). Cutting costs and seeking profit is an example of what public company CEOs might do in anticipation of a rotational shift from growth to value investing that could hit their shares.

Never forget that due to Daniel Ek’s super-voting stock (itself an ESG fail), he is in control of Spotify. So there’s nowhere to hide when the iconography turns to blame. It’s not that easy or cheap to fire him, but if the board really wanted to give him the heave, they could do it.

I expect that Ek’s newly found parsimony will be even more front and center in renegotiations of Spotify’s royalty deals since he’s always blamed the labels for why Spotify can’t turn a profit. Not that WTC lease, surely. This would be a lot more tolerable from someone you thought was actually making an effort to cut all costs not just your revenue. Maybe that will happen, but even if Spotify became a lean mean machine, it will take years to recover from the 1999 levels of stupid that preceded it.

Hellooo Apple. One big thinker in music business issues calls it “Spotify drunk” which describes the tendency of record company marketers to focus entirely on Spotify and essentially ignore Apple Music as a distribution partner. If you’re in that group drinking the Spotify Kool Aid, you may want to give Apple another look. One thing that is almost certain is that that Apple will still be around in five years.

Just sayin.

Mechanicals on Physical and Downloads Get COLA Increase; Nothing for Streaming

Recall that the “Phonorecords IV” minimum mechanical royalties paid by record companies on physical and downloads increased from 9.1¢ to 12¢ with an annual cost of living adjustment each year of the PR IV rate period. The first increase was calculated by the Copyright Royalty Judges and was announced this week. That increase was from 12¢ to 12.40¢ and is automatic effective January 1, 2024.

Note that there is no COLA increase for streaming for reasons I personally do not understand. There really is no justification for not applying a COLA to a government mandated rate that blocks renegotiation to cover inflation expectations. After all, it works for Edmund Phelps.

The Federal Trade Commission on Copyright and AI

The FTC’s comment in the Copyright Office AI inquiry shows an interesting insight to the Commission’s thinking on some of the same copyright issues that bother us about AI, especially AI training. Despite Elon Musk’s refreshing candor of the obvious truth about AI training on copyrights, the usual suspects in the Copyleft (Pam Samuelson, Sy Damle, etc.) seem to have a hard time acknowledging the unfair competition aspects of AI and AI training (at p. 5):

Conduct that may violate the copyright laws––such as training an AI tool on protected expression without the creator’s consent or selling output generated from such an AI tool, including by mimicking the creator’s writing style, vocal or instrumental performance, or likeness—may also constitute an unfair method of competition or an unfair or deceptive practice, especially when the copyright violation deceives consumers, exploits a creator’s reputation or diminishes the value of her existing or future works, reveals private information, or otherwise causes substantial injury to consumers. In addition, conduct that may be consistent with the copyright laws nevertheless may violate Section 5.

We’ve seen unfair competition claims pleaded in the AI cases–maybe we should be thinking about trying to engage the FTC in prosecutions.

The UK Government “Took the Bait”: Eric Schmidt Says the Quiet Part Out Loudon Biden AI Executive Order and Global Governance

There are a lot of moves being made in the US, UK and Europe right now that will affect copyright policy for at least a generation. Google’s past chair Eric Schmidt has been working behind the scenes for the last two years at least to establish US artificial intelligence policy. Those efforts produced the “Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence“, the longest executive order in history. That EO was signed into effect by President Biden on October 30, so it’s done. (It is very unlikely that that EO was drafted entirely at Executive Branch agencies.)

You may ask, how exactly did this sweeping Executive Order come to pass? Who was behind it, because someone always is. As you will see in his own words, Eric Schmidt, Google and unnamed senior engineers from the existing AI platforms are quickly making the rule and essentially drafted the Executive Order that President Biden signed into law on October 30. And which was presented as what Mr. Schmidt calls “bait” to the UK government–which convened a global AI safety conference convened by His Excellency Rishi Sunak (the UK’s tech bro Prime Minister) that just happened to start on November 1, the day after President Biden signed the EO, at Bletchley Park in the UK (see Alan Turing). (See “Excited schoolboy Sunak gushes as mentor Musk warns of humanoid robot catastrophe.”)

Remember, an executive order is an administrative directive from the President of the United States that addresses the operations of the federal government, particularly the vast Executive Branch. In that sense, Executive Orders are anti-majoritarian and are as close to at least a royal decree or Executive Branch legislation as we get in the United States (see Separation of Powers, Federalist 47 and Montesquieu). Executive orders are not legislation; they require no approval from Congress, and Congress cannot simply overturn them.

So you can see if the special interests wanted to slide something by the people that was difficult to undo or difficult to pass in the People’s House…and based on Eric Schmidt’s recent interview with Mike Allen at the Axios AI+ (available here), this appears to be exactly what happened with the sweeping and vastly concerning AI Executive Order. I strongly recommend that you watch Mike Allen’s “interview” with Mr. Schmidt which fortunately is the first conversation in the rather long video of the entire event. I put “interview” in scare quotes because whatever it is, it isn’t the kind of interview that prompts probing questions that might put Mr. Schmidt on the spot. That’s understandable because Axios is selling a conference and you simply won’t get senior corporate executives to attend if you put them on the spot. Not a criticism, but understand that you have to find value for your time. Mr. Schmidt’s ego provides plenty of value; it just doesn’t come from the journalists.

Crucially, Congress is not involved in issuing an executive order. Congress may refuse to fund the subject of the EO which could make it difficult to give it effect as a practical matter but Congress cannot overturn an EO. Only a sitting U.S. President may overturn an existing executive order. In Mr. Schmidt’s interview at AI+, he tells us how all this regulatory activity happened:

The tech peoplealong with myself have been meeting for about a year. The narrative goes something like this: We are moving well past regulatory or government understanding of what is possible, we accept that. [Remember the antecedent of “we” means Schmidt and “the tech people,” or more broadly the special interests, not you, me or the American people.].

Strangely…this is the first time that the senior leaders who are engineers have basically said that they want regulation, but we want it in the following ways…which as you know never works in Washington [unless you can write an Executive Order and get the President to sign it because you are the biggest corporation in commercial history].

There is a complete agreement that there are systems and scenarios that are dangerous. [Agreement by or with whom? No one asks.]. And in all of the big [AI platforms with which] you are familiar like GPT…all of them have groups that look at the guard rails [presumably internal groups of managers] and they put constraints on [their AI platform in their silo]. They say “thou shalt not talk about death, thou shall not talk about killing”. [Anthropic, which received a $300 million investment from Google] actually trained the model with its own constitution [see “Claude’s Constitution“] which they did not just write themselves, they hired a bunch of people [actually Claude’s Constitution was crowd sourced] to design a “constitution” for an AI, so it’s an interesting idea.

The problem is none of us believe this is strong enough….Our opinion at the moment is that the best path is to build some IPCC-like environment globally that allows accurate information of what is going on to the policy makers. [This is a step toward global governance for AI (and probably the Internet) through the United Nations. IPCC is the Intergovernmental Panel on Climate Change.]

So far we are on a win, the taste of winning is there. If you look at the UK event which I was part of, the UK government took the bait, took the ideas, decided to lead, they’re very good at this, and they came out with very sensible guidelines. Because the US and UK have worked really well together—there’s a group within the National Security Council here that is particularly good at this, and they got it right, and that produced this EO which is I think is the longest EO in history, that says all aspects of our government are to be organized around this.

While Mr. Schmidt may say, aw shucks dictating the rules to the government never works in Washington, but of course that’s simply not true if you’re Google. In which case it’s always true and that’s how Mr. Schmidt got his EO and will now export it to other countries.

It’s not Just Google: Microsoft Is Getting into the Act on AI and Copyright

Google and New Mountain Capital Buy BMI: Now what?

Careful observers of the BMI sale were not led astray by BMI’s Thanksgiving week press release that was dutifully written up as news by most of the usual suspects except for the fabulous Music Business Worldwide and…ahem…us. You may think we’re making too much out of the Google investment through it’s CapitalG side fund, but judging by how much BMI tried to hide the investment, I’d say that Google’s post-sale involvement probably varies inversely to the buried lede. Not to mention the culture clash over ageism so common at Google–if you’re a BMI employee who is over 30 and didn’t go to Carnegie Mellon, good luck.

After Uruguay was the first Latin American country to pass streaming remuneration laws to protect artists, Spotify threw its toys out of the pram and threatened to go home. Can we get that in writing? A Spotify exit would probably be the best thing that ever happened to increase local competition in a Spanish language country. Also, this legislation has been characterized as “equitable remuneration” which it really isn’t. It’s its own thing, see the paper I wrote for WIPO with economist Claudio Feijoo. Complete Music Update’s Chris Cook suggested that a likely result of Spotify paying the royalty would be that they would simply do a cram down with the labels on the next round of license negotiations. If that’s not prohibited in the statute, it should be, and it’s really not “paying twice for the same music” anyway. The streaming remuneration is compensation for the streamers use of and profit from the artists’ brand (both featured and nonfeatured), e.g., as stated in the International Covenant on Economic, Social and Cultural Rights and many other human rights documents:

The Covenant recognizes everyone’s right — as a human right–to the protection and the benefits from the protection of the moral and material interests derived from any scientific, literary or artistic production of which he or she is the author. This human right itself derives from the inherent dignity and worth of all persons.

It’s a nice story, but it’s just that. Just a story.

from Snatch, written by Guy Richie

You may have noticed that there is a multi-part Netflix miniseries called “The Playlist” that is based on this book:

“The Spotify Play: How CEO and Founder Daniel Ek Beat Apple, Google and Amazon in the race for audio dominance” is an English translation of Spotify Inifrån, the Swedish book that all of this is based on, which I understand is loosely translated as “Spotify Untold” or as the inside story of Spotify. How it got from “Spotify Untold” to a title straight out of a corporate comms department of failed English majors is anyone’s guess. But notice that the book has now been refocused on the really important story–ahem–of how Daniel Ek crushed the competition and secured his monopoly on global music, or as he calls it “audio”.

For these authors to refer to music as “audio” is very much in line with the story of Spotify’s business model that Daniel Ek tells to Wall Street (which is, in all likelihood, the important audience for all this from Spotify’s perspective). Listen to any Spotify earnings call and you’ll hear what I mean.

The somewhat maniacal focus on global dominance is also interesting when you think about the fact that Daniel Ek uses the 10:1 voting stock he retains to be in global control of music streaming which may explain why Spotify’s algorithms always seem to say “Bieber.” He might want to be a bit careful about the “dominance” word.

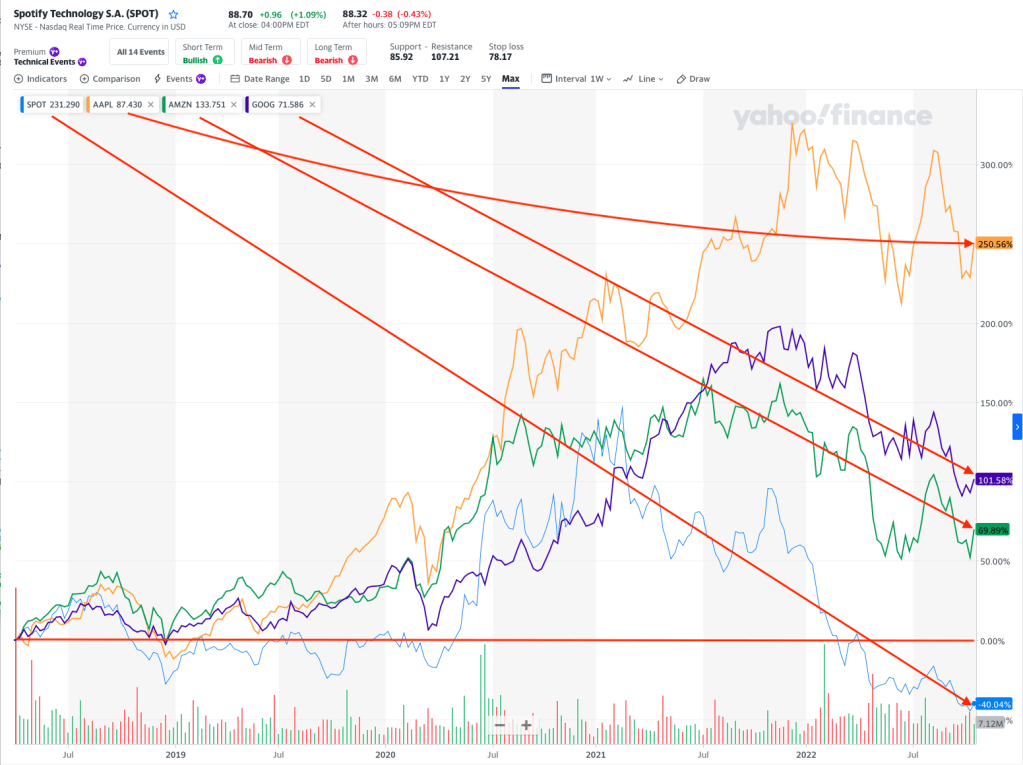

Just in time for the Netflix debut, Spotify’s stock has tanked. Which begs the question of why Spotify was ever a public company to begin with. But that’s a story for another day. Here’s what “beating” Apple, Google and Amazon looks like (the straight red line across the bottom of the chart is where Spotify closed on its first day of trading):

You’ll notice that this chart is the relative growth on a percentage basis of all these stocks measured over the same time period. Spotify briefly outperformed the others during COVID, but now is easy to find because it is the one with the minus sign in front of its growth rate.

The authors display more enthusiasm toward Ek than readers are likely to have (they call frequent lies in his personal life “entrepreneurial hustle,” and spend pages writing about the “headaches” behind his multimillion-dollar homes), and let some of his surprising claims slide as quirks, as with an account of Ek insisting Steve Jobs was calling him to breathe over the phone and intimidate him.

I think if you do the timeline of this Steve Jobs anecdote, you will find it particularly odd because Steve was kind of busy at that time. He was busy dying. Which makes the anecdote both troubling and kind of sick.

I happened to have a chat with a Hollywood film executive–let’s call him/her “Bubba”–about the Netflix miniseries and the odd way that a book in Swedish was set up for production at Netflix at lightning speed without ever being on a best seller list or gaining an audience.

“Smell that?” said Bubba, doing an impression of Robert Duvall in Apocalypse Now. “Nothing else in the world smalls like that. Smells like…astroturf.”

Really? I said. Which part?

“All of it,” Bubba said. “But look, it’s just a story. A bunch of workers got paid to tell a story that some rich guy wanted told a certain way. Those workers may go on to do something important like send their kid to college or write the next Citizen Kane or Chinatown. Or Dirty Harry for that matter. But this month they could pay for gas and their mortgage. Just another day in Hollywood. Let’s get the steak tartare.”

So lots of questions about how this book came to be written and miniseries came to be made. The solution is likely the same as it is for radio payola–disclosure.

Look at Spotify’s “Global Top 50” playlist on any day and the world’s biggest music service will show all or nearly all English language songs. With few exceptions these songs are performed by Anglo-American artists released by major record companies.

These “enterprise” playlists largely take the place of broadcast radio for many users where Spotify operates and Spotify competes with local radio for advertising revenue on the free version of Spotify.

However, Spotify has not been subject to any local content protections that would be in place for local radio broadcasters. Enterprise playlists that exclude local music contributes to the destruction of music economies, including performers. Local performers struggle even more to compete with Anglo-American repertoire, even in their own countries.

Due to this phenomenon, local artists are forced to compete for “shelf space” with everyone in their local language and then the Anglo-American artists and their record companies. This also means that local artists compete for a diminishing share of the payable royalties. The “big pool” revenue share method of royalty compensation is designed to overcompensate the English-language big names and reduce payments to artists performing in other languages in their own country.

Local Content Rules

Many countries implement local content broadcast rules that require broadcasters to play a certain number of recordings performed by local artists or indigenous people, songs written by local songwriters in local languages, or recordings that are released by locally-owned record companies.

Because streaming playlists, especially Spotify enterprise playlists or algorithmically selected recordings, are an equivalent to broadcast radio, there is a question as to whether national governments should regulate streaming services operating in their countries to require local content rules. Implementing such rules could benefit local performers and songwriters in an otherwise unsustainable enviornment.

The Fallacy of Infinite Shelf Space

Because Spotify adds recordings at a rate of 60,000 tracks daily (now reports of 100,000 tracks daily) and never deletes recordings, there is a marked competitive difference between a record store and Spotify. In the record store model, artists had to compete with recordings that were in current release; in the Spotify model, artists have to compete will all recordings ever released.

Adding the dominant influence of Anglo-American recordings on Spotify, the “infinite shelf space” simply compounds the competitive problems for non-English recordings.

Streaming RemunerationHelps Solve the Sustainability Crisis

The streaming remuneration model requires streaming services—not record companies—to pay additional compensation to nonfeatured and featured performers. Streaming remuneration would be created under national law and is compensatory in nature, not monies in exchange for a license. Existing licenses (statutory or contractual) would not be affected and remuneration payments could not be offset by streamers against label payments or by labels against artist payments.

Each country would determine the amount to be paid to performers by streaming services and the payment periods. Payments would be made to local CMOs or the equivalent depending on the infrastructure in the particular country.

European Corporate Dominance

It must also be said that the two founders of Spotify hold a 10:1 voting control over the company through special stock issued only to them. This means that these two Caucasian Europeans control 100% of the dominant music streaming company in the world. For comparison, Google and Facebook have a similar model, while Apple has a 1 share 1 vote structure as does Amazon (although Jeff Bezos owns a controlling interest in Amazon).

The net effect is that the entire global streaming music industry is controlled by six Caucasian males of European descent. This demography also argues for local content rules to protect local performers from these influences that have produced an English-only Global Top 50 playlist.

Local governments could consider whether companies with the 10:1 voting stock (so-called “dual class” or “supervoting” shares) should be allowed to operate locally.

Countries Can Respond to Streaming’s Homogenized Algorithmic Playlist Culture

Many national cultural protection laws have a history of sustaining local culture and musicians in the face of the Anglo-American Top 40 juggernaut. There is no reason to think that these agencies are not up for the task of protecting their citizens in the face of algorithms and neuromarketing.

Emmanuel Legrand prepared an excellent and important study for the European Grouping of Societies of Authors and Composers (GESAC) that identifies crucial effects of streaming on culture, creatives and especially songwriters. The study highlights the cultural effects of streaming on the European markets, but it would be easy to extend these harms globally as Emmanuel observes.

For example, consider the core pitch of streaming services that started long ago with the commercial Napster 2.0 pitch of “Own Nothing, Have Everything”. This call-to-serfdom slogan may sound good but having infinite shelf space with no cutouts or localized offering creates its own cultural imperative. And that’s even if you accept the premise the algorithmically programed enterprise playlists on streaming services should not be subject to the same cultural protections for performers and songwriters as broadcast radio–its main competitor.

[This] massive availability of content on [streaming] platforms is overshadowed by the fact that these services are under no positive obligations to ensure visibility and discoverability of more diverse repertoires, particularly European works….[plus] the initial individual subscription fee of 9.99 (in Euros, US dollars, or British pound) set in 2006, has never increased, despite the exponential growth in the quality, amount of songs, and user-friendliness of music streaming services.

Artists working new recordings, especially in a language other than English, are forced to fight for “shelf space” and “mindshare”–that is, recognition–against every recording ever released. While this was always true theoretically; you never had that same fight the same way at Tower Records.

This is not theoretically true on streaming platforms–it is actually true because these tens of millions of historical recordings are the competition on streaming services. When you look at the global 100 charts for streaming services, almost all of the titles are in English and are largely Anglo-American releases. Yes, we know–Bad Bunny. But this year’s exception proves the rule.

And then Emmanuel notes that it is the back room algorithms–the terribly modern version of the $50 handshake–that support various payola schemes:

The use of algorithms, as well as bottleneck represented by the most popular playlists, exacerbates this. Furthermore, long-standing flaws in the operations of music streaming platforms, such as “streaming fraud”, “ghost/fake artists”, “payola schemes”, “royalty free content” and other coercive practices [not to mention YouTube withholding access to Content ID] worsen the impact on many professional creators….

This report suggests solutions to bring greater transparency in the use of algorithms and invites stakeholders to undertake a review of the economic models of streaming services and evaluate how they currently affect cultural diversity which should be promoted in its various forms — music genres, languages, origin of performers and songwriters, in particular through policy actions.

MTS readers will recall my extensive dives into the hyperefficient market share distribution of streaming royalties known as the “big pool” compared to my “ethical pool” proposal and the “user centric” alternative. As Emmanuel points out, the big pool royalty model belies a cultural imperative–if you are counting streams on a market share basis that results in the rich getting richer based on “stream share” that same stream share almost guarantees that Anglo American repertoire will dominate in every market the big streamers operate.

Emmanuel uses French-Canadian repertoire as an example (a subject I know a fair amount about since I performed and recorded with many vedettes before Quebecoise was cool).

A lot of research has been made in Canada with regards to discoverability, in particular in the context of French-Canadian music, which is subject to quotas for over the air broadcasters which however do not apply to music streaming services. The research shows that while the lists of new releases from Québec studied are present in a large proportion on streaming platforms, they are “not very visible and very little recommended.”

It further shows that the situation is even worse when it is not about new releases, including hit music, when the presence of titles “drops radically.” It is not very difficult to imagine that if we were to swap Québec in the above sentence with the name of any country from the European Union [or any non-Anglo American country], and even with music from the European Union as a whole, we could find similar results.

In other words, there may be aggregators with repertoire in languages other than English that deliver tracks to streamers in their countries, but–absent localized airplay rules–a Spotify user might never know the tracks were there unless the user already knew about the recording, artist or songwriter. (Speaking of Canada, check the MAPL system.)

This is a prime example of why Professor Feijoo and I proposed streaming remuneration in our WIPO study to allow performers to capture the uncompensated capital markets value to the enterprise driven by these performers. Because of the market share royalty system, revenues and royalties do not compensate all performers, particularly regional or non-featured performers (i.e., session players and singers) who essentially get zero compensation for streaming.

Emmanuel also comments on the imbalance in song royalty payments and invites a re-look at how the streaming system biases against songwriters. I would encourage everyone to stop thinking of a pie to be shared or that Johnny has more apples–when the services refuse to raise prices in order to tell a growth story to Wall Street or The City, measuring royalties by a share of some mythical royalty pie is not ever going to get it done. It will just perpetuate a discriminatory system that fails to value the very people on whose backs it was built be they songwriters or session players.

One of the sure signs of a bubble is when those invested in the bubble narrative deny the obvious. Southern California real estate is replete with examples. Another sign is when there are too many people invested in the narrative. The British corporate raider and financier Sir James Goldsmith was asked why he got into all cash the summer before the 1987 stock market crash. The apocryphal story is that it was because he got a stock tip from his barber. Facts, dear readers, facts are stubborn things.

One such fact surfaced this week–the Obamas are exiting their exclusive podcast deal with Spotify according to Yahoo News (citing Bloomberg). Now let us accept as a given that the Obamas as a brand are still one of the strongest personal brands in the world–in a brand shoot out with fellow podcasters on the Big Stream it ain’t even close. Meghan and Harry? Please.

But get a load of the reasons given. First there’s this one:

The former first couple’s media production company, Higher Ground, will split with Spotify after the streaming giant declined to make an offer to renew their deal, Bloomberg reported on Thursday, citing people familiar with negotiations.

Huh? “Declined to make an offer”? The thing about talent is that it doesn’t come around twice. If you were lucky enough to get into business with real stars, you hang on for dear life. Granted that statement sounds a bit like press release BS to keep the Obamas from looking greedy, but it’s not greedy to want the next deal point–it’s just creativity and smart business to keep that talent feeling ike the best place in the universe to work on that creativity is in your house.

High Ground’s departure follows a number of disagreements with Spotify, such as how frequently the Obamas would feature in output, and over exclusivity of shows, including the former president’s podcast with Bruce Springsteen, according to Bloomberg.

Say what? How often do the Obamas “feature in output”? As many times as they want. If you’ll pay $100 million for Joe Rogan (or whatever the 9 figure number actually is), you will understand that the deal is basically about freedom, like this:

The first show under the Obamas’ Spotify deal, “The Michelle Obama Podcast,” was among the platform’s most popular podcasts during its exclusive run, though Spotify later made it available on rival podcast apps. Barack Obama also hosted his own Spotify show called “Renegades: Born in the USA,” alongside musician Bruce Springsteen.

So let’s get this straight–the Spot will pay big bucks for Rogan and the naming rights to the Barcelona football club and their Camp Nou stadium, but turn around and be cheap and petty with Barack and Michelle Obama.

Right.

As I told the UK Competition and Markets Authority, do not mistake muscle for genius. Spoxit is on the move.

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

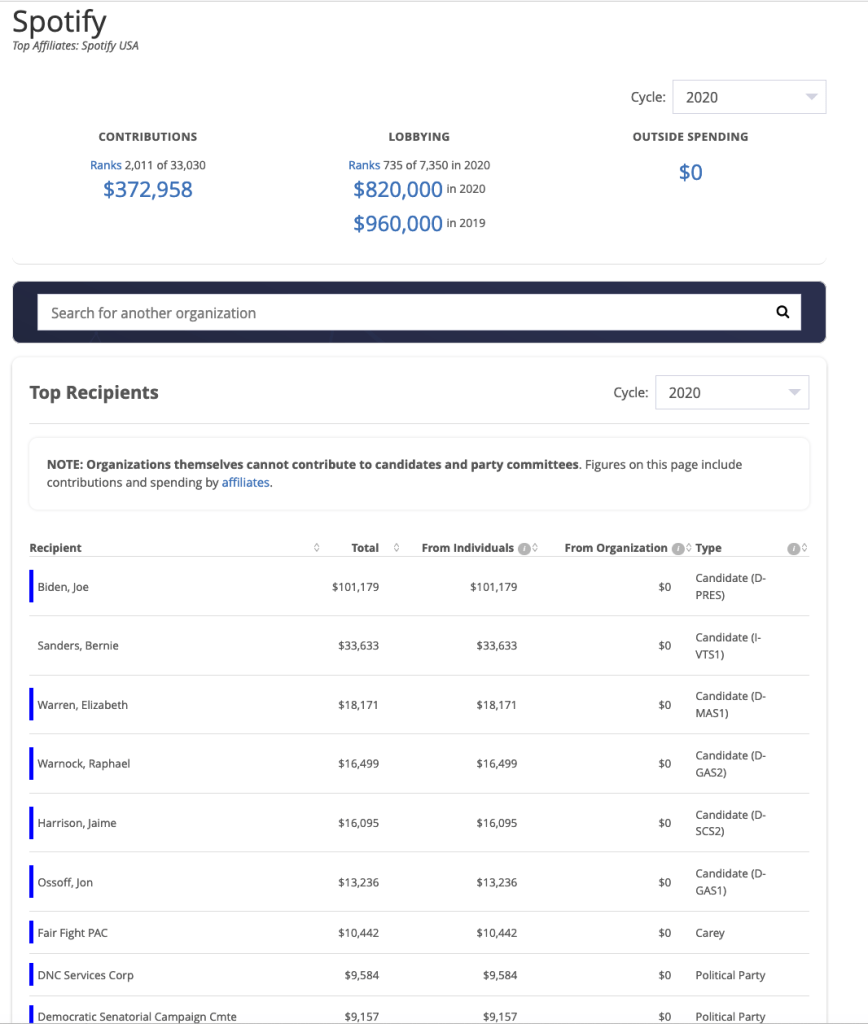

On the political side, let’s see what the company’s campaign contributions tell us:

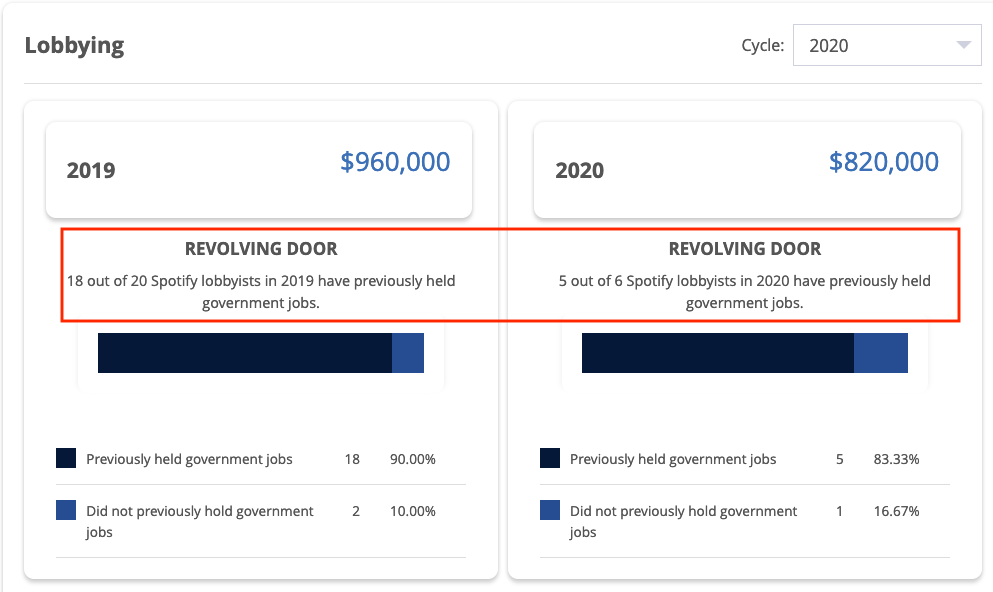

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score.

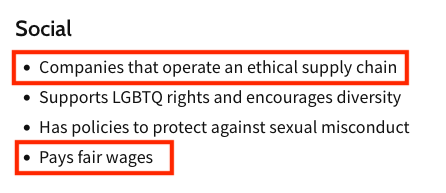

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.