Spotify has announced they are “Modernizing Our Royalty System.” Beware of geeks bearing “modernization”–that almost always means they get what they want to your disadvantage. Also sounds like yet another safe harbor. At a minimum, they are demonstrating the usual lack of understanding of the delicate balance of the music business they now control. But if they can convince you not to object, then they get away with it.

Don’t let them.

An Attack on Property Rights

There’s some serious questions about whether Spotify has the right to unilaterally change the way it counts royalty-bearing streams and to encroach on the private property rights of artists.

Here’s their plan: Evidently the plan is to only pay on streams over 1,000 per song accruing during the previous 12 months. I seriously doubt that they can engage in this terribly modern “stream discrimination” in a way that doesn’t breach any negotiated direct license with a minimum guarantee (if not others).

That doubt also leads me to think that Spotify’s unilateral change in “royalty policy” (whatever that is) is unlikely to affect everyone the same. Taking a page from 1984newspeakers, Spotify calls this discrimination policy “Track Monetization Eligibility”. It’s not discrimination, you see, it’s “eligibility”, a whole new thing. Kind of like war is peace, right? Or bouillabaisse.

According to Spotify’s own announcement this proposed change is not an increase in the total royalty pool that Spotify pays out (God forbid the famous “pie” should actually grow): ”There is no change to the size of the music royalty pool being paid out to rights holders from Spotify; we will simply use the tens of millions of dollars annually [of your money] to increase the payments to all eligible tracks, rather than spreading it out into $0.03 payments [that we currently owe you].”

Yep, you won’t even miss it, and you should sacrifice for all those deserving artists who are more eligible than you. They are not growing the pie, they are shifting money around–rearranging the deck chairs.

Spotify’s Need for Living Space

So why is Spotify doing this to you? The simple answer is the same reason monopolists always use: they need living space for Greater Spotify. Or more simply, because they can, or they can try. They’ll tell you it’s to address “streaming fraud” but there are a lot more direct ways to address streaming fraud such as establishing a simple “know your vendor” policy, or a simple pruning policy similar to that established by record companies to cut out low-sellers (excluding classical and instrumental jazz). But that would require Spotify to get real about their growth rates and be honest with their shareholders and partners. Based on the way Spotify treated the country of Uruguay, they are more interested in espoliating a country’s cultural resources than they are in fairly compensating musicians.

Of course, they won’t tell you that side of the story. They won’t even tell you if certain genres or languages will be more impacted than others (like the way labels protected classical and instrumental jazz from getting cut out measured by pop standards). Here’s their explanation:

It’s more impactful [says who?] for these tens of millions of dollars per year to increase payments to those most dependent on streaming revenue — rather than being spread out in tiny payments that typically don’t even reach an artist (as they do not surpass distributors’ minimum payout thresholds). 99.5% of all streams are of tracks that have at least 1,000 annual streams, and each of those tracks will earn more under this policy.

This reference to “minimum payout thresholds” is a very Spotifyesque twisting of a generalization wrapped in cross reference inside of spin. Because of the tiny sums Spotify pays artists due to the insane “big pool” or “market centric” royalty model that made Spotify rich, extremely low royalties make payment a challenge.

Plus, if they want to make allegations about third party distributors, they should say which distributors they are speaking of and cite directly to specific terms and conditions of those services. We can’t ask these anonymous distributors about their policies if we don’t know who they are.

What’s more likely is that tech platforms like PayPal stack up transaction fees to make the payment cost more than the royalty paid. Of course, you could probably say that about all streaming if you calculate the cost of accounting on a per stream basis, but that’s a different conversation.

So Spotify wants you to ignore the fact that they impose this “market centric” royalty rate that pays you bupkis in the first place. Since your distributor holds the tiny slivers of money anyway, Spotify just won’t pay you at all. It’s all the same to you, right? You weren’t getting paid anyway, so Spotify will just give your money to these other artists who didn’t ask for it and probably wouldn’t want it if you asked them.

There is a narrative going around that somehow the major labels are behind this. I seriously doubt it–if they ever got caught with their fingers in the cookie jar on this scam, would it be worth the pittance that they will end up getting in pocket after all mouths are fed? The scam is also 180 out from Lucian Grange’s call for artist centric royalty rates, so as a matter of policy it’s inconsistent with at least Universal’s stated goals. So I’d be careful about buying into that theory without some proof.

What About Mechanical Royalties?

What’s interesting about this scam is that switching to Spotify’s obligations on the song side, the accounting rules for mechanical royalties say (37 CFR § 210.6(g)(6) for those reading along at home) seem to contradict the very suckers deal that Spotify is cramming down on the recording side:

Royalties under 17 U.S.C. 115 shall not be considered payable, and no Monthly Statement of Account shall be required, until the compulsory licensee’s [i.e., Spotify’s] cumulative unpaid royalties for the copyright owner equal at least one cent. Moreover, in any case in which the cumulative unpaid royalties under 17 U.S.C. 115 that would otherwise be payable by the compulsory licensee to the copyright owner are less than $5, and the copyright owner has not notified the compulsory licensee in writing that it wishes to receive Monthly Statements of Account reflecting payments of less than $5, the compulsory licensee may choose to defer the payment date for such royalties and provide no Monthly Statements of Account until the earlier of the time for rendering the Monthly Statement of Account for the month in which the compulsory licensee’s cumulative unpaid royalties under section 17 U.S.C. 115 for the copyright owner exceed $5 or the time for rendering the Annual Statement of Account, at which time the compulsory licensee may provide one statement and payment covering the entire period for which royalty payments were deferred.

Much has been made of the fact that Spotify may think it can unilaterally change its obligations to pay sound recording royalties, but they still have to pay mechanicals because of the statute. And when they pay mechanicals, the accounting rules have some pretty low thresholds that require them to pay small amounts. This seems to be the very issue they are criticizing with their proposed change in “royalty policy.”

But remember that the only reason that Spotify has to pay mechanical royalties on the stream discrimination is because they haven’t managed to get that free ride inserted into the mechanical royalty rates alongside all the other safe harbors and goodies they seem to have bought for their payment of historical black box.

So I would expect that Spotify will show up at the Copyright Royalty Board for Phonorecords V and insist on a safe harbor to enshrine stream discrimination into the Rube Goldberg streaming mechanical royalty rates. After all, controlled compositions are only paid on royalty bearing sales, right? And since it seems like they get everything else they want, everyone will roll over and give this to them, too. Then the statutory mechanical will give them protection.

To Each According to Their Needs

Personally, I have an issue with any exception that results in any artist being forced to accept a royalty free deal. Plus, it seems like what should be happening here is that underperforming tracks get dropped, but that doesn’t support the narrative that all the world’s music is on offer. Just not paid for.

Is it a lot of money to any one person? Not really, but it’s obviously enough money to make the exercise worthwhile to Spotify. And notice that they haven’t really told you how much money is involved. It may be that Spotify isn’t holding back any small payments from distributors if all payments are aggregated. But either way it does seem like this new new thing should start with a clean slate–and all accrued royalties should be paid.

This idea that you should be forced to give up any income at all for the greater good of someone else is kind of an odd way of thinking. Or as they say back in the home country, from each according to their ability and to each according to their needs. And you don’t really need the money, do you?

By the way, can you break a $20?

The NO AI Fraud Act

Thanks to U.S. Representatives Salazar and Dean, there’s an effort underway to limit Big Tech’s AI rampage just in time for Davos. (Remember, the AI bubble got started at last year’s World Economic Forum Winter Games in Davos, Switzerland).

Chairman Issa Questions MLC’s Secretive Investment Policyfor Hundreds of Millions in Black Box

As we’ve noted a few times, the MLC has a nontransparent–some might say “secretive”–investment policy that has the effect of a government rule. This has caught the attention of Chairman Darrell Issa and Rep. Ben Cline at a recent House oversight hearing. Chairman Issa asked for more information about the investment policy in follow-up “questions for the record” directed to MLC CEO Kris Ahrend. It’s worth getting smart about what the MLC is up to in advance of the upcoming “redesignation” proceeding at the Copyright Office. We all know the decision is cooked and scammed already as part of the Harry Fox Preservation Act (AKA Title I of the MMA), but it will be interesting to see if anyone actually cares and the investment policy is a perfect example. It will also be interesting to see which Copyright Office examiner goes to work for one of the DiMA companies after the redesignation as is their tradition.

It is commonplace for artists to conduct a royalty examination of their record company, sometimes called an “audit.” Until the Music Modernization Act, the statutory license did not permit songwriters to audit users of the statutory license. The Harry Fox Agency “standard” license for physical records had two principal features that differed from the straight statutory license: quarterly accounting and an audit right. When streaming became popular, the services both refused to comply with the statutory regulations and also refused to allow anyone to audit because the statutory regulations they failed to comply with did not permit an audit. I brought this absurdity to the attention of the Copyright Office in 2011.

After much hoopla, the lobbyists wrote an audit right for copyright owners into the Music Modernization Act. However, rather than permitting copyright owners to audit music users as is long standing common practice on the record side, the lobbyists decided to allow copyright owners to audit theMechanical Licensing Collective. This is consistent with the desire of services to distance themselves from those pesky songwriters by inserting the MLC in between the services and their ultimate vendors, the songwriters and copyright owners. The services can be audited by the MLC (whose salaries are paid by the services), but that hasn’t happened yet to my knowledge.

But the MLC has received what I believe is its first audit notice that was just published by the Copyright Office after receiving it on November 9. First up is Bridgeport Music, Inc. for the period January 1, 2021, through December 31, 2023. January 1, 2021 was the “license availability date” or the date that the MLC began accounting for royalties under the MMA’s blanket license.

Bridgeport’s audit is wise. There are no doubt millions if not billions of streams to be verified. The MLC’s systems are largely untested, compared to other music users such as record companies that have been audited hundreds, if not thousands of times depending on how long they are operating. Competent royalty examiners will look under the hood and find out whether it’s even possible to render reasonably accurate accounting statements given the MLC’s systems. Maybe it’s all fine, but maybe it’s not. The wisdom of Bridgeport’s two year audit window is that two years is long enough to have a chance at a recovery but it’s not so long that you are drowned in data and susceptible to taking shortcuts.

In other words, why wait around?

Auditing the Black Box

A big difference between the audit rules the lobbyists wrote into the MMA and other audits is that the MLC audit is based on payments, not statements. The relevant language in the statute makes this very clear:

A copyright owner entitled to receive payments of royalties for covered activities from the mechanical licensing collective may, individually or with other copyright owners, conduct an audit of the mechanical licensing collective to verify the accuracy of royalty payments by the mechanical licensing collective to such copyright owner…The qualified auditor shall determine the accuracy of royalty payments, including whether an underpayment or overpayment of royalties was made by the mechanical licensing collective to each auditing copyright owner.

Royalty payments would include a share of black box royalties distributed to copyright owners. It seems reasonable that on audit a copyright owner could verify how this share was arrived at and whatever calculations would be necessary to calculate those payments, or maybe the absence of such payments that should have been made. Determining what is not paid that should have been paid is an important part of any royalty verification examination.

Systems Transparency

Information too confidential to be detected cannot be corrected. It is important to remember that copyright owner audits of the MLC will be the first time an independent third party has had a look at the accounting systems and functional technology of The MLC. If those audits reveal functional defects in the MLC’s systems or technology that affects any output of The MLC, i.e., not just the royalties being audited, it seems to me that those defects should be disclosed to the public. Audit settlements should not be used as hush money payments to keep embarrassing revelations from being publicly disclosed.

Unsurprisingly, The MLC lobbied to have broadly confidential treatment of all audits. Realize that there may well be confidential financial information disclosed as part of any audit that both copyright owners and The MLC will want to keep secret. There is no reason to keep secrets about The MLC’s systems. To take an extreme example, if on audit the auditors discovered that The MLC’s systems added 2 plus 2 and got 5, that is a fact that others have a legitimate interest in having disclosed to include the Copyright Office itself that is about to launch a 5 year review of The MLC for redesignation. Indeed, auditors may discover systemic flaws that could arguably require The MLC to recalculate many if not all statements or at least explain why they should not. (Note that a royalty auditor is required to deliver a copy of the auditor’s final report to The MLC for review even before giving it to their client. This puts The MLC on notice of any systemic flaws in The MLC’s systems found by the auditor and gives it the opportunity to correct any factual errors.)

I think that systemic flaws found by an auditor should be disclosed publicly after taking care to redact any confidential financial information. This will allow both the Copyright Office and MLC members to fix any discovered flaws.

The “Qualified Auditor” Typo

It is important to realize that there is no good reason why a C.P.A. must conduct the audit; this is another drafting glitch in the MMA that requires both The MLC’s audited financial statements and royalty compliance examinations be conducted by a C.P.A, defined as a “Qualified Auditor” (17 USC § 115(e)(25)). It’s easy to understand why audited financials prepared according to GAAP should be opined by a C.P.A. but it is ludicrous that a C.P.A. should be required to conduct a royalty exam for royalties that have nothing to do with GAAP and never have.

As Warner Music Group’s Ron Wilcox testified to the CRJs, “Because royalty audits require extensive technical and industry-specific expertise, in WMG’s experience a CPA certification is not generally a requirement for conducting such audits. To my knowledge, some of the. most experienced and knowledgeable royalty auditors in the music industry are not CPAs.”

The “Qualified Auditor” defined term should be limited to the MLC’s financials and removed from the audit clauses.

@VVBrown Articulates the Need for a Complete Reset of Streaming

Finally, I asked singer-songwriter VV Brown about the impact of streaming:

"It's impacted my income massively, we aren't making the money we should, I don't see my music as a way for me to survive – put food on the table. We have to change this; we need a complete reset." (5/5) pic.twitter.com/dbXC59p2IE

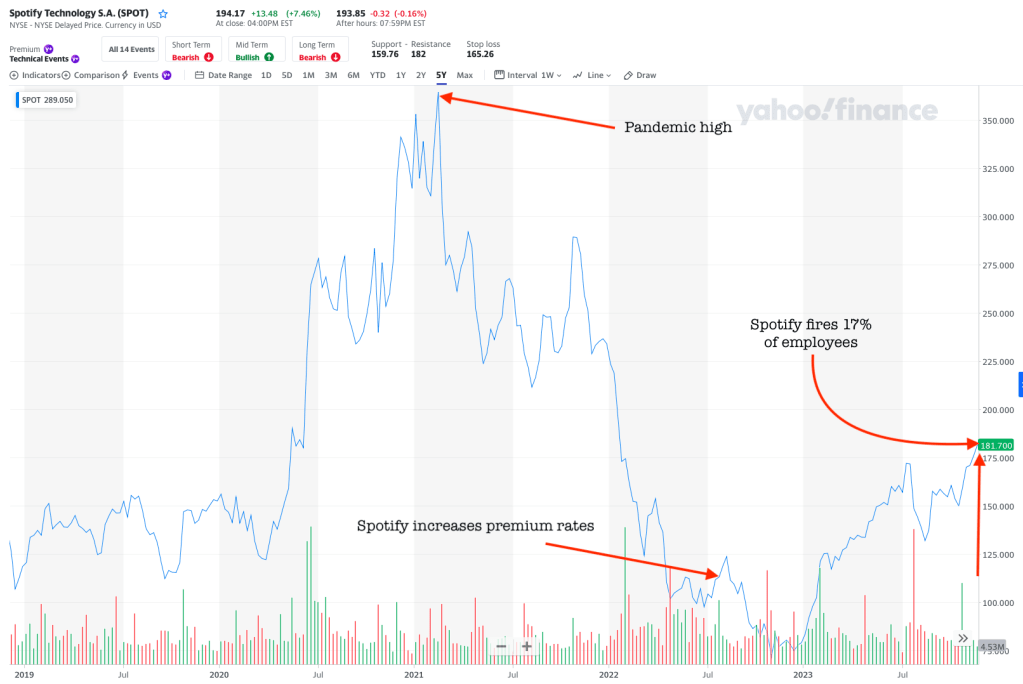

Harsh? Not really, at least not from a share price point of view. Spotify’s all time highest share price was during the COVID pandemic.

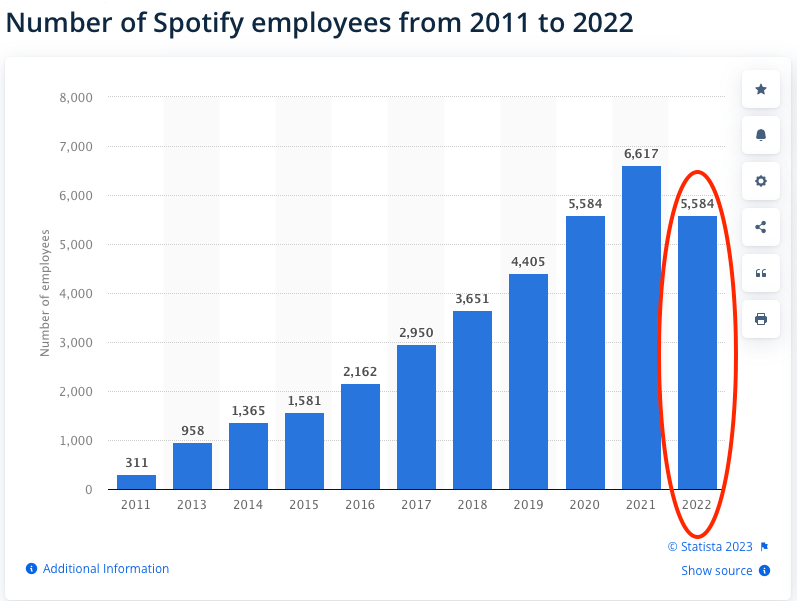

Spotify CEO Daniel Ek and the press tells us that Spotify is cutting 1,500 jobs which works out to about 17% of Spotify employees. Which works out to a pre-layoff workforce of 8,823. So let’s start there—that workforce number seems very high and is completely out of line with some recent data from Statista which is usually reliable.

If Statista is correct, Spotify employed 5,584 as of last year. Yet somehow Spotify’s 2023 workforce grew to 9200 according to the Guardian, fully 2/3 over that 2022 level without a commensurate and offsetting growth in revenue. That’s a governance question in and of itself.

Why the layoffs? The Guardian reports that Spotify CEO Daniel Ek is concerned about costs. He says “Despite our efforts to reduce costs this past year, our cost structure for where we need to be is too big.” Maybe I missed it, but the only time I can recall Daniel Ek being vocally concerned about Spotify’s operating costs was when it came to paying royalties. Then it was full-blown poor mouthing while signing leases for very expensive office space in 4 World Trade Center as well as other pricy real estate, executive compensation and podcasters like Harry & Meghan.

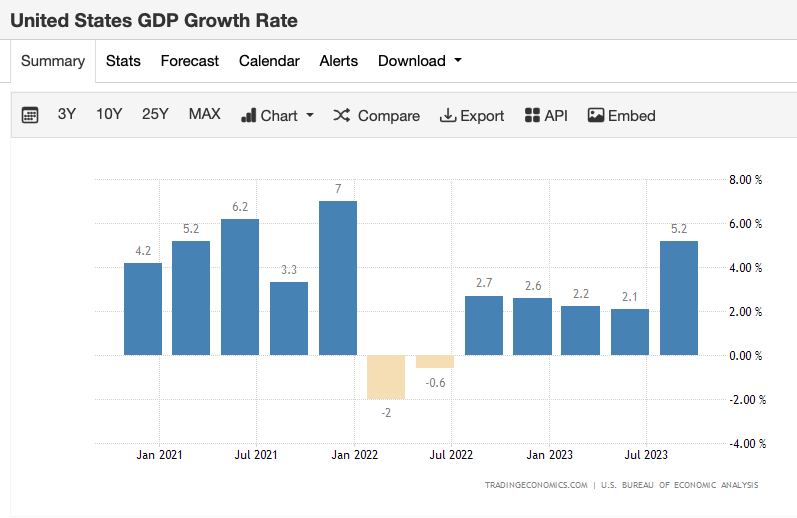

Over the last two years, we’ve put significant emphasis on building Spotify into a truly great and sustainable business – one designed to achieve our goal of being the world’s leading audio company and one that will consistently drive profitability and growth into the future. While we’ve made worthy strides, as I’ve shared many times, we still have work to do. Economic growth has slowed dramatically and capital has become more expensive. Spotify is not an exception to these realities.

Which “economic growth” is that?

But, he is definitely right about capital costs.

Still, Spotify’s job cuts are not necessarily that surprising considering the macro economy, most specifically rents and interest rates. As recently as 2018, Spotify was the second largest tenant at 4 WTC. Considering the sheer size of Spotify’s New York office space, it’s not surprising that Spotify is now sublettingfive floors of 4 WTC earlier this year. That’s right, the company had a spare five floors. Can that excess just be more people working at home given Mr. Ek’s decision to expand Spotify’s workforce? But why does Spotify need to be a major tenant in World Trade Center in the first place? Renting the big New York office space is the corporate equivalent of playing house. That’s an expensive game of pretend.

Remember that Spotify is one of the many companies that rose to dominance during the era of easy money in response to the financial crisis that was the hallmark of quantitative easing and the Federal Reserve’s Zero Interest Rate Policy beginning around 2008. Spotify’s bankers were able to fuel Daniel Ek’s desire to IPO and cash out in the public markets by enabling Spotify to run at a loss because money was cheap and the stock market had a higher tolerance for risky investments. When you get a negative interest rate for saving money, Spotify stock doesn’t seem like a totally insane investment by comparison. This may have contributed to two stock buy-back programs of $1 billion each, Spotify’s deal with Barcelona FC and other notorious excesses.

As a great man said, don’t confuse leverage for genius. It was only a matter of time until the harsh new world of quantitative tightening and sharply higher inflation came back to bite. For many years, Spotify told Wall Street a growth story which deflected attention away from the company’s loss making operations. A growth story pumps up the stock price until the chickens start coming home to roost. (Growth is also the reason to put off exercising pricing power over subscriptions.) Investors bought into the growth story in the absence of alternatives, not just for Spotify but for the market in general (compare Russell Growth and Value indexes from 2008-2023). Cutting costs and seeking profit is an example of what public company CEOs might do in anticipation of a rotational shift from growth to value investing that could hit their shares.

Never forget that due to Daniel Ek’s super-voting stock (itself an ESG fail), he is in control of Spotify. So there’s nowhere to hide when the iconography turns to blame. It’s not that easy or cheap to fire him, but if the board really wanted to give him the heave, they could do it.

I expect that Ek’s newly found parsimony will be even more front and center in renegotiations of Spotify’s royalty deals since he’s always blamed the labels for why Spotify can’t turn a profit. Not that WTC lease, surely. This would be a lot more tolerable from someone you thought was actually making an effort to cut all costs not just your revenue. Maybe that will happen, but even if Spotify became a lean mean machine, it will take years to recover from the 1999 levels of stupid that preceded it.

Hellooo Apple. One big thinker in music business issues calls it “Spotify drunk” which describes the tendency of record company marketers to focus entirely on Spotify and essentially ignore Apple Music as a distribution partner. If you’re in that group drinking the Spotify Kool Aid, you may want to give Apple another look. One thing that is almost certain is that that Apple will still be around in five years.

Just sayin.

Mechanicals on Physical and Downloads Get COLA Increase; Nothing for Streaming

Recall that the “Phonorecords IV” minimum mechanical royalties paid by record companies on physical and downloads increased from 9.1¢ to 12¢ with an annual cost of living adjustment each year of the PR IV rate period. The first increase was calculated by the Copyright Royalty Judges and was announced this week. That increase was from 12¢ to 12.40¢ and is automatic effective January 1, 2024.

Note that there is no COLA increase for streaming for reasons I personally do not understand. There really is no justification for not applying a COLA to a government mandated rate that blocks renegotiation to cover inflation expectations. After all, it works for Edmund Phelps.

The Federal Trade Commission on Copyright and AI

The FTC’s comment in the Copyright Office AI inquiry shows an interesting insight to the Commission’s thinking on some of the same copyright issues that bother us about AI, especially AI training. Despite Elon Musk’s refreshing candor of the obvious truth about AI training on copyrights, the usual suspects in the Copyleft (Pam Samuelson, Sy Damle, etc.) seem to have a hard time acknowledging the unfair competition aspects of AI and AI training (at p. 5):

Conduct that may violate the copyright laws––such as training an AI tool on protected expression without the creator’s consent or selling output generated from such an AI tool, including by mimicking the creator’s writing style, vocal or instrumental performance, or likeness—may also constitute an unfair method of competition or an unfair or deceptive practice, especially when the copyright violation deceives consumers, exploits a creator’s reputation or diminishes the value of her existing or future works, reveals private information, or otherwise causes substantial injury to consumers. In addition, conduct that may be consistent with the copyright laws nevertheless may violate Section 5.

We’ve seen unfair competition claims pleaded in the AI cases–maybe we should be thinking about trying to engage the FTC in prosecutions.

The UK Government “Took the Bait”: Eric Schmidt Says the Quiet Part Out Loudon Biden AI Executive Order and Global Governance

There are a lot of moves being made in the US, UK and Europe right now that will affect copyright policy for at least a generation. Google’s past chair Eric Schmidt has been working behind the scenes for the last two years at least to establish US artificial intelligence policy. Those efforts produced the “Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence“, the longest executive order in history. That EO was signed into effect by President Biden on October 30, so it’s done. (It is very unlikely that that EO was drafted entirely at Executive Branch agencies.)

You may ask, how exactly did this sweeping Executive Order come to pass? Who was behind it, because someone always is. As you will see in his own words, Eric Schmidt, Google and unnamed senior engineers from the existing AI platforms are quickly making the rule and essentially drafted the Executive Order that President Biden signed into law on October 30. And which was presented as what Mr. Schmidt calls “bait” to the UK government–which convened a global AI safety conference convened by His Excellency Rishi Sunak (the UK’s tech bro Prime Minister) that just happened to start on November 1, the day after President Biden signed the EO, at Bletchley Park in the UK (see Alan Turing). (See “Excited schoolboy Sunak gushes as mentor Musk warns of humanoid robot catastrophe.”)

Remember, an executive order is an administrative directive from the President of the United States that addresses the operations of the federal government, particularly the vast Executive Branch. In that sense, Executive Orders are anti-majoritarian and are as close to at least a royal decree or Executive Branch legislation as we get in the United States (see Separation of Powers, Federalist 47 and Montesquieu). Executive orders are not legislation; they require no approval from Congress, and Congress cannot simply overturn them.

So you can see if the special interests wanted to slide something by the people that was difficult to undo or difficult to pass in the People’s House…and based on Eric Schmidt’s recent interview with Mike Allen at the Axios AI+ (available here), this appears to be exactly what happened with the sweeping and vastly concerning AI Executive Order. I strongly recommend that you watch Mike Allen’s “interview” with Mr. Schmidt which fortunately is the first conversation in the rather long video of the entire event. I put “interview” in scare quotes because whatever it is, it isn’t the kind of interview that prompts probing questions that might put Mr. Schmidt on the spot. That’s understandable because Axios is selling a conference and you simply won’t get senior corporate executives to attend if you put them on the spot. Not a criticism, but understand that you have to find value for your time. Mr. Schmidt’s ego provides plenty of value; it just doesn’t come from the journalists.

Crucially, Congress is not involved in issuing an executive order. Congress may refuse to fund the subject of the EO which could make it difficult to give it effect as a practical matter but Congress cannot overturn an EO. Only a sitting U.S. President may overturn an existing executive order. In Mr. Schmidt’s interview at AI+, he tells us how all this regulatory activity happened:

The tech peoplealong with myself have been meeting for about a year. The narrative goes something like this: We are moving well past regulatory or government understanding of what is possible, we accept that. [Remember the antecedent of “we” means Schmidt and “the tech people,” or more broadly the special interests, not you, me or the American people.].

Strangely…this is the first time that the senior leaders who are engineers have basically said that they want regulation, but we want it in the following ways…which as you know never works in Washington [unless you can write an Executive Order and get the President to sign it because you are the biggest corporation in commercial history].

There is a complete agreement that there are systems and scenarios that are dangerous. [Agreement by or with whom? No one asks.]. And in all of the big [AI platforms with which] you are familiar like GPT…all of them have groups that look at the guard rails [presumably internal groups of managers] and they put constraints on [their AI platform in their silo]. They say “thou shalt not talk about death, thou shall not talk about killing”. [Anthropic, which received a $300 million investment from Google] actually trained the model with its own constitution [see “Claude’s Constitution“] which they did not just write themselves, they hired a bunch of people [actually Claude’s Constitution was crowd sourced] to design a “constitution” for an AI, so it’s an interesting idea.

The problem is none of us believe this is strong enough….Our opinion at the moment is that the best path is to build some IPCC-like environment globally that allows accurate information of what is going on to the policy makers. [This is a step toward global governance for AI (and probably the Internet) through the United Nations. IPCC is the Intergovernmental Panel on Climate Change.]

So far we are on a win, the taste of winning is there. If you look at the UK event which I was part of, the UK government took the bait, took the ideas, decided to lead, they’re very good at this, and they came out with very sensible guidelines. Because the US and UK have worked really well together—there’s a group within the National Security Council here that is particularly good at this, and they got it right, and that produced this EO which is I think is the longest EO in history, that says all aspects of our government are to be organized around this.

While Mr. Schmidt may say, aw shucks dictating the rules to the government never works in Washington, but of course that’s simply not true if you’re Google. In which case it’s always true and that’s how Mr. Schmidt got his EO and will now export it to other countries.

It’s not Just Google: Microsoft Is Getting into the Act on AI and Copyright

Google and New Mountain Capital Buy BMI: Now what?

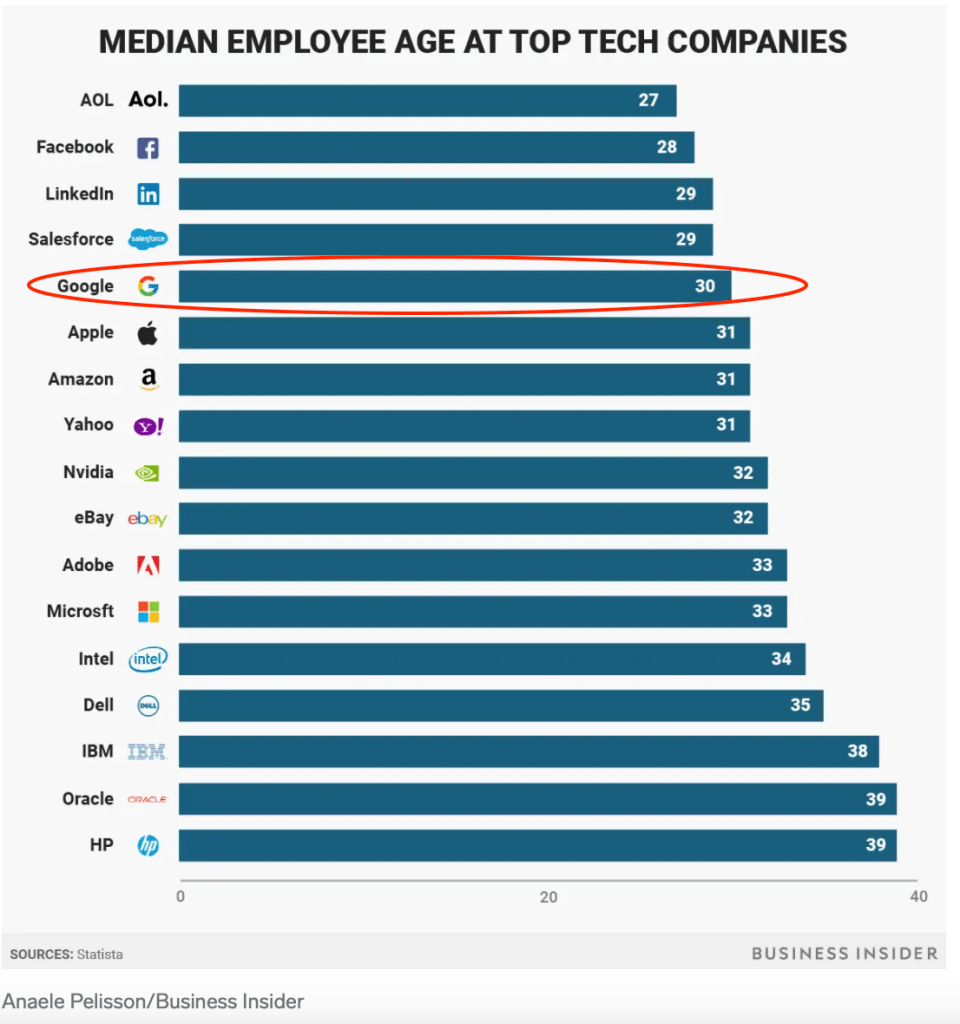

Careful observers of the BMI sale were not led astray by BMI’s Thanksgiving week press release that was dutifully written up as news by most of the usual suspects except for the fabulous Music Business Worldwide and…ahem…us. You may think we’re making too much out of the Google investment through it’s CapitalG side fund, but judging by how much BMI tried to hide the investment, I’d say that Google’s post-sale involvement probably varies inversely to the buried lede. Not to mention the culture clash over ageism so common at Google–if you’re a BMI employee who is over 30 and didn’t go to Carnegie Mellon, good luck.

After Uruguay was the first Latin American country to pass streaming remuneration laws to protect artists, Spotify threw its toys out of the pram and threatened to go home. Can we get that in writing? A Spotify exit would probably be the best thing that ever happened to increase local competition in a Spanish language country. Also, this legislation has been characterized as “equitable remuneration” which it really isn’t. It’s its own thing, see the paper I wrote for WIPO with economist Claudio Feijoo. Complete Music Update’s Chris Cook suggested that a likely result of Spotify paying the royalty would be that they would simply do a cram down with the labels on the next round of license negotiations. If that’s not prohibited in the statute, it should be, and it’s really not “paying twice for the same music” anyway. The streaming remuneration is compensation for the streamers use of and profit from the artists’ brand (both featured and nonfeatured), e.g., as stated in the International Covenant on Economic, Social and Cultural Rights and many other human rights documents:

The Covenant recognizes everyone’s right — as a human right–to the protection and the benefits from the protection of the moral and material interests derived from any scientific, literary or artistic production of which he or she is the author. This human right itself derives from the inherent dignity and worth of all persons.

BMI recently sold to New Mountain Capital and Google’s CapitalG side fund. If you review CapitalG’s website, you’ll see that the fund announces that providing Google employees to advise portfolio companies are a big part of its management style. That’s fine when the cultures of Google and the investment are compatible. But a quick review of CapitalG’s portfolio companies should tell you that the culture of BMI just ain’t quite the same as Airbnb, Fanduel or Lyft. Let’s start with the obvious one–age.

According to Business Insider, the average age of Google employees is 30. I don’t have any specific data about the average age of BMI employees, but I’d be willing to place a fairly sizable bet that it’s over 30. So when CapitalG sends a consulting team of Googlers over to BMI to help them do their jobs better, or do their jobs the Google way, the Googlers (or more likely YouTubers) will probably have to get past the initial reaction of why do you have a job?

While age is a significant issue in Silicon Valley hiring practices, salary is, too. In a stock-option environment (which probably does not exist at BMI except for the very senior management perhaps), salaries are often not as high as music industry. So the Google consultant who is dictating the new rules may well make significantly less than the BMI person they are managing. All the while wondering why AI can’t do the job and do it “better.”

Not to be cynical, but that ageist culture clash is so predictable and incurably actuarial that I would expect to see many, many early retirement offers on the table. Googlers don’t understand the concept of writer relations, they think we make too much money, have too many assistants and aren’t properly motivated.

You don’t have to look very hard for empirical evidence on Silicon Valley’s culture:

“Mark Zuckerberg said that “young people are just smarter.” In recent years, older employees have faced layoffs, or not been hired by tech companies in the first place. Older startup founders have been refused venture capital funding because they’re “not 25 years old having just left Facebook as a product manager.”

If I’m correct about that culture clash, this could be a great opportunity to take early retirement or for highly skilled employees to start something new before Google does the same thing to The MLC.

Fraudsters are using AI-enabled voice cloning to defraud & extort Americans.

Today @FTC launched a voice cloning challenge to spur ideas for how to prevent and detect voice cloning misuse. Submissions accepted from Jan. 2-12, with $25k for the winner. https://t.co/nJYmPmDMLS

Congress is considering whether to renew The MLC, Inc.‘s designation as the mechanical licensing collective. If that sentence seems contradictory, remember those are two different things: the mechanical licensing collective is the statutory body that administers the compulsory license under Section 115. The MLC, Inc. is the private company that was “designated” by Congress through its Copyright Office to do the work of the mechanical licensing collective. This is like the form of a body that performs a function (the mechanical licensing collective) and having to animate that form with actual humans (The MLC, Inc.), kind of like Plato’s allegory of the cave, shadows on the wall being what they are.

Congress reviews the work product of The MLC, Inc. every five years (17 USC §115(d)(3)(B)(ii)) to decide if The MLC, Inc. should be allowed to continue another five years. In its recent guidance to The MLC, Inc. about artificial intelligence, the Copyright Office correctly took pains to make that distinction in a footnote (footnote 2 to be precise. Remember–always read the footnotes, it’s often where the action is.). This is why it is important that we be clear that The MLC, Inc. does not “own” the data it collects (and that HFA as its vendor doesn’t own it either, a point I raised to Spotify’s lobbyist several years ago). Although it may be a blessing if Congress fired The MLC, Inc. and the new collective had to start from scratch.

But Congress likely would only re-up The MLC, Inc. if it had already decided to extend the statutory license and all its cumbersome and byzantine procedures, proceedings and prohibitions on the freedom of songwriters to collectively bargain. Not to mention an extraordinarily huge thumbs down on the scales in favor of the music user and against the interest of the songwriters. The compulsory license is so labyrinthine and Kafka-esque it is actually an insult to Byzantium, but that’s another story.

Rather than just deciding about who is going to get the job of administering the revenues for every songwriter in the world, maybe there should be a vote. Particularly because songwriters cannot be members of the mechanical licensing collective as currently operated. Congress did not ask songwriters what they thought when the whole mechanical licensing scheme was established, so how about now?

Before the Congress decides to continue The MLC, Inc. many believe strongly that the body should reconsider the compulsory license itself. It is the compulsory license that is the real issue that plagues songwriters and blocks a free market. The compulsory license really has passed its sell by date and it’s pretty easy to understand why its gone so sour. Eliminating the Section 115 license will have many implications and we should tread carefully, but purposefully.

Party Like it’s 1909

First of all, consider the actual history of the compulsory license. It’s over 100 years old, and it was established at a time, believe it or not, when the goal of Congress was to even the playing field between, music users and copyright owners. They were worried about music users being hard done by because of the anticompetitive efforts of songwriters and copyright owners. As the late Register Marybeth Peters told Congress, when Congress created the exclusive right to control reproduction and distribution in 1909, “…due to concerns about potential monopolistic behavior [by the copyright owners], Congress also created a compulsory license to allow anyone to make and distribute a mechanical reproduction of a nondramatic musical work without the consent of the copyright owner provided that the person adhered to the provisions of the license, most notably paying a statutorily established royalty to the copyright owner.”

Well, that ship has sailed, don’t you think?

This is kind of incredible when you think about it today because the biggest users of the compulsory license are those who torture the bejesus out of songwriters by conducting lawfare at the Copyright Royalty Board–the richest corporations in commercial history that dominate practically every moment of American life. In fact, the statutory license was hardly used at all before these fictional persons arrived on the scene and have been on a decades-long crusade to hack the Copyright Act through lawfare ever since. This is particularly true since about 2007 when Big Tech discovered Section 115. (And they’re about to do it again with AI–first they send the missionaries.)

If the purpose of the statutory scheme was to create a win-win situation that floats all boats, you would have expected to see songwriters profiting like never before, right? If the compulsory was so great, what we really needed was for everyone to use Section 115, right? Actually, the opposite has happened, even with decades of price fixing at 2¢ by the federal government. When hardly anyone used the compulsory license, songwriters prospered. When its use became widespread, songwriters suffered, and suffered badly.

Songwriters have been relegated to the bottom of the pile in compensation, a sure sign of no leverage because whatever leverage songwriters may have is taken–there’s that word again–by the compulsory license. I don’t think Google, a revanchist Microsoft, Apple, Amazon or Spotify need any protection from the anticompetitive efforts of songwriters. Google, Amazon, Apple, Microsoft, Spotify are only worried about “monopolistic behavior” when one of them does it to one of the others. The Five Families would tell you its nothing personal, it’s just business.

Yet these corporate neo-colonialists would have you believe that the first thing that happens when the writing room door closes is that songwriters collude against them. (Sounding very much like the Radio Music Licensing Committee–so similar it makes you wonder, speaking of collusion.)

The Five Year Plan

Merck Mercuriadis makes the good point that there is no time like the present to evolve: “In the United States, we have a position of stability for the next five years – at the highest rates paid to songwriters to date – in the evolution of the streaming economy. We are now working towards improving the songwriters’ share of the streaming revenue ‘pie’ yet further and, eventually, getting to a free market.” The clock is ticking on the next five years, a reference to the rate period set by the Copyright Royalty Board in the Phonorecords IV proceeding. (And that five years is a different clock than the five years clock on the MLC which is itself an example of the unnecessary confusion in the compulsory license.)

What would happen if the compulsory license vanished? Very likely the industry would continue its easily documented history of voluntary catalog licenses. The evidence is readily apparent for how the industry and music users handled services that did not qualify for a compulsory license like YouTube or TikTok. However stupid the deals were doesn’t change the fact that they happened in the absence of a compulsory license. That Invisible Hand thing, dunno could be good. Seems to work out fine for other people.

Let’s also understand that there is a cottage industry complete with very nice offices, pensions and rich salaries that has grown up around the compulsory license (or consent decrees for that matter). A cottage industry where collecting the songwriters’ money results in dozens of jobs paying more in a year than probably 95% of songwriters will make, maybe ever. (The Trichordist published an excerpt from a recent MLC tax return showing the highest compensated MLC employees.) Generations of lawyers and lobbyists have put generations of children through college and law school from legal fees charged in the pursuit of something that has never existed in the contemporary music business–a willing buyer and a willing seller. Those people will not want to abandon the very government policy that puts food on their tables, but both sides are very, very good at manufacturing excuses why the compulsory license really must be continued to further humanity.

The even sadder reality is that as much as we would like to simply terminate the compulsory license, there is a certain legitimacy to being clear-eyed about a transition. (An example is the proposals for transitioning from PRO consent decrees–ASCAP’s consent decree has been around a long time, too.) There would likely need to be a certain grandfathering in of services that were pre or post the elimination of the compulsory, but that’s easily done, albeit not without a last hurrah of legal fees and lobbyist invoices. Register Pallante noted in the well-received 2015 Copyright Office study (Copyright and the Music Marketplace at 5) “The Office thus believes that, rather than eliminating section 115 altogether, section 115 should instead become the basis of a more flexible collective licensing system that will presumptively cover all mechanical uses except to the extent individual music publishers choose to opt out.” An opt out is another acceptable stop along the way to liberation, or even perhaps a destination itself. David Lowery had a very well thought-out idea along these lines in the pre-MLC era that should be revisited.

X Day

However, while there is a certain attractiveness to having a plan that the dreaded “stakeholders” and their legions of lobbyists and lawyers agree with, it is crucially important for Congress to fix a date certain by which the compulsory license will expire. Rain or shine, plan or no plan, it goes away on the X Day, say five years from now as Merck suggests. So wakey, wakey.

That transparency drives a wedge into the process because otherwise millions will be spent in fees for profiting from moral hazard and surely the praetorians protecting the cottage industry wouldn’t want that. If you doubt that asking for a plan before establishing X Day would fail as a plan, just look at the Copyright Royalty Board and in particular the Phonorecords III remand. Years and years, multiple court rulings, and the rates still are not in effect. Perseveration is not perseverance, it’s compulsive repetition when you know the same unacceptable result will occur.

But don’t let people tell you that the sky will fall if Congress liberates songwriters from the government mandate. The sky will not fall and songwriters will have a generational opportunity to organize a collective bargaining unit with the right to say no to a deal.

The closest that Congress has come to a meaningful “vote” in the songwriting world is inviting public comments through interventions, rule makings, roundtables and the like–information gathering that is not controlled by the lobbyists. Indeed, it was this very process at the Copyright Royalty Board that resulted in many articulate comments by songwriters and publishers themselves that were clearly quite at odds with what the CRB was being fed by the lobbyists and lawyers. So much so that the Copyright Royalty Judges rejected not only the “Subpart B” settlement reached by the insiders but the very premise of that settlement. Imagine what might happen if the issue of the compulsory license itself was placed upon the table?

Now that songwriters have had a taste of how The MLC, Inc. has been handling their money, maybe this would be a good time to ask them what they think about how things are going. And whether they want to be liberated from the entire sinking ship that is designed to help Big Tech. And you can start by asking how they feel about the $500 million in black box money that is still sitting in the bank account of The MLC, Inc. and has not been paid–with an infuriating lack of transparency. Yet is being “invested” by The MLC, Inc. with less transparency than many banks with smaller net assets.

This “investment” is another result of the compulsory license which has no transparency requirements for such “investments” of other peoples’ money, perhaps “invested” in the very Big Tech companies that fund the The MLC, Inc. That wasn’t a question that was on the minds of Congress in 1909 but it should be today.

Attention Must Be Paid

Let’s face facts. The compulsory license has coexisted in the decimation of songwriting as a profession. That destruction has increased at an increasing rate roughly coincident with the time the Big Tech discovered Section 115 and sent their legions of lawyers to the Copyright Royalty Board to grind down publishers, and very successfully. That success is in large part due to the very mismatch that the compulsory license was designed to prevent back in 1909 except stood on its head waiting for loophole seekers to notice the potential arbitrage opportunity.

The Phonorecords III and IV proceedings at the Copyright Royalty Board tell Congress all they need to know about how the game is played today and how it has changed since 1909, or the 1976 revision of the Copyright Act for that matter. The compulsory license is no longer fit for purpose and songwriters should have a say in whether it is to be continued or abandoned.

We see the Writers Guild striking and SAG-AFTRA taking a strike authorization vote. When was the last time any songwriters voted on their compensation? Maybe never? Voting, hmm. There’s a concept. Now where have I heard that before?

New body to look at musician remuneration – example of how cross party Select Committee working @CommonsCMS and effective campaigning @WeAreTheMU @MrTomGray can achieve progress – the industry must engage positively https://t.co/zDERe5ehoB

“The supreme art of war is to subdue the enemy without fighting.” ― Sun Tzu,The Art of War

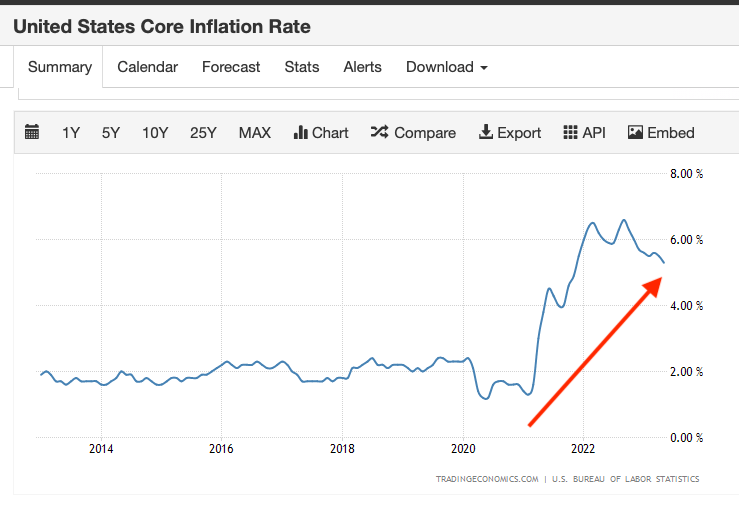

“Core” or “sticky” Inflation

When your business is forced to accept a price that is fixed by the government, keeping a good eye on macroeconomic conditions is part of your job description. This is a particularly important part of your job when government rates are going to be in place for five years at a minimum and affect the entire world. I say “at a minimum” because as we have seen with the Phonorecords III remand, you can be stuck with crappy rates for much longer if you have soulless counterparts. And we do.

There was one bright light in Phonorecords IV. Songwriters will recall how the Copyright Royalty Board rejected the negotiated private settlement by the NMPA, NSAI and the RIAA on physical records and downloads. Due to the outcry from independent music publishers and songwriters not represented by that bargaining group, the CRB then forced a new negotiation. That negotiation resulted in a settlement that raised the statutory mechanical rate for physical records–plus a cost of living adjustment based on a Consumer Price Index.

This inflation adjustment makes the statutory rate for songs on physical goods and downloads similar to the “administrative assessment” for the MLC, Inc. that the Copyright Office put in charge of operating the mechanical licensing collective. (The MLC also has an inflation adjustment in the “assessment” which is the sum paid by services to cover its operating costs.)

Unfortunately, the NMPA and NSAI were unable to–or in any event didn’t–negotiate a cost of living adjustment on streaming mechanicals. There was also an outcry from independent publishers and songwriters not represented by the NMPA and NSAI, but it was too late. Instead they agreed to extend the trickle down royalty structure largely based on revenues rather than share price. Another missed opportunity. Oh well, maybe next time.

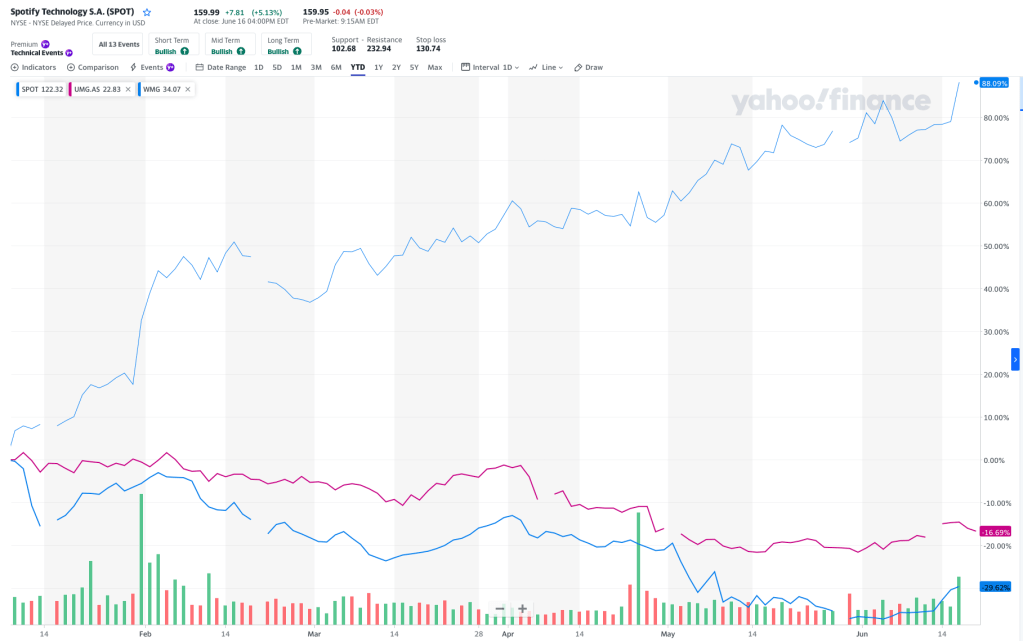

Spotify Share Price Compared to Universal and Warner TTM

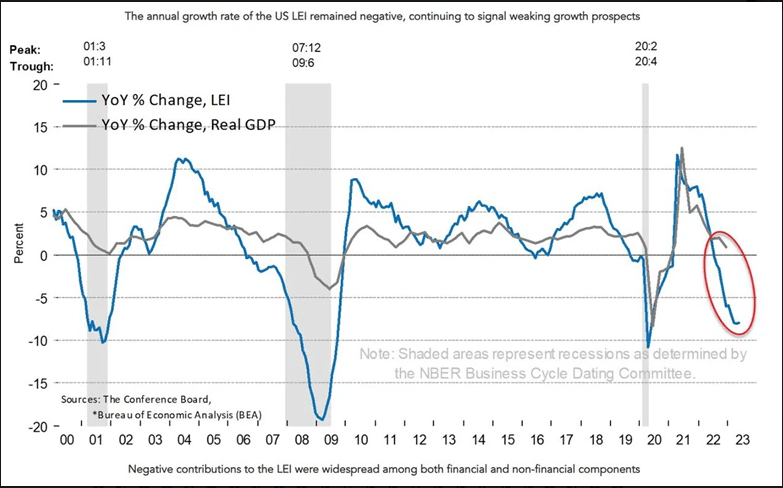

Why is the topic of inflation important right now? When negotiating a five year statutory rate, one might want to study the five year trends in global macroeconomic conditions. For example, consider the Conference Board’s leading economic indicators, everyone else does. That metric has been a good predictor of the economic future. As you’ll see from the chart, we are currently in the 14th straight monthly decline–the longest streak of declines since the Lehman Bros. collapse in 2008. That record was 22 straight months of declines from June 2007 to April 2008.

Given these shockwaves, one might anticipate a recession ahead that highlights the need to preserve purchasing power. One might also want to develop a mindset or theory about how inflation would rot away a fixed rate of return ordered by the government, such as the statutory mechanical rate. Even if one accepted the lack of.a crystal ball, economists make projections all the time, particularly five year, i.e., short term, projections. (Remember that physical mechanicals is a fixed penny rate so inflation rot is easy to measure. Streaming mechanicals is a bizarre formula that changes the result from month to month and so it is easier to hide the mechanical rot from the actual pennies–which almost always start three to four decimal places to the right, anyway.)

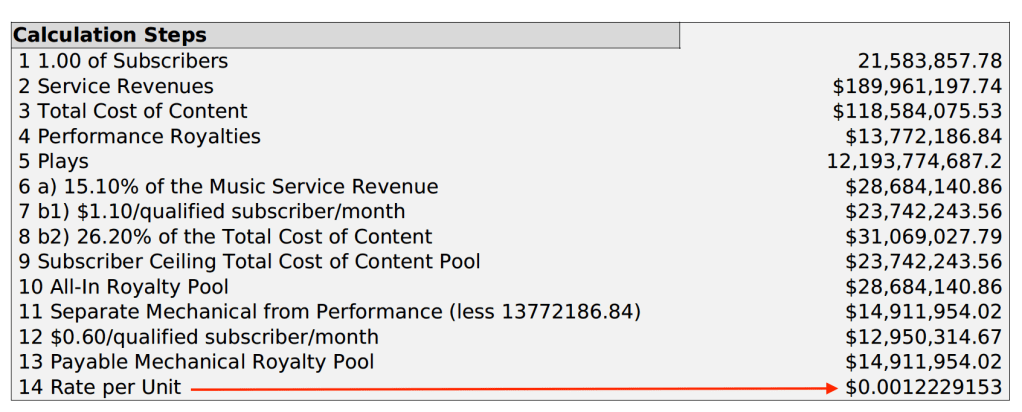

MLC Rate Calculation for a Subscription Service with Rate per Unit for 100% Song Share

How “Sticky” Is Inflation?

Without reading too much into the global macroeconomic situation, it is pretty simple to see that “core” inflation (like housing, but excluding food and energy) is pretty “sticky” meaning it is not decreasing much despite the best efforts of the central banks, including our own Federal Reserve. US core inflation actually increased in the most recent period. How is it in the rest of the world? Consider the BRICS.

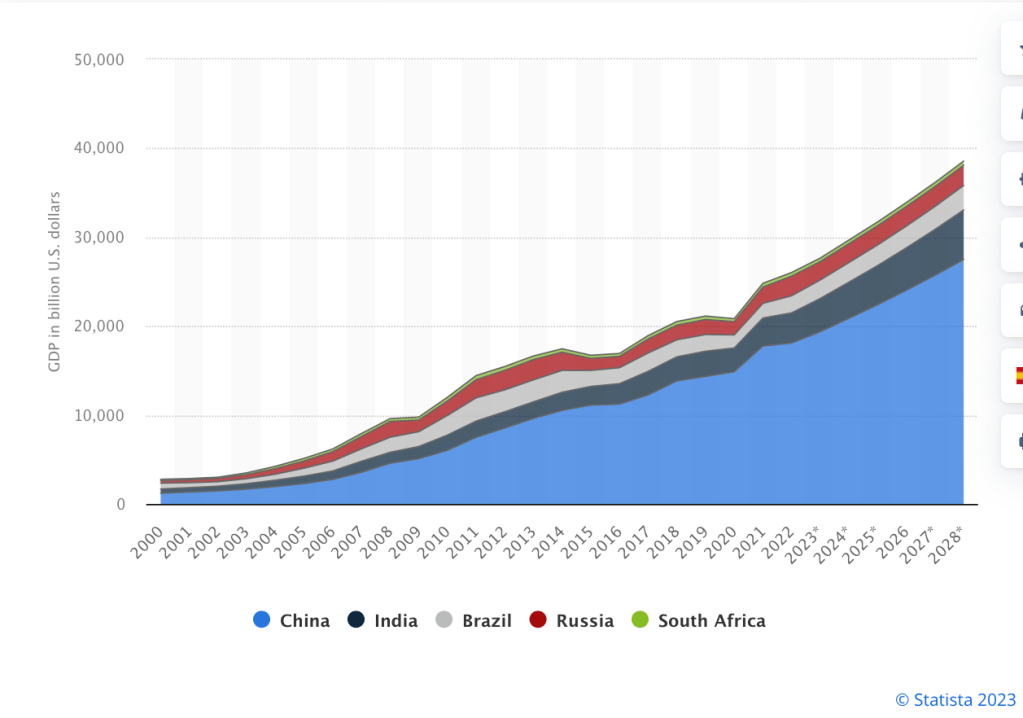

You may have heard of the annual “BRICS” Summit to be held this year on 22 August in Durban, South Africa. BRICS is an acronym of the Brazil, Russia, India, China and South Africa “Partnership for Global Stability”. That’s right, they think they are about the business of “global stability.” Realize that the BRICS bloc combined had a GDP over US$26.03 trillion in 2022, which is slightly more than the United States. When someone tells you who they are, believe them.

Gross Domestic Product of BRICS countries 2000-2028

One of the ways these countries partner for global stability is with currency. A stable currency helps to fight off the inflationary trends associated with the world’s current prime reserve currency, the U.S. dollar. Together these countries account for a substantial amount of world trade and gold reserves. Is it any wonder that BRICS has formed the New Development Bank and the BRICS Contingent Reserve Arrangement as alternatives to Bretton Woods?

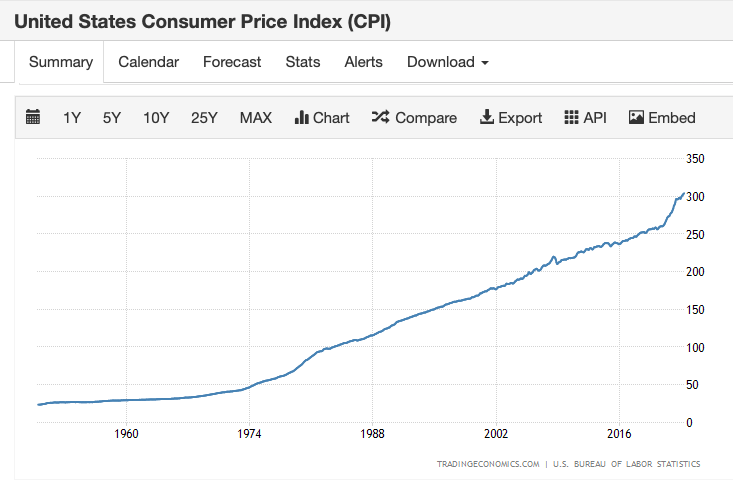

Why would a currency backed by gold be attractive? It stops governments from printing vast quantities of currency for one thing. Pegging a currency like the dollar to the price of gold acts as a brake on government spending which is inflationary. Consider that inflation in the US has steadily risen at nearly a 45 degree slope since around 1972. Now what might have happened in 1972 that could help explain that rise?

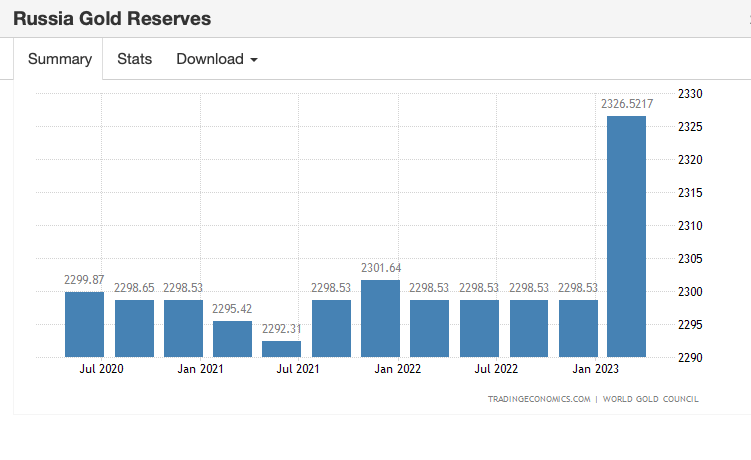

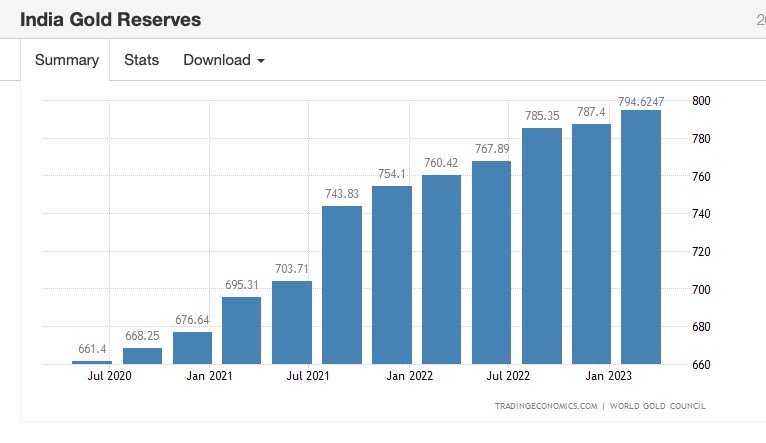

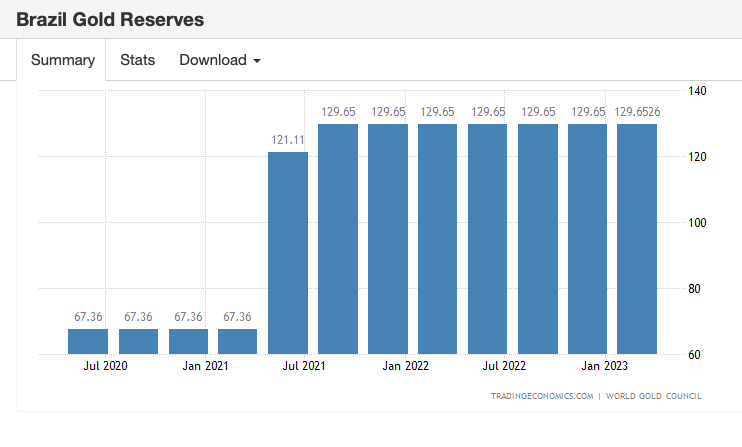

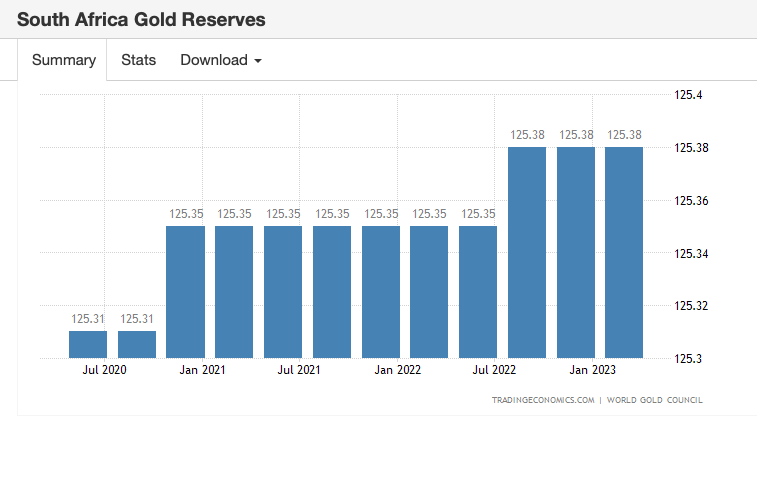

It should not be surprising then that BRICS members have been increasing their gold reserves over the last few years, which is what one would expect to see in advance of forming a currency union pegged to gold. While none of these countries have currency strong enough to challenge the dollar, what if they together were to peg a new currency to gold, what Joseph Sullivan writing in Foreign Policy called a “bric”? What then? No single currency of the BRICs is well suited to replace the dollar, but if a basket of these currencies were pegged to gold, that might be different. If a bric were pegged to gold, we might have a ball game that could displace the dollar as a reserve currency at least in the BRICS countries.

If that was the plan, would you expect to see the BRICS accumulate gold by purchases in the open market to increase their respective gold reserves?

It should also be noted that the weaponization of the US dollar against Russia seems to have had no effect on BRICS. Their global summit will be held in Durban, South Africa recent events in Russia notwithstanding. In fact, it probably is not an overreach to say that not only do these countries not seem to care about being blocked from the SWIFT banking system, the US may find itself blocked from a BRICS banking system and at least given a strong push toward being dislodged as the world’s prime reserve currency.

We’re going to talk about what that means and how it could happen. In a nutshell, the effect on songwriters without inflation protection could be as bad as when the government froze rates from 1909-1978, except in a much more compressed time frame.

There are signs and portents. You’ve probably seen press reports about China making significant commercial deals that promote its renminbi (yuan) currency in large scale sovereign resource and development contracts in bilateral agreements with resource-rich BRICS countries. This is particularly seen with China leveraging its position as the largest crude oil importer and recently surged commerce with France, America’s oldest ally. While there’s a long way to go before the renminbi unseats King Dollar as the world’s prime reserve currency, the point is that China is really trying hard to make that happen which is a first. The downside of losing prime reserve currency status would be as devastating as a war and would result in hyperinflation the likes of which America has never seen.

Of course, we won’t go straight to being Argentina, but there could easily be pressures along the way that would cause our inflation to spike, particularly for those who live off of wages fixed by the government from Social Security to the statutory mechanical royalty rate. This makes fighting for Cost of Living Adjustments all the more important. Just ask the MLC how they protect their administrative assessment.

Sleeping Through the Wars

Let’s go back to February 23, 1998. Like most days, there were some odd coincidences. The U.S. Air Force announced that the iconic RQ-4 Global Hawk drone was cleared to file its own flight plans and fly in civilian air space in the United States. Pam and Tommy got divorced. President William Jefferson Clinton was bogged down in a personal crisis of his own making. Celine Dion was number one with a song from a movie about an unsinkable ship that sunk.

The U.S. was a debtor country, meaning our balance of payments was negative. Howard Stern’s radio show premiered on WAVF in Charleston, South Carolina.

And a fellow most of the world had never heard of declared war on the United States. None of the smart people noticed. We were, after all, Fortress America, etc., etc., and did not pay attention to such things.

Well, it wasn’t quite a declaration of war as we know it. Al-Quds al-Arabi, an Arabic newspaper published in London, printed the full text of a document in Arabic titled “Declaration of the World Islamic Front for Jihad against the Jews and the Crusaders” (now studied at West Point). That document was ostensibly signed by a relatively unknown Saudi financier who masterminded the August bombings of the US embassies in East Africa, and even more obscure leaders of militant Islamist groups in Egypt, Pakistan, and Bangladesh. That Saudi financier was named Usama bin Ladin, and the smart people paid him no mind, not even when he repeated the fatwa on CNN the next year. When someone tells you who they are, believe them.

China Declares a People’s War on the US

Another event happened in 1999, less than a year after UBL’s fatwa. Two colonels in China’s Peoples’ Liberation Army of the Peoples Republic of China published a book in Mandarin entitled Unrestricted Warfare. The title is variously translated as Unrestricted Warfare: Two Air Force Senior Colonels on Scenarios for War and the Operational Art in an Era of Globalization, or the more bellicose Unrestricted Warfare: China’s Master Plan to Destroy America.

You’ve probably never heard of this seminal book. The colonels’ thesis is that it is a mistake for a contemporary great power like China to think of war solely in military terms; war includes an economic, cyber, space, information war (especially social media like TikTok), and other dimensions–including kinetic–depending on the national interest at the time. The colonels offered an extension of Western thinkers with Chinese characteristics.

I think of Unrestricted Warfare as an origin story for China’s civil and military fusion policy, later expressed in various statutes of the Chinese Communist Party that were on full display in the recent TikTok hearing before Congress. Although the book was translated and certain of the cognoscenti read it in Mandarin (see Michal Pillsbury and Gen. Rob Spencer), it was largely unnoticed right next to Bin Ladin.

Except in China–the CCP rewarded the authors handsomely: Qiao Liang retired as a major general in the PLA and Wang Xiangsui is a professor at Beihang University in Beijing following his retirement as a senior Colonel in the PLA (OF-5).

The point of both the 1998 fatwa and Unrestricted Warfare is that no one in the West paid attention. We know where that got us with bin Ladin, there are movies about it.

Fast forward 20 years to May 14, 2019 when the CCP government declared a “people’s war” against the United States as reported in the Pravda of China, the Global Times operated by Xinhua News Agency (the cabinet-level “news” agency run by the CCP):

The most important thing is that in the China-US trade war, the US side fights for greed and arrogance … and morale will break at any point. The Chinese side is fighting back to protect its legitimate interests. The trade war in the US is the creation of one person and one administration, but it affects that country’s entire population. In China, the entire country and all its people are being threatened. For us, this is a real ‘people’s war.’

And “people’s war” has a specific meaning in China:

People’s war, also called protracted people’s war, is a Maoist military strategy. First developed by the Chinese communist revolutionary leader Mao Zedong (1893–1976), the basic concept behind people’s war is to maintain the support of the population and draw the enemy deep into the countryside (stretching their supply lines) where the population will bleed them dry through a mix of mobile warfare and guerrilla warfare.

So in the dimension of unrestricted warfare, what end state would the CCP like to achieve? Bearing in mind that they will avoid a shooting war in favor of the various other dimensions of civil-military fusion and following Sun Tzu’s admonishment to subdue the enemy without fighting. One way would be to impose economic damage on the United States (and really the West) but to do so in a way that does not damage China’s economy or not as much. A prime example might be establishing a military base for electronic and biological warfare in Cuba right before they take Taiwan off the board. Go, not checkers.

Dedollarization

Another way to do that would be by fully or partially displacing the U.S. dollar as the world’s prime reserve currency. And it helps if you think of the U.S. or France the way China does, as a market for Chinese goods. Forget the iconography of the White House or the Élysée Palace; try thinking of the presidents of the U.S. and France as the regional VPs of sales for China, Inc. with Xi Jinping as the Chairman of the Board. That may well be how Xi thinks. It’s certainly how he acts.

What is all this talk from the CCP of breaking morale, people’s war, economic warfare? You mean aside from a few key chapters in Unrestricted Warfare, the manual for the CCP’s hegemony?

First, let’s take an example of the world as it existed on February 8, 2022. And let’s say you are the President of Steppestan, a Central Asian country and CCP buffer state with two natural resources in abundance located a stone’s throw from China’s border: large oil fields and cobalt deposits.

Prior to February 8, 2022 if you wanted to sell your oil, you would almost certainly need to fulfill those trades in U.S. dollars, also called the petrodollar. (President Nixon took us off the gold standard and effectively pegged the dollar to the price of oil when Nurse Ratched wasn’t looking in return for protecting the security of Saudi (see United States-Saudi Arabian Joint Commission on Economic Cooperation.))

So that means that you as President of Steppestan need to find another country, let’s say China, that has dollars to close these oil trades. You’re in luck–China has a bottomless pit of dollars. Well…not bottomless as we will see, but it looks bottomless in February 2022. So Steppestan and China enter into a private “output” deal, a long term contract for Steppestan to provide China with oil for about 30 or 40 years. This contract will require the trades to be closed in dollars unless both sides agree on a different currency. Because Steppestan and China are not going to be pushed around by the American neo-imperialists forever, right? See “people’s war” above.

And since this is an output deal and Steppestan is essentially providing all the oil China can buy from them, the price of oil will be discounted so that China is protected from price fluctuations imposed by OPEC+ (OPEC plus Russia…ahem…and some of the other stans). That means that if OPEC+ decided something, oh say, for example, to cut production and increase the price of gasoline at the pump before a U.S. Presidential election, it won’t affect China at all to the extent of its output deals like they have with Iran.

For the moment then, Steppestan and China agree to denominate their deal in U.S. dollars, which provides you the dollars to do all kinds of other business that also are denominated in dollars. And of course, it’s not just these deals; the Bank for International Settlements shows 90% of this type of transactions were dollar denominated. This is what it means to be the prime reserve currency. It means that your dollars are good everywhere and everyone wants to hold dollars. It means there is a great temptation to continue printing these valuable dollars as if they were inflatable magic gold. It also means that there may be an audience of people who are tired of holding inflated dollars given the trainwreck at the Federal Reserve, fiscal dominance by Congressional appropriators, bank failures, and other alarming events.

Why is the Dollar the King?

There are a few reasons why the dollar has been and currently is the currency of choice for all countries in the world. The U.S. financial industry is pretty well regulated (aside from the 2008 financial crisis, several recent bank failures, massive deficits and high inflation), we have rule of law so don’t have riots in the streets (ahem…), and our currency is stable (aside from devaluing the dollar due to high inflation, high interest rates, and giving up on our manufacturing base despite Mike Rowe’s best efforts).

Now as President of Steppestan, you need to spend those U.S. dollars you got from China in return for oil. You can buy stuff made in America or American assets like real estate or stocks of U.S. companies. You can spend the dollars as fast as you make them, but if you just want to put a little aside, now what? You’ve got a pile of dollars in your central bank that needs to get invested, so where do you put these “reserves” (as in “prime reserve currency” as opposed to “transaction currency”).

Where will you invest your country’s dollar reserves? Well, you want a well-regulated financial system, rule of law, low inflation, all the same things your grandparents wanted with your college fund. But unlike grands, you will want that investment to be liquid, so you can move your money around from instrument to instrument, or raise cash as needed. Plus there’s never been a question that the U.S. would pay its bills and would not refuse to pay if you held those treasury bonds to maturity or pay interest on the debt obligations for any reason. Like if the U.S. government decided Steppestan was a bunch of bad people–it doesn’t only have to do with being able to pay, it could be purposely refusing to pay today in a form of sanction like a blocked account.

For decades, really in the post-WWII era, many countries have chosen U.S. treasury debt, not solely because Hitler was dumb enough to get into a bombing campaign with a country his bombers couldn’t reach, but really because the U.S. ticked all the boxes as a good investment. One could also say that a significant reason was because nobody tried to challenge King Dollar as the world’s prime reserve currency (or in the post WWII era really was able to–see Bretton Woods). That was because nobody wanted to make unrestricted warfare against the U.S. in the economic dimension or declare a people’s war in that dimension. At least not until now.

When Sanctions Backfire

And until February 8, 2022, the U.S. hadn’t really gone after another country the way it went after Russia–which may have a direct effect on the ability of the US to finance deficits. Now remember–due to fiscal dominance by the appropriators, there has never been an effective limit on what Congress could spend because if Congress could pass it, the Federal Reserve would find the money somehow, even if they had to buy toxic assets and print money to buy bonds they couldn’t sell to people like Steppestan or China.

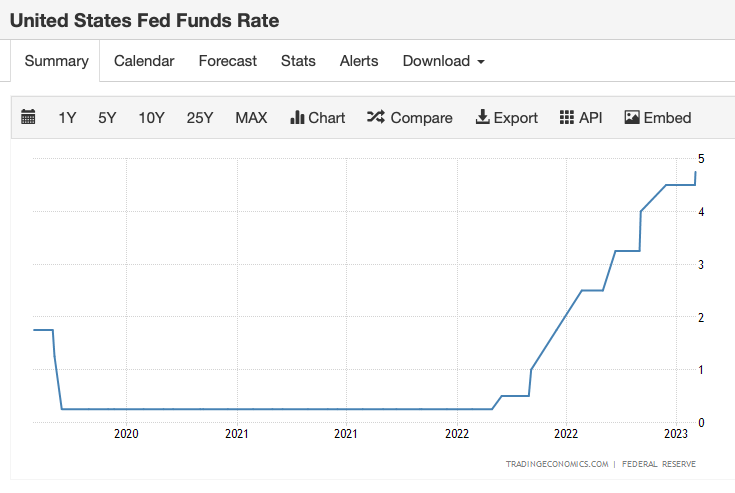

So you could say that the leverage that these other countries have is not just that they hold U.S. debt, it’s that they are willing to continue to buy U.S. debt, even during the Federal Reserve’s Zero Interest Rate Policy (or “ZIRP” which sounds like something General Zog might say). In other words, there were people willing to buy U.S. treasury obligations that paid no interest, and that helped Congress drive up the price of all assets.

You’ll often hear that U.S. treasury debt is backed by the “full faith and credit of the United States”. That’s true. But what does it mean? It sounds like a latter day Nicene Creed or something but there’s actually a very simple secular explanation for this “full faith and credit” thing. Look in the mirror and there it is. The full faith and credit of the United States is you and me and generations yet unborn,

What this does is allow the U.S. to borrow unbelievable amounts of money. When you hear “Congress spent” take a closer look and you’ll see that a good chunk of the dollar figure that follows “spent” was borrowed. Imagine if journalists got fact checked into saying “Congress borrowed”? Do you think that would be a different reaction?

The End State of Economic Warfare

At the moment, emphasis on “moment”, that is all working out, but you can see what would happen if a country wanted to engage in economic warfare against the U.S., or more broadly, the West. All they’d have to do is offer better terms on the transactional currency, like say allowing transactions to close in renminbi (another name for China’s “yuan” which is a unit of renminbi, like sterling and pound). Or in gold denominated brics.

Those better terms could be actual cash terms, or it could be investing in a country like China has done with its Belt and Road Initiative involving debt forgiveness in return for access to a port, train line, or strategic mineral rights like say Steppestan’s other natural resource, cobalt. Never mind that Steppestan mines cobalt using children clawing cobalt out of the ground with their bare hands and who get very sick in terrible work conditions like in the Congo. China’s not worried about that as you can see from the vast amount of pollution and slave labor owned by the CCP. In that way, the sleaze factor in CCP business is right at home in Steppestan, just like they were in Afghanistan after the U.S. abandoned the post.

As if by magic, the Steppestan deals with China are denominated in renminbi, which is part of thousands of transactions, including oil deals with Saudi that are now denominated in the China currency. Every time this happens, it gets closer and closer to shifting the world reserve currency to renminbi and away from dollars.

Let’s say that Steppestan does something that angers the then-current American presidential administration, and all of Steppestan’s dollar denominated reserve accounts are frozen by order of the President. Steppestan is denied access to their own money because they are blocked from the SWIFT system. Steppestan says wait, we bought all that U.S. debt because rule of law, etc., etc., and now you’re just going to take it away from us because you can?

The price you pay for being the world’s prime reserve currency is that you don’t do things like freeze sovereign reserve accounts if you want to stick around. You can be offended, and there are many, many ways that a country like the U.S. can express that offense and even anger. One of them is called SEAL Teams, another is Delta. And there’s a lot of diplomatic steps that don’t cost the blood of our treasure. But is it worth getting knocked off as the prime reserve currency and becoming Argentina? If you think 5% inflation is bad, you ain’t seen nothing yet.

And here’s why. Steppestan is saying, I don’t want to play this game anymore and I don’t need to because I can get almost anything I need from China in renminbi or from the BRICS in the bric, and what I can’t get from them, I can get from somebody else who America has cheesed using renminbi, the bric or some other currency or even good old fashioned barter. Or I could just barter because the Global South has a lot of stuff I need. This is called “sanction proofing”.

Subduing without Fighting

So when you see stories about countries doing deals with China in renminbi, this is what it means. Will the collapse happen tomorrow? Probably not, but it’s the kind of thing that happens gradually and then suddenly. Along the way one possible outcome is that one day when the U.S. goes to borrow the hundreds of billions of dollars it needs that day to keep paying these deficits and say, finance the transfer from fossil fuels to electric along with all the grid upgrades, charging stations and the like that must be acquired, the price won’t be the same because we may have to pay sweeteners to get people to take our debt. (We may have to start doing this now because of inflation, set aside the Federal Reserve quantitative tightening and interest rate rises.)

If it happens, it will happen gradually and then suddenly in the words of Mike Campbell in The Sun Also Rises. It will be hyper inflationary. And it’s a very good reason to keep fighting for cost of living adjustments in any government payment like the statutory mechanical royalty.

The “risk free rate” is often thought of as the rate of interest paid on US government bonds. That interest rate is thought of as risk free because it is backed by the full faith and credit of the United States. Want to know where you can find that full faith and credit? Look in the mirror.

When you ask around about what collective management organizations do with their “black box” monies while they are waiting to match money with songwriters or at least copyright owners, you often hear that the money is invested in very safe instruments, like U.S. treasury bonds. This might be particularly true of CMOs that are required to pay interest on black box because that interest has to come from somewhere.

But–and here it is–but, as we have learned from the Silicon Valley Bank collapse and the number of federal government officials in the mumble tank about why these banks are failing and why they are getting bailed out by, you know, the full faith and credit of the United States, “risk free” seems to be a relative concept. When you buy US government bonds, there are a number of different maturity dates available to you, kind of like buying a certificate of deposit. A common maturity date is the 10-year bond and the two-year bond, both of which were recently down sharply.

But–there is a connection between the interest rate that the bond pays, the price of the bond, and the maturity date of that bond. When bond interest rates increase, the face price tends to decrease. So if you paid $100 for a bond with a interest rate of say .08% and that rate then increased to say 4.5%, the face price of that bond will no longer be $100, it will be less. If that increase happens fairly quickly, you can have difficulty finding a buyer. The good news is that when the Federal Reserve raises the interest rate, there is about as much news coverage of the event as it is theoretically possible to have, both before during and after the rate increase, not to mention the Federal Reserve chair testifying to Congress. It’s very public. Closely watched doesn’t really capture that level of attention.

When bond prices decline, holders only “realize” the loss or gain if they sell the bond unless the bond is marked to market so the firm has to disclose the amount of what the loss would be if they sold the bond. Hence the concept of “unrealized losses,” “maturity risk,” or “interest rate risk.” Some think that US banks currently have $620 billion in unrealized losses due to interest rate risk. And don’t forget, these are your betters. These are the smart people. These are the city fellers.

This interest rate risk issue is not limited to banks, however. It is also present anytime that an entity tasked with caring for other people’s money invests that money in treasury bonds, crypto, or whatever. You don’t have to be Wall Street Bets to end up losing your shirt or something in this environment.

So the point is that the same problem of interest rate risk and unrealized losses could apply to CMOs, such as The MLC, Inc. because of their undisclosed “investment policy” of investing the $424 million of black box they were paid by the services. They don’t disclose what the investment policy is and they don’t disclose their holdings so we don’t really know what has happened, if anything. The money could be perfectly safe.