When the dust settled after the last mechanical royalty rate setting we saw the Copyright Royalty Board approving two different settlements for mechanical royalties. The royalty rate for physical mechanicals and permanent downloads get a significant rate increase and the royalty rate for streaming mechanicals got a theoretical rate increase. However, only physical mechanicals and downloads got both a rate increase and a cost of living adjustment (or “inflation protection”). Streaming mechanicals did not get inflation protection–could have but did not.

This means that the same writers on the same song in the same recording will get inflation protection when that song is sold in physical formats (such as the surging vinyl configuration) or downloads, but will not when that song is sold in streaming formats. What is the logic to this? One difference is that record companies are paying on the physical and download side and the lived experience of record companies necessarily puts them closer to songwriters than the services. And the lived experience of streaming companies is…well, breakfast at Buck’s, Hefner level private jets, warmed bidets and beach volleyball courts at home with imported sand. (Although Sergey Brin has a real beach in his Malibu home. Surf’s up in geekville. Maybe he’ll send DiMA to represent him at the Malibu city council meetings if Malibew-du-bumbum is ready for Silicon Valley style lobbying to decide who can surf Sergey’s beach and the color scheme of their boards. Kind of like the Palo Alto Architectural Review Board with a tan.)

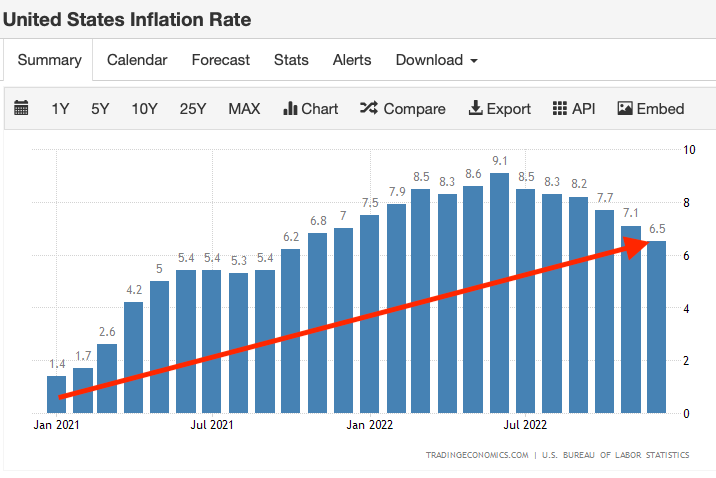

We heard that inflation was transitory, which may prove true–or not. Transitory or not, that’s not an argument against treating songwriters equally on two versions of the same mechanical license; rather, it’s a reason why it should be easy to afford if you cared about sustaining songwriters at least as much as investing in ChatGPT to replace them.

However, in one of the great oopsies of the 21st Century, it doesn’t look much like inflation is all that transitory. Based on some of the posts I wrote starting in 2020, I think we can see that inflation is way worse on the items that count for songwriters like “food at home,” rent, utilities and gasoline. Very often the number of Americans working a job is used to counter the lived experience of the high number of people who believe the economy is tanking. But what about that jobs report? More jobs equals good times, yes? There’s something weird about the math of the jobs report which should make you wonder about whether that’s such a great argument.

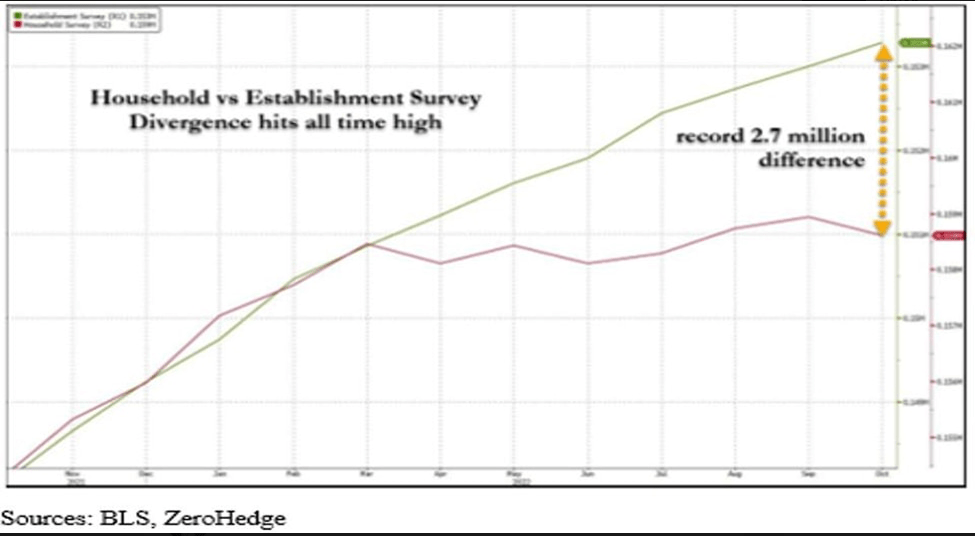

If I still have your attention after the “math” word, there are two standard surveys of the economy used to measure jobs that measure different components of the jobs created in a given measurement period. These data are the “Establishment Payroll Survey” which measures the total number of jobs in the U.S. economy. That’s the number most people refer to with the “jobs report” you hear so much about. (More formally titled the “Current Establishment Statistics (Establishment Survey).”)

There’s another number called the “Household Survey” that measures the total number of jobs per household (more formally titled the Current Population Survey).

Note that the Establishment survey measures all jobs; the Household survey measures jobs per household. If you had two or three jobs, the Household survey would count you as “employed”; the Establishment survey would count the number of jobs you had. Now note that there is currently 2.7 million job difference between the two. Why?

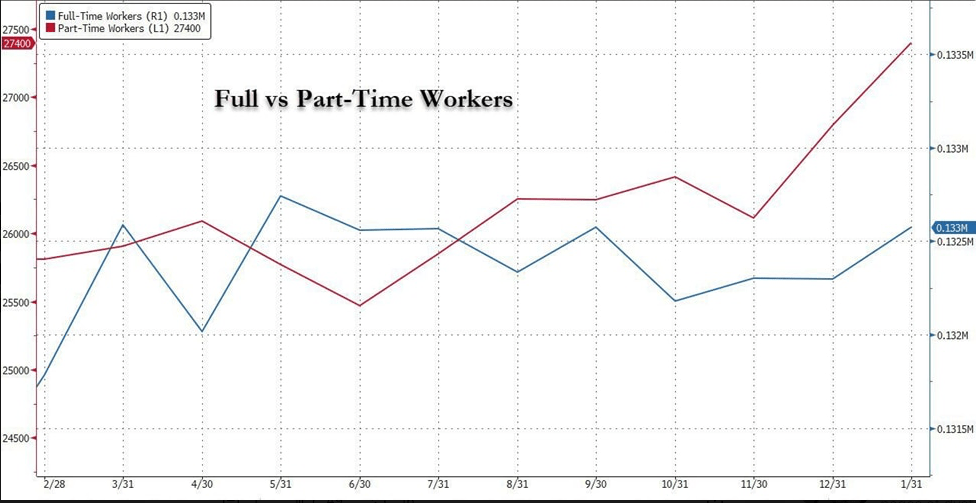

I’m not really sure, but it would appear that there are more jobs than households. That difference may occur from time to time, but it’s quite a big difference at the moment and seems to be a trend that’s confirmed by another statistic: the surge in part-time jobs as shown in this chart:

So what’s missing is how many jobs that are counted in the Establishment survey are held by any one or two household members in the Household survey. If you were to draw the conclusion that every job in the Establishment survey is a full time job held by the primary source of support in a household and that when the Establishment number is rising things are looking up, that may be a leap unsupported by evidence. That may be one of the things you’d want to know if you were trying to predict how well the government’s songwriter royalties would hold their value over the five year rate period.

The sharp increase since June in the number of part time workers may suggest that more people are working multiple jobs and not that more people are working. In fact, the total number of full time workers seems to have declined by a bit over the same period.

That’s not to say that inflation protection is not a serious requirement of everyone who relies on the government for their livelihood. While the inflation rate has declined a bit recently, possibly due to the Federal Reserve abandoning its zero interest rate policy, it is still significant. In my view, nothing in the employment report suggests otherwise and continues to highlight the importance of songwriters being accorded the same inflation protection on streaming as they are on physical and downloads.

Just because the physical rate is paid by the record companies and the streaming rate is paid by the richest corporations in history does not excuse the distinction. Each should be protected equally.