The Copyright Royalty Judges have announced that the new COLA-adjusted minimum statutory rate for 2026 is 13.1¢ for physical and downloads, up from 12.7¢, effective 1/1/26. This is the last year of the Phonorecords IV rate period, so that’s an increase from the 9.1¢ frozen mechanical rate that had been in effect for 15 years.

The adjusted rate stands in stark contrast to the streaming mechanical which not only has been frozen for the entire 5 year rate period, but has actually declined substantially due to Spotify’s bundling silliness. That smooth move has set up what will no doubt be a donnybrook in Phonorecords V, i.e., the next rate proceeding which is due to start any minute now (actually more like January, which is close enough).

It must be said that the reason there’s a rate increase for physical/downloads is due to the efforts of independents who filed two rounds of comments in Phonorecords IV and also the willingness of the labels to be flexible and reasonable. I suspect that has a lot to do with the fact that at the end of the day, we are all in the same business and it’s to everyone’s advantage that songwriters thrive. Obviously, the same cannot be said of the streaming platforms like Spotify that are busy seeding AI tracks with both hands. I really don’t know what business those people think they are in, but it’s not the music business.

When you see artists and songwriters getting starved out of the music business while at the same time fighting over scraps from streaming, that’s unusual. When you see more and more labels caring almost as much about acquiring ever more catalogs rather than helping artists in developing long-term careers, that’s unusual. Why is this becoming the norm? Could it be we are in a “Malthusian trap”?

Remember “nice price” CDs? The budget bin? Top line, mid price, budget price points? That’s called “price differentiation” or “price segmentation.” It’s common in pretty much any consumer good. The idea is that people will pay more for stuff they really want and less money for the nice to haves–the 10 second MBA, buy low sell high. Pretty much any consumer good except–of course–streaming music. One big difference between streaming and physical records is that with streaming, the retailer controls both the wholesale price and the retail price. Want to bet that Wal Mart would just love that model? That should explain why so many artists and especially songwriters are gasping for air. And it should explain why so many are suffering from the streaming pandemic.

Price segmentation in streaming music could be an effective way to avoid the economic concept of the “Malthusian trap.” Simply put, the Malthusian trap occurs when demand for resources outpaces the supply of available resources. This is most likely to happen when buyers with cash exploit sellers who want that cash by using price fixing and market allocation. Like the big pool method of manipulating wholesale prices.

Adopting a more sophisticated approach required by segmentation could allow the music business to move away from the “big pool” program of price controls that has been adopted by every streaming service for both songs and sound recordings. Notice that blowing up the big pool has nothing to do with a compulsory license.

Remember that the “big pool” method allocates a “pie” which is roughly 50ish% of a defined revenue pool calculated each month for the sound recording and about 14ish% of a slightly different revenue pool for the song. Those two “pies” are then divided up based on market share or said another way, popularity. I say “defined revenue” because it is a negotiated number, not all revenue. Want to bet that defined revenue is less than actual revenue? Sure as there’s gambling at Rick’s. So there’s nothing inherent in the pie, and if you wanted to bet that share price and market valuation is not included in that defined revenue, you’d be a winner.

That “big pool” formula is calculated every month (call that Time X or “Tx”) which is essentially:

(Defined Revenue x [Your Total Streams ÷ All Streams]) = Your Revenue @Tx

and then

Your Revenue ÷ Your Streams = Wholesale Price Per Stream

There are a few bells and whistles to this calculation, but it’s easy to see why this method of price fixing is attractive to the streaming services–it’s just that it’s killing the artists and songwriters stuck in the Malthusian trap. It’s also easy to see that unless Your Total Streams are increasing at a greater rate of increase than the increase in All Streams at T1, T2, T3 and so on, or if the Defined Revenue is not increasing at a greater rate than All Streams, then whoever gets the cash called “Your Revenue” is getting screwed blued and tattooed. Why?

Because they cannot control the wholesale price. That sets into motion the big pool downward spiral and that’ downward spiral can also be called the Malthusian Trap in honor of the 18th Century economist Thomas Malthus who you’ve probably have never heard of.

The Malthusian Trap and Faux Democratization of the Denominator

The “Malthusian Trap” occurs in streaming when wholesale prices determined by the “big pool” method of price caps is overtaken by the services’ open invitation for the supposed “democratization of the denominator.” That surge in tracks uploaded to music streaming services is sometimes estimated at 120,000 per day. (I doubt that it’s exactly that number but let’s go with it on the assumption that whatever the correct number is, it’s a lot compared to what a single artist or even a single label would put into commerce.). You are not uploading 120,000 tracks per day. I doubt that the biggest labels are uploading 120,000 tracks per day and they are definitely not uploading 43,800,000 tracks per year. Granted, those tracks are not all streaming, maybe 25% never get played at all.

But that still means that the only number in the big pool formula that is increasing essentially exponentially is the denominator. And when you consider that streaming revenues are growing less than 10% or so annually, the result of the big pool formula is steadily declining. High school algebra, right?

This faux “democratization” uses artists as human shields to put control of wholesale pricing squarely in the hands of streaming services due to wholesale price caps on both the sound recording and song payouts.

When the growth of a service’s sound recording offering outpaces available revenues, the “big pool” method effectively transfers control over wholesale prices from rights holders to services and causes diminishing returns for both labels and publishers. Regardless of the terms of any one artist’s record deal or the convoluted compulsory mechanical royalty for songwriters, these diminishing returns will hit artists, producers and songwriters because returns are diminished to the labels and publishers, particularly on a per-artist basis. Particular deals may make the decline even more or less pronounced, but the race to the bottom is baked into the model. High school algebra.

By introducing a more dynamic and differentiated pricing segmentation model, rights holders could regain control over their own wholesale prices, streaming services might better align revenue payouts with actual usage and consumer preferences. We could all potentially avoid the scenario where a fixed revenue pool gets stretched too thin across an ever-expanding catalog.

It must also be said that because performance on Spotify is closely tied–so to speak–to other commerce such as talent buyers for live shows that constantly check how a new artist has performed on Spotify before giving them a show date, a relatively simple economic decision becomes complex. A demonetized artist may be economically indifferent to continuing to support Spotify by driving fans to the platform, but removing themselves from Spotify may hurt them in booking live shows. So the big pool needs to get blown up for yet another valid, if not actionable, reason.

Blowing Up the Compulsory?

On the songwriter side, there is a sense that what we really need to do is blow up the compulsory license particularly given the reaming songwriters are taking from Spotify’s exploitation of the “bundle” loophole that has foolishly been in the Copyright Royalty Board’s regulations for many, many years. But even so, I suggest that the path dependence of 100-plus years of reliance by a wide variety of music users on the U.S. compulsory mechanical license is unlikely to get “blown up” and abandoned by lawmakers. But what may get “blown up” is the hated “big pool” royalty payable under that compulsory. It may turn out that it’s the big pool that is the culprit, not the compulsory license. (And by the way–be careful what you wish for with all this “blowing up” of the compulsory. You may really not want who comes next.)

Why are we still suffering under this ancient regime? Unfortunately, when the handful of people who forced through Title I of the Music Modernization Act got done with it in 2018, they made bad choices. For example, they had a golden opportunity to do something simple like shorten the rate period from five years to a realistic duration that more closely matches the term of direct license agreements. It’s simply bizarre to use a five year term during a contemporary era marked by relatively high inflation when rates during the 1988-2004 period were adjusted every two years.

They also had a chance to choose between perpetuating the DMV-style model of licensing administration in favor of creating an Apple Store-style model and they went for “more DMV please” like carp on bait. And here we are, more screwed than ever. Gee thanks, thought leaders!

Understanding the Malthusian Trap in Streaming

In the current “big pool” model, royalties are divided among artists based on the proportion of streams their music receives relative to the total number of streams on the platform. Songwriters are paid in a similar version of the “big pool.” This system leads to diminishing payouts as the catalog expands and the user base grows, since:

The total revenue pool remains relatively static due to slowing streaming growth and frozen subscription prices, while the denominator (the total number of streams) grows larger;

2. The more content added to the platform, the less valuable each individual stream becomes (regardless of particular artist deals); and

3. Artists or songwriters with fewer streams get demonetized by Spotify or are paid but fall outside the mainstream struggle to receive meaningful payouts.

The “Malthusian trap,” in this context means there is an imbalanced relationship between increasing content and relatively static revenue pools. That imbalance results in declining payouts over time for artists and songwriters. This especially true for those creators whose total streams (the numerator in the ratio) are relatively constant or declining due to falling off in fan engagement for whatever reason (including bands that break up or artists who pass away).

In other words, the big pool’s fixed cap on aggregated streaming prices creates its own scarcity despite the infinite shelf space of a streaming service. (See Chris Anderson’s rather tarnished “long tail” theory that still reigns supreme at streaming services which demonstrates once again there is no free lunch.)

“Malthusian” refers to the sometimes controversial ideas of Thomas Robert Malthus (1766–1834) the British economist, scholar, and demographer, best known for his theories on population growth and its relationship to resources, particularly food. His most influential work is “An Essay on the Principle of Population” (1798), where he argued that populations tend to grow exponentially, while food production grows at a much slower, linear rate.

This mismatch, according to Malthus, would eventually lead to overpopulation and resource scarcity, resulting in widespread poverty, famine, and social instability. Malthus called this the “surplus population” or what the AI accelerationists call “useless eaters.” Surplus population leads to famine just like streaming leads to Discovery Mode and demonetization. Mr. Malthus has a fairly gloomy view of the world, so no Spotify stock options for him. He wouldn’t have his pompoms out as a streaming cheerleader our Thomas, but his ideas are very relevant to the streaming analysis.

Key Concepts of Malthusian Theory: Also see Malthus critic Charles Dickens (“may I have some more”), England’s response to the Irish potato famine and Gangs of New York.

Exponential Population Growth: Malthus believed that if left unchecked, populations grow exponentially (doubling every 25 years), which would outpace the resources needed to sustain them. Comparatively, the total number of tracks on Spotify has doubled approximately every four years. (This is like Sergei’s Corollary to Moore’s Law–royalties decline 50% with every two year increase in computing power.)

Limited Food Supply: Malthus argued that food production could only grow at an arithmetic (linear) rate because of the finite land, labor, and capital available to produce it. Over time, the availability of food per capita would diminish just like the per-stream rate on streaming platforms–that’s why Spotify continues to deny a per-stream rate even exists (ludicrous propaganda). That is, populations tend to increase geometrically (2, 4, 8, 16 …), whereas food reserves grow arithmetically (2, 3, 4, 5 …). I’d say this is like a vast number of under performing recordings lead to competition for the artificially capped revenue under “big pool” and the relatively frozen subscription prices. This helps to explain Daniel Ek’s–very Malthusian–comment that artists need to work harder to keep up which was straight out of Oliver Twist.

The Malthusian Trap: The theory suggests that any improvements in living standards (through better agriculture, technology, or economic progress) would eventually lead to population growth, which would, in turn, bring the standard of living back down to subsistence levels. Essentially, population pressure would cause periodic famines, diseases, or wars–you know, demonetization–that would control population size and maintain balance with available resources. The trap helps to explain why we need to blow up the big pool model and its fixed wholesale prices.

Preventive and Positive Checks: Malthus identified two types of checks on population growth:

Preventive checks: These are voluntary actions people can take to limit population growth, such as delayed marriage and celibacy. In the streaming analogy, this would occur if Spotify were to limit the number of royalty bearing tracks (like demonetizing under 1,000 streams).

Positive checks: These occur when the population exceeds the capacity for sustenance, leading to famine, disease, and mortality, which ultimately reduce the population. In the streaming analogy, this occurs when artists or songwriters quit the music business or abandon streaming platforms. Given the close ties between traction on Spotify and validation for talent buyers, for example, it is unlikely that a working artist could abandon the platform entirely no matter how much it costs them to stay on Spotify–although there are limits.

Can Price Segmentation Address the Malthusian Trapin Streaming?

Price segmentation allows streaming platforms to differentiate pricing based on different user segments, content types, or usage behaviors, which can provide several key benefits to avoid the Malthusian trap. We’ll see if the thought leaders have some other suggestions–that I cynically (I admit) think are most likely to be continuing to put bandaids on the status quo.

There is loose talk these days about something called “blowing up the compulsory” license for songs in the US under Section 115 of the Copyright Act. This is odd. It is particularly odd given that a lot of the same people now trying to find a parade to get in front of were the very people who championed–barely five years ago–the bizarre and counterintuitive Title I of the Music Modernization Act (aka the Harry Fox Preservation Act). Title I was the part of the MMA legislation that created the Mechanical Licensing Collective and invited Big Tech even further into our house. (Don’t forget there were other important parts of what became the MMA that were actually well thought out and helpful.)

The geniuses who came up with Title I are also the same people who refused to include artist pay for radio play in the package of bills that became the sainted MMA back in 2018. So at the very least before anyone takes seriously any plan to “blow up the compulsory”, the proponents who want buy-in on that change in policy can get right with history and atone by declaring their support–vocal support–for artist pay for radio play. This would be supporting the American Music Fairness Act recently introduced in this Congress by our allies Senator Blackburn and Rep. Issa and their colleagues.

It is important to realize that “blowing up the compulsory” cannot be a shoot-from-the-hip reaction to Spotify taking advantage of the gaping bundling loophole left wide open in the highly negotiated streaming mechanical settlement under Phonorecords IV. There are too many factors in that big a shock to the system. Songwriters around the world should not get caught up in throwing toys out of the pram along with 100 years of licensing practice just because they made a bad deal. This is particularly true given that the smart people handed over the industry’s bargaining leverage against Big Tech as part of the MMA debacle in return for what? Allowing Spotify’s public stock offering to go forward on schedule? Another genius move by the smart people. I wonder what they got out of that deal? I mean this stock offering, you know, the one that made Daniel Ek a billionaire:

A good thing we didn’t let another MTV build their business on our backs.

It is also important to recognize the obvious–the compulsory is not really a compulsory, it’s a compulsory in the absence of a negotiated direct agreement such as the one that Universal recently made with Spotify. Copyright owners have always been free to make direct deals with music users. The compulsory is not just a license, it is also a compulsory rate that casts a long commercial shadow over even the big industry negotiations and certainly over rates in the rest of the world.

And for reasons of historical accident those rates are not determined in Nashville, or New York, or Los Angeles, or even Austin, but rather in Washington, DC in front of the Copyright Royalty Board–an agency that itself is on pretty shakey Constitutional grounds after a Supreme Court decision in the 2020 Term. So if we’re going to “blow up the compulsory”, maybe a good place to start is not having lobbyists make these decisions.

Even if the former opponents of artist pay for radio play come to their senses and support fundamental fairness for artists, that’s just a good start. We have to acknowledge that “blowing up the compulsory” is not going to be well received by the streaming services for starters. (Not to mention the labels.) Those would be the same streaming services that the smart people invited into our house by means of underwriting the costs of the Mechanical Licensing Collective.

I don’t know how others feel about it, but I for one am not inclined to go to the mattresses to assuage the multimillion dollar whiplash that the services must feel. We should understand that Big Tech are being asked to abandon their intensely successful lobbying campaign that led songwriters and publishers right down the garden path with the MMA. Not to mention the millions they have spent creating the MLC so the MLC could pass through some of those monies to HFA.

Before Congress goes along with blowing up Title I of the MMA, they’re probably going to want an explanation of why this isn’t just another fine mess in a long string of fine messes. That will probably involve a study by the Copyright Office like the one the Office was asked by a songwriter to conduct as part of the MLC’s five year review (but declined to undertake at that time). Fortunately that five year review is still dragging on over a year after it started so this would be a perfect time to launch that study. Perhaps Congress will instruct them to do so? At this rate, it will be time for a new five year review before the first one gets completed, so as usual, time is not a factor.

Even if the services and Congress would go along with “blowing up the compulsory” what does that mean for the MLC and the sainted musical works database? Remember, the lack of a database was the excuse that services relied on for years for their sloppy licensing practices. The database was the fig leaf they needed to avoid iterative infringement lawsuits for their failure–or the failure of the services outside licensing consultants.

It also must be said that the services were invited by the same smart people to spend millions on setting up the MLC. In fairness they have a right to get the benefit of the bargain they were invited to make by the same people who now want to blow it up. Or get their money back. Plus they have to like the leverage they were handed to go to Congress and complain, and complain quite believably with great credibility.

And perhaps most important of all is what happens to the $1.2 BILLION in publicly traded securities that the MLC announced on their 2023 tax return that they are (or at least were) holding in their name? Does that get blown up, too?

We are rapidly approaching the next rate-setting proceeding before the three-judge panel at the Copyright Royalty Board for the royalty payable to copyright owners (and ultimately to songwriters) for exploitations of songs. These proceedings set rates for the next five year period and are numbered to tell them apart. The last proceeding, for example, was styled “Phonorecords IV” or sometimes “CRB 4” for those who struggle with long words. (Using the “CRB” acronym instead of “Phonorecords” is actually misleading because the CRB sets a number of rates.)

The proceedings will likely be divided in two: One proceeding for songs exploited in physical records like vinyl, CDs and permanent downloads and one proceeding for streaming mechanicals. These hearings are simultaneous and not sequential, so each hearing will be conducted side by side.

One reason for these simultaneous hearings is that the participants in each of the proceedings differ–the physical/download participants are songwriters and publishers on one side and the record companies on the other. The streaming participants are (often) the same songwriters and publishers on one side, but the streaming services are on the other.

The participants are incented to reach a voluntary settlement that they then present to the Copyright Royalty Judges for approval. The settlement negotiations are largely conducted in secret and no one on the songwriter side except a couple of participants knows anything about the terms of the settlement until it is presented to the Judges and the Judges make it public.

At this point, the Judges are required to entertain comments from the public as to whether the public supports the settlement (as required under a federal law applicable to all of the administrative state agencies from the Environmental Protection Agency to the Social Security Administration to the Copyright Royalty Board).

No matter how much some of the publishers would like to spin it, it is this public comment step where it all began to fall apart during the last proceeding styled “Phonorecords IV”, particularly over the “frozen mechanicals” issue. Signally, this disintegration of the initial physical/downloads “settlement” attracted a prairie fire of public comments that rejected the authority of the NMPA and NSAI to speak on behalf of all songwriters and publishers and also rejected the side deal that these groups had negotiated with the labels. The Judges listened, and the Judges rejected that settlement–I believe for the first time in the history of the rate setting proceedings.

The same was not true of the streaming mechanicals piece, however. I never did read a well-reasoned explanation for why participants lacked authority to speak on behalf of all songwriters, i.e., beyond their own members, in the frozen mechanicals proceeding, but that authority could not be questioned in the streaming proceeding. It should have been apparent to anyone paying attention that any consensus behind the time-encrusted “Big Pool” royalty calculation method for streaming mechanicals was rapidly crumbling apart. The Judges’ “39 Steps” royalty calculation is as mysterious as a Hitchcock movie and many did not trust it. And more importantly for our discussion today–still do not trust it at all.

As we approach Phonorecords V, there are some fundamental questions that all involved need to be asking themselves. The first is whether we want to go back to the same tired process of secret meetings with the big reveal resulting in public hostilities in the comments–against what is ostensibly our side. This before we even get to the negotiation with the other side.

The powers that be had the chance over the last few years to bring in some different viewpoints. Had they done so, they would have both diffused the inevitable collision, but could also have gotten the benefit of those viewpoints when there was still time to build alliances. There’s an idea–an integrative negotiation with a collaborative outcome.

Another fundamental question is whether we can reach a fairly quick deal with the labels on the physical/download side so that all concerned can turn their attention to bringing the streaming rates into some semblance of reality. Because the songwriters did such a persuasive job of raising the frozen mechanicals rates from 9.1¢ to 12¢ plus a COLA, that minimum statutory rate has now increased to 12.7¢. Given current inflation projections, it’s likely that the statutory rate will increase to about 13¢ and change by the end of 2026.

If a settlement could be reached quickly, it would not surprise me if someone came up with the idea of simply taking the then-extant minimum rate (for 2027) as the new base rate for the first year of Phonorecords V (2028) plus extending the annual COLA to protect songwriters in the out-years of PR V. Wherever the actual penny rates end up, if the songwriters and labels could reach an agreement quickly, it would save a bunch of effort and allow everyone to turn their attention to the streaming rates.

I wonder if it’s even possible to reach a negotiated settlement with the streaming services on the streaming mechanical. The entire concept of the “Big Pool” royalty rate is failing for streaming on both the sound recording and the song side of the deals. It was, frankly, a silly idea to begin with–and that takes us back to the beginning of streaming when deals were poorly negotiated with little to no accountability because physical still paid the bills. The general idea was that “superfans” would rule according to Thomas Hesse in Billboard who was around at the time: “If you get to superfans, who listen to music all the time, you get to all the money — not just from those people, but you get all the money from everybody.” The reality is that you can replace “superfans” with “superstars” or more simply, “market share”, and you would have a much better understanding of the “Big Pool” concept. The Big Pool is actually just a hyper efficient marketshare distribution of a pool of money.

What Spotify has demonstrated with their short sighted move on bundling is simply all the reasons why they are disliked and untrustworthy. They said the quiet part out loud–we have no idea what we are doing in this business but we–and not songwriters or musicians–are getting stupid rich at it. It is unlikely that anyone is going to welcome more of the same in Phonorecords V.

What is becoming apparent to an increasing number of songwriters is that there is one metric that matters to Spotify’s CEO–stock market valuation. That is what has made him a billionaire. That is what has made plenty of people at Spotify into millionaires. That is also the one metric that songwriters and artists have never participated in. Our negotiators have had their eye on the wrong ball.

I say if we’re going to spend millions on the government’s rate proceedings anyway, let’s get something for it for a change, shall we?

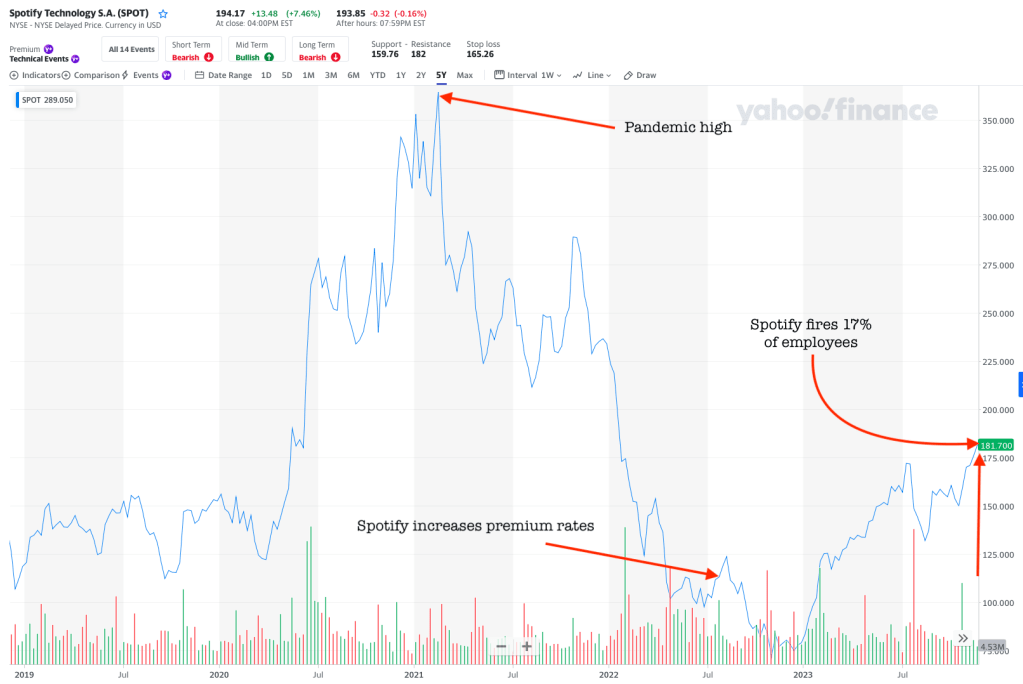

Harsh? Not really, at least not from a share price point of view. Spotify’s all time highest share price was during the COVID pandemic.

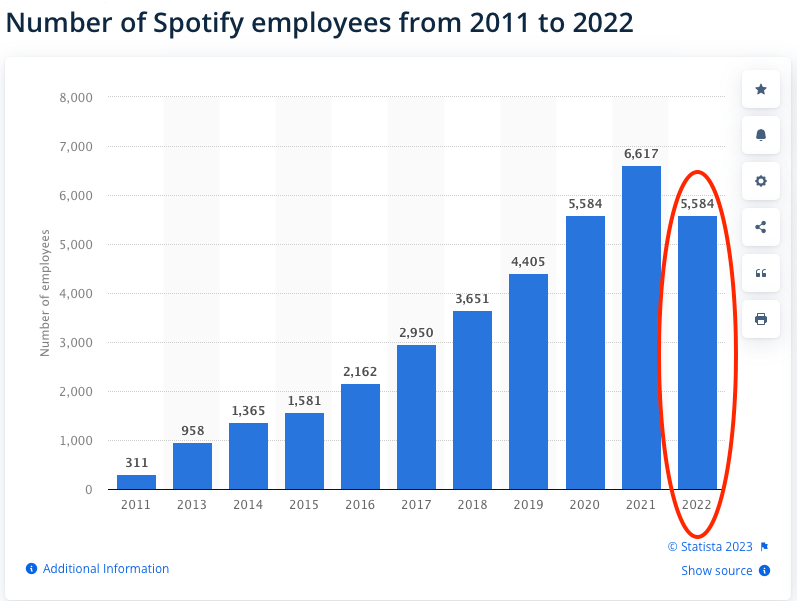

Spotify CEO Daniel Ek and the press tells us that Spotify is cutting 1,500 jobs which works out to about 17% of Spotify employees. Which works out to a pre-layoff workforce of 8,823. So let’s start there—that workforce number seems very high and is completely out of line with some recent data from Statista which is usually reliable.

If Statista is correct, Spotify employed 5,584 as of last year. Yet somehow Spotify’s 2023 workforce grew to 9200 according to the Guardian, fully 2/3 over that 2022 level without a commensurate and offsetting growth in revenue. That’s a governance question in and of itself.

Why the layoffs? The Guardian reports that Spotify CEO Daniel Ek is concerned about costs. He says “Despite our efforts to reduce costs this past year, our cost structure for where we need to be is too big.” Maybe I missed it, but the only time I can recall Daniel Ek being vocally concerned about Spotify’s operating costs was when it came to paying royalties. Then it was full-blown poor mouthing while signing leases for very expensive office space in 4 World Trade Center as well as other pricy real estate, executive compensation and podcasters like Harry & Meghan.

Over the last two years, we’ve put significant emphasis on building Spotify into a truly great and sustainable business – one designed to achieve our goal of being the world’s leading audio company and one that will consistently drive profitability and growth into the future. While we’ve made worthy strides, as I’ve shared many times, we still have work to do. Economic growth has slowed dramatically and capital has become more expensive. Spotify is not an exception to these realities.

Which “economic growth” is that?

But, he is definitely right about capital costs.

Still, Spotify’s job cuts are not necessarily that surprising considering the macro economy, most specifically rents and interest rates. As recently as 2018, Spotify was the second largest tenant at 4 WTC. Considering the sheer size of Spotify’s New York office space, it’s not surprising that Spotify is now sublettingfive floors of 4 WTC earlier this year. That’s right, the company had a spare five floors. Can that excess just be more people working at home given Mr. Ek’s decision to expand Spotify’s workforce? But why does Spotify need to be a major tenant in World Trade Center in the first place? Renting the big New York office space is the corporate equivalent of playing house. That’s an expensive game of pretend.

Remember that Spotify is one of the many companies that rose to dominance during the era of easy money in response to the financial crisis that was the hallmark of quantitative easing and the Federal Reserve’s Zero Interest Rate Policy beginning around 2008. Spotify’s bankers were able to fuel Daniel Ek’s desire to IPO and cash out in the public markets by enabling Spotify to run at a loss because money was cheap and the stock market had a higher tolerance for risky investments. When you get a negative interest rate for saving money, Spotify stock doesn’t seem like a totally insane investment by comparison. This may have contributed to two stock buy-back programs of $1 billion each, Spotify’s deal with Barcelona FC and other notorious excesses.

As a great man said, don’t confuse leverage for genius. It was only a matter of time until the harsh new world of quantitative tightening and sharply higher inflation came back to bite. For many years, Spotify told Wall Street a growth story which deflected attention away from the company’s loss making operations. A growth story pumps up the stock price until the chickens start coming home to roost. (Growth is also the reason to put off exercising pricing power over subscriptions.) Investors bought into the growth story in the absence of alternatives, not just for Spotify but for the market in general (compare Russell Growth and Value indexes from 2008-2023). Cutting costs and seeking profit is an example of what public company CEOs might do in anticipation of a rotational shift from growth to value investing that could hit their shares.

Never forget that due to Daniel Ek’s super-voting stock (itself an ESG fail), he is in control of Spotify. So there’s nowhere to hide when the iconography turns to blame. It’s not that easy or cheap to fire him, but if the board really wanted to give him the heave, they could do it.

I expect that Ek’s newly found parsimony will be even more front and center in renegotiations of Spotify’s royalty deals since he’s always blamed the labels for why Spotify can’t turn a profit. Not that WTC lease, surely. This would be a lot more tolerable from someone you thought was actually making an effort to cut all costs not just your revenue. Maybe that will happen, but even if Spotify became a lean mean machine, it will take years to recover from the 1999 levels of stupid that preceded it.

Hellooo Apple. One big thinker in music business issues calls it “Spotify drunk” which describes the tendency of record company marketers to focus entirely on Spotify and essentially ignore Apple Music as a distribution partner. If you’re in that group drinking the Spotify Kool Aid, you may want to give Apple another look. One thing that is almost certain is that that Apple will still be around in five years.

Just sayin.

Mechanicals on Physical and Downloads Get COLA Increase; Nothing for Streaming

Recall that the “Phonorecords IV” minimum mechanical royalties paid by record companies on physical and downloads increased from 9.1¢ to 12¢ with an annual cost of living adjustment each year of the PR IV rate period. The first increase was calculated by the Copyright Royalty Judges and was announced this week. That increase was from 12¢ to 12.40¢ and is automatic effective January 1, 2024.

Note that there is no COLA increase for streaming for reasons I personally do not understand. There really is no justification for not applying a COLA to a government mandated rate that blocks renegotiation to cover inflation expectations. After all, it works for Edmund Phelps.

The Federal Trade Commission on Copyright and AI

The FTC’s comment in the Copyright Office AI inquiry shows an interesting insight to the Commission’s thinking on some of the same copyright issues that bother us about AI, especially AI training. Despite Elon Musk’s refreshing candor of the obvious truth about AI training on copyrights, the usual suspects in the Copyleft (Pam Samuelson, Sy Damle, etc.) seem to have a hard time acknowledging the unfair competition aspects of AI and AI training (at p. 5):

Conduct that may violate the copyright laws––such as training an AI tool on protected expression without the creator’s consent or selling output generated from such an AI tool, including by mimicking the creator’s writing style, vocal or instrumental performance, or likeness—may also constitute an unfair method of competition or an unfair or deceptive practice, especially when the copyright violation deceives consumers, exploits a creator’s reputation or diminishes the value of her existing or future works, reveals private information, or otherwise causes substantial injury to consumers. In addition, conduct that may be consistent with the copyright laws nevertheless may violate Section 5.

We’ve seen unfair competition claims pleaded in the AI cases–maybe we should be thinking about trying to engage the FTC in prosecutions.

Congress is considering whether to renew The MLC, Inc.‘s designation as the mechanical licensing collective. If that sentence seems contradictory, remember those are two different things: the mechanical licensing collective is the statutory body that administers the compulsory license under Section 115. The MLC, Inc. is the private company that was “designated” by Congress through its Copyright Office to do the work of the mechanical licensing collective. This is like the form of a body that performs a function (the mechanical licensing collective) and having to animate that form with actual humans (The MLC, Inc.), kind of like Plato’s allegory of the cave, shadows on the wall being what they are.

Congress reviews the work product of The MLC, Inc. every five years (17 USC §115(d)(3)(B)(ii)) to decide if The MLC, Inc. should be allowed to continue another five years. In its recent guidance to The MLC, Inc. about artificial intelligence, the Copyright Office correctly took pains to make that distinction in a footnote (footnote 2 to be precise. Remember–always read the footnotes, it’s often where the action is.). This is why it is important that we be clear that The MLC, Inc. does not “own” the data it collects (and that HFA as its vendor doesn’t own it either, a point I raised to Spotify’s lobbyist several years ago). Although it may be a blessing if Congress fired The MLC, Inc. and the new collective had to start from scratch.

But Congress likely would only re-up The MLC, Inc. if it had already decided to extend the statutory license and all its cumbersome and byzantine procedures, proceedings and prohibitions on the freedom of songwriters to collectively bargain. Not to mention an extraordinarily huge thumbs down on the scales in favor of the music user and against the interest of the songwriters. The compulsory license is so labyrinthine and Kafka-esque it is actually an insult to Byzantium, but that’s another story.

Rather than just deciding about who is going to get the job of administering the revenues for every songwriter in the world, maybe there should be a vote. Particularly because songwriters cannot be members of the mechanical licensing collective as currently operated. Congress did not ask songwriters what they thought when the whole mechanical licensing scheme was established, so how about now?

Before the Congress decides to continue The MLC, Inc. many believe strongly that the body should reconsider the compulsory license itself. It is the compulsory license that is the real issue that plagues songwriters and blocks a free market. The compulsory license really has passed its sell by date and it’s pretty easy to understand why its gone so sour. Eliminating the Section 115 license will have many implications and we should tread carefully, but purposefully.

Party Like it’s 1909

First of all, consider the actual history of the compulsory license. It’s over 100 years old, and it was established at a time, believe it or not, when the goal of Congress was to even the playing field between, music users and copyright owners. They were worried about music users being hard done by because of the anticompetitive efforts of songwriters and copyright owners. As the late Register Marybeth Peters told Congress, when Congress created the exclusive right to control reproduction and distribution in 1909, “…due to concerns about potential monopolistic behavior [by the copyright owners], Congress also created a compulsory license to allow anyone to make and distribute a mechanical reproduction of a nondramatic musical work without the consent of the copyright owner provided that the person adhered to the provisions of the license, most notably paying a statutorily established royalty to the copyright owner.”

Well, that ship has sailed, don’t you think?

This is kind of incredible when you think about it today because the biggest users of the compulsory license are those who torture the bejesus out of songwriters by conducting lawfare at the Copyright Royalty Board–the richest corporations in commercial history that dominate practically every moment of American life. In fact, the statutory license was hardly used at all before these fictional persons arrived on the scene and have been on a decades-long crusade to hack the Copyright Act through lawfare ever since. This is particularly true since about 2007 when Big Tech discovered Section 115. (And they’re about to do it again with AI–first they send the missionaries.)

If the purpose of the statutory scheme was to create a win-win situation that floats all boats, you would have expected to see songwriters profiting like never before, right? If the compulsory was so great, what we really needed was for everyone to use Section 115, right? Actually, the opposite has happened, even with decades of price fixing at 2¢ by the federal government. When hardly anyone used the compulsory license, songwriters prospered. When its use became widespread, songwriters suffered, and suffered badly.

Songwriters have been relegated to the bottom of the pile in compensation, a sure sign of no leverage because whatever leverage songwriters may have is taken–there’s that word again–by the compulsory license. I don’t think Google, a revanchist Microsoft, Apple, Amazon or Spotify need any protection from the anticompetitive efforts of songwriters. Google, Amazon, Apple, Microsoft, Spotify are only worried about “monopolistic behavior” when one of them does it to one of the others. The Five Families would tell you its nothing personal, it’s just business.

Yet these corporate neo-colonialists would have you believe that the first thing that happens when the writing room door closes is that songwriters collude against them. (Sounding very much like the Radio Music Licensing Committee–so similar it makes you wonder, speaking of collusion.)

The Five Year Plan

Merck Mercuriadis makes the good point that there is no time like the present to evolve: “In the United States, we have a position of stability for the next five years – at the highest rates paid to songwriters to date – in the evolution of the streaming economy. We are now working towards improving the songwriters’ share of the streaming revenue ‘pie’ yet further and, eventually, getting to a free market.” The clock is ticking on the next five years, a reference to the rate period set by the Copyright Royalty Board in the Phonorecords IV proceeding. (And that five years is a different clock than the five years clock on the MLC which is itself an example of the unnecessary confusion in the compulsory license.)

What would happen if the compulsory license vanished? Very likely the industry would continue its easily documented history of voluntary catalog licenses. The evidence is readily apparent for how the industry and music users handled services that did not qualify for a compulsory license like YouTube or TikTok. However stupid the deals were doesn’t change the fact that they happened in the absence of a compulsory license. That Invisible Hand thing, dunno could be good. Seems to work out fine for other people.

Let’s also understand that there is a cottage industry complete with very nice offices, pensions and rich salaries that has grown up around the compulsory license (or consent decrees for that matter). A cottage industry where collecting the songwriters’ money results in dozens of jobs paying more in a year than probably 95% of songwriters will make, maybe ever. (The Trichordist published an excerpt from a recent MLC tax return showing the highest compensated MLC employees.) Generations of lawyers and lobbyists have put generations of children through college and law school from legal fees charged in the pursuit of something that has never existed in the contemporary music business–a willing buyer and a willing seller. Those people will not want to abandon the very government policy that puts food on their tables, but both sides are very, very good at manufacturing excuses why the compulsory license really must be continued to further humanity.

The even sadder reality is that as much as we would like to simply terminate the compulsory license, there is a certain legitimacy to being clear-eyed about a transition. (An example is the proposals for transitioning from PRO consent decrees–ASCAP’s consent decree has been around a long time, too.) There would likely need to be a certain grandfathering in of services that were pre or post the elimination of the compulsory, but that’s easily done, albeit not without a last hurrah of legal fees and lobbyist invoices. Register Pallante noted in the well-received 2015 Copyright Office study (Copyright and the Music Marketplace at 5) “The Office thus believes that, rather than eliminating section 115 altogether, section 115 should instead become the basis of a more flexible collective licensing system that will presumptively cover all mechanical uses except to the extent individual music publishers choose to opt out.” An opt out is another acceptable stop along the way to liberation, or even perhaps a destination itself. David Lowery had a very well thought-out idea along these lines in the pre-MLC era that should be revisited.

X Day

However, while there is a certain attractiveness to having a plan that the dreaded “stakeholders” and their legions of lobbyists and lawyers agree with, it is crucially important for Congress to fix a date certain by which the compulsory license will expire. Rain or shine, plan or no plan, it goes away on the X Day, say five years from now as Merck suggests. So wakey, wakey.

That transparency drives a wedge into the process because otherwise millions will be spent in fees for profiting from moral hazard and surely the praetorians protecting the cottage industry wouldn’t want that. If you doubt that asking for a plan before establishing X Day would fail as a plan, just look at the Copyright Royalty Board and in particular the Phonorecords III remand. Years and years, multiple court rulings, and the rates still are not in effect. Perseveration is not perseverance, it’s compulsive repetition when you know the same unacceptable result will occur.

But don’t let people tell you that the sky will fall if Congress liberates songwriters from the government mandate. The sky will not fall and songwriters will have a generational opportunity to organize a collective bargaining unit with the right to say no to a deal.

The closest that Congress has come to a meaningful “vote” in the songwriting world is inviting public comments through interventions, rule makings, roundtables and the like–information gathering that is not controlled by the lobbyists. Indeed, it was this very process at the Copyright Royalty Board that resulted in many articulate comments by songwriters and publishers themselves that were clearly quite at odds with what the CRB was being fed by the lobbyists and lawyers. So much so that the Copyright Royalty Judges rejected not only the “Subpart B” settlement reached by the insiders but the very premise of that settlement. Imagine what might happen if the issue of the compulsory license itself was placed upon the table?

Now that songwriters have had a taste of how The MLC, Inc. has been handling their money, maybe this would be a good time to ask them what they think about how things are going. And whether they want to be liberated from the entire sinking ship that is designed to help Big Tech. And you can start by asking how they feel about the $500 million in black box money that is still sitting in the bank account of The MLC, Inc. and has not been paid–with an infuriating lack of transparency. Yet is being “invested” by The MLC, Inc. with less transparency than many banks with smaller net assets.

This “investment” is another result of the compulsory license which has no transparency requirements for such “investments” of other peoples’ money, perhaps “invested” in the very Big Tech companies that fund the The MLC, Inc. That wasn’t a question that was on the minds of Congress in 1909 but it should be today.

Attention Must Be Paid

Let’s face facts. The compulsory license has coexisted in the decimation of songwriting as a profession. That destruction has increased at an increasing rate roughly coincident with the time the Big Tech discovered Section 115 and sent their legions of lawyers to the Copyright Royalty Board to grind down publishers, and very successfully. That success is in large part due to the very mismatch that the compulsory license was designed to prevent back in 1909 except stood on its head waiting for loophole seekers to notice the potential arbitrage opportunity.

The Phonorecords III and IV proceedings at the Copyright Royalty Board tell Congress all they need to know about how the game is played today and how it has changed since 1909, or the 1976 revision of the Copyright Act for that matter. The compulsory license is no longer fit for purpose and songwriters should have a say in whether it is to be continued or abandoned.

We see the Writers Guild striking and SAG-AFTRA taking a strike authorization vote. When was the last time any songwriters voted on their compensation? Maybe never? Voting, hmm. There’s a concept. Now where have I heard that before?

When the dust settled after the last mechanical royalty rate setting we saw the Copyright Royalty Board approving two different settlements for mechanical royalties. The royalty rate for physical mechanicals and permanent downloads get a significant rate increase and the royalty rate for streaming mechanicals got a theoretical rate increase. However, only physical mechanicals and downloads got both a rate increase and a cost of living adjustment (or “inflation protection”). Streaming mechanicals did not get inflation protection–could have but did not.

This means that the same writers on the same song in the same recording will get inflation protection when that song is sold in physical formats (such as the surging vinyl configuration) or downloads, but will not when that song is sold in streaming formats. What is the logic to this? One difference is that record companies are paying on the physical and download side and the lived experience of record companies necessarily puts them closer to songwriters than the services. And the lived experience of streaming companies is…well, breakfast at Buck’s, Hefner level private jets, warmed bidets and beach volleyball courts at home with imported sand. (Although Sergey Brin has a real beach in his Malibu home. Surf’s up in geekville. Maybe he’ll send DiMA to represent him at the Malibu city council meetings if Malibew-du-bumbum is ready for Silicon Valley style lobbying to decide who can surf Sergey’s beach and the color scheme of their boards. Kind of like the Palo Alto Architectural Review Board with a tan.)

The Big Google

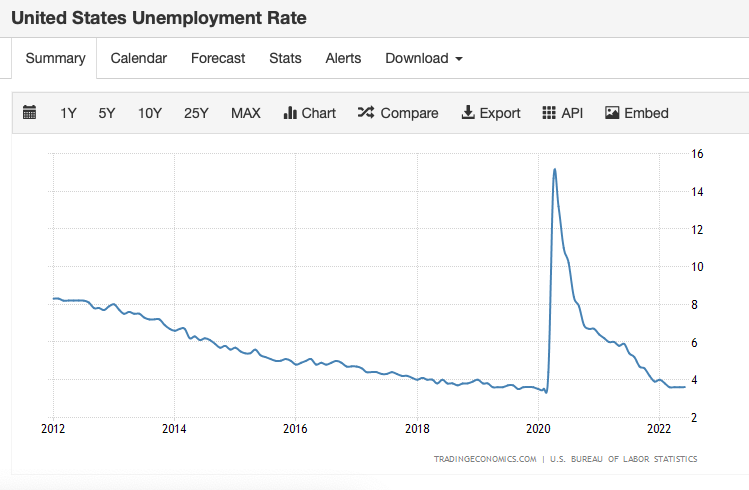

We heard that inflation was transitory, which may prove true–or not. Transitory or not, that’s not an argument against treating songwriters equally on two versions of the same mechanical license; rather, it’s a reason why it should be easy to afford if you cared about sustaining songwriters at least as much as investing in ChatGPT to replace them.

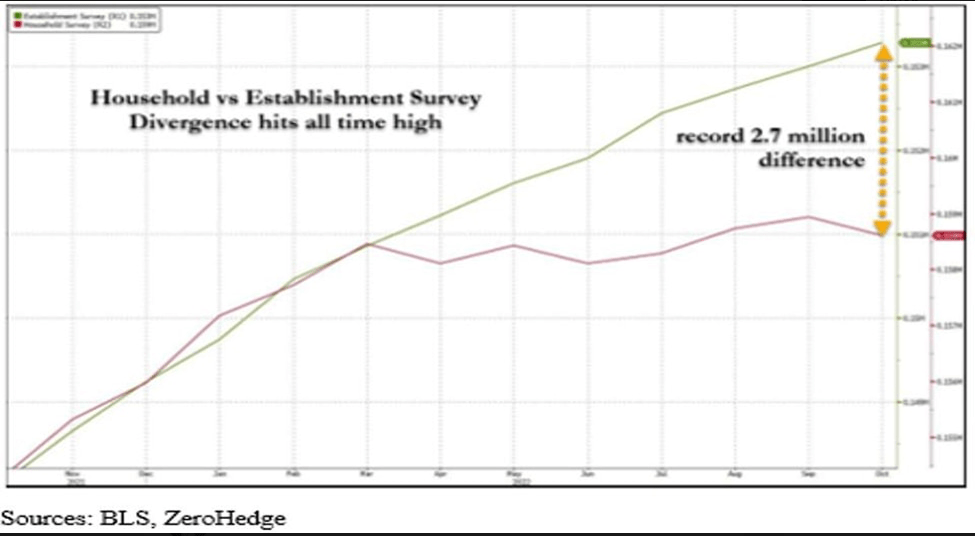

However, in one of the great oopsies of the 21st Century, it doesn’t look much like inflation is all that transitory. Based on some of the posts I wrote starting in 2020, I think we can see that inflation is way worse on the items that count for songwriters like “food at home,” rent, utilities and gasoline. Very often the number of Americans working a job is used to counter the lived experience of the high number of people who believe the economy is tanking. But what about that jobs report? More jobs equals good times, yes? There’s something weird about the math of the jobs report which should make you wonder about whether that’s such a great argument.

If I still have your attention after the “math” word, there are two standard surveys of the economy used to measure jobs that measure different components of the jobs created in a given measurement period. These data are the “Establishment Payroll Survey” which measures the total number of jobs in the U.S. economy. That’s the number most people refer to with the “jobs report” you hear so much about. (More formally titled the “Current Establishment Statistics (Establishment Survey).”)

There’s another number called the “Household Survey” that measures the total number of jobs per household (more formally titled the Current Population Survey).

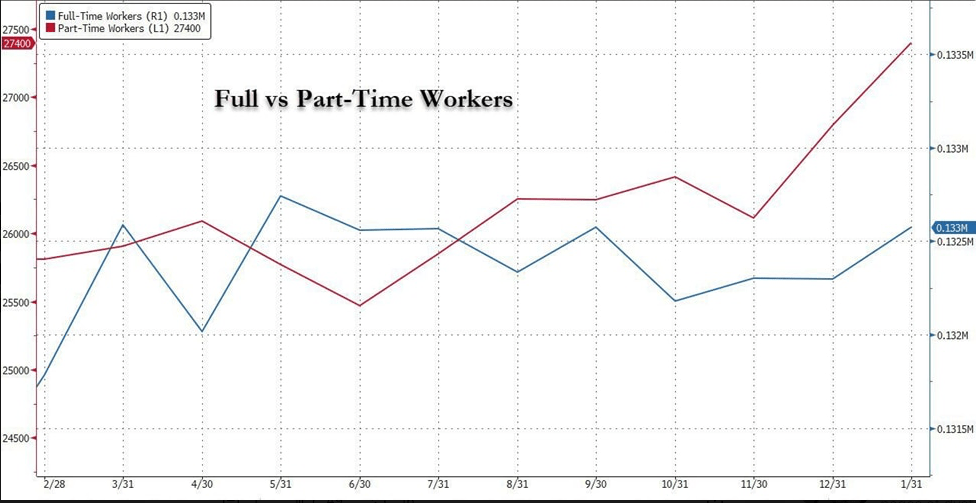

Note that the Establishment survey measures all jobs; the Household survey measures jobs per household. If you had two or three jobs, the Household survey would count you as “employed”; the Establishment survey would count the number of jobs you had. Now note that there is currently 2.7 million job difference between the two. Why?

I’m not really sure, but it would appear that there are more jobs than households. That difference may occur from time to time, but it’s quite a big difference at the moment and seems to be a trend that’s confirmed by another statistic: the surge in part-time jobs as shown in this chart:

So what’s missing is how many jobs that are counted in the Establishment survey are held by any one or two household members in the Household survey. If you were to draw the conclusion that every job in the Establishment survey is a full time job held by the primary source of support in a household and that when the Establishment number is rising things are looking up, that may be a leap unsupported by evidence. That may be one of the things you’d want to know if you were trying to predict how well the government’s songwriter royalties would hold their value over the five year rate period.

The sharp increase since June in the number of part time workers may suggest that more people are working multiple jobs and not that more people are working. In fact, the total number of full time workers seems to have declined by a bit over the same period.

That’s not to say that inflation protection is not a serious requirement of everyone who relies on the government for their livelihood. While the inflation rate has declined a bit recently, possibly due to the Federal Reserve abandoning its zero interest rate policy, it is still significant. In my view, nothing in the employment report suggests otherwise and continues to highlight the importance of songwriters being accorded the same inflation protection on streaming as they are on physical and downloads.

Just because the physical rate is paid by the record companies and the streaming rate is paid by the richest corporations in history does not excuse the distinction. Each should be protected equally.

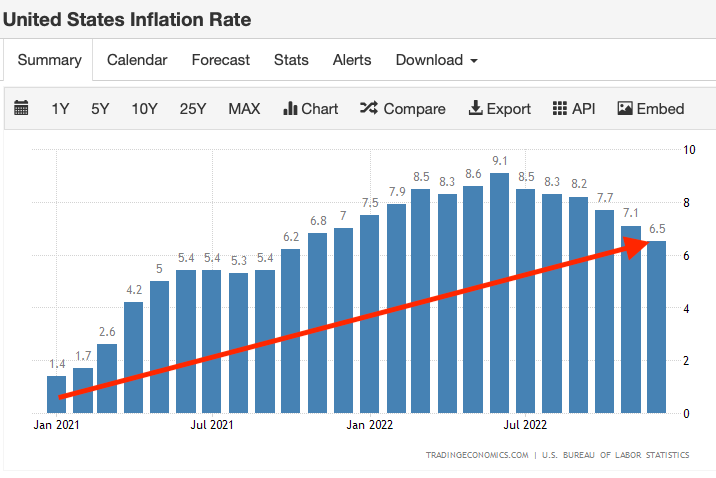

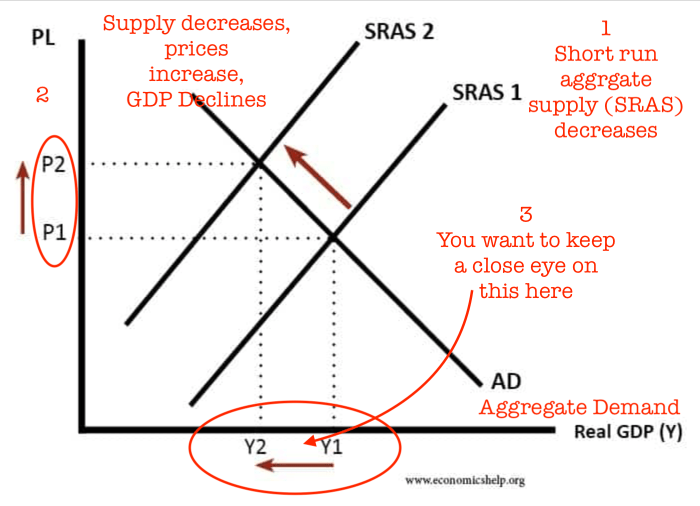

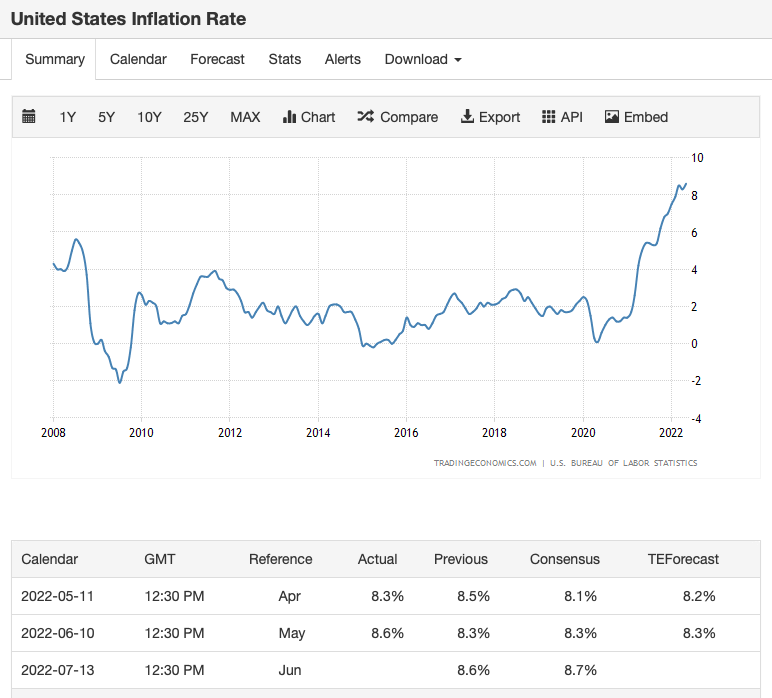

When I made the soft call for impending stagflation last October I had no idea that that it would hit the US economy with such force and speed. The trends were, frankly, obvious and the signs unmistakable. But it’s the speed with which stagflation struck that I didn’t expect. We have seen each step of stagflation’s three point play undeniably demonstrated in real life and the result is inflation as far as the eye can see.

Stagflation’s Three Point Play

The return of 1970s style stagflation and the now-confirmed recession along with Federal Reserve “quantitative tightening” could mean policymakers recognize the need to end the easy money policy that has been in place since “quantitative easing” began around 2008. Arguably, the global economy has been in a post-Big Short bubble ever since, with the inevitable growth in the money supply that provided “too much money” that was chasing “too few goods.”

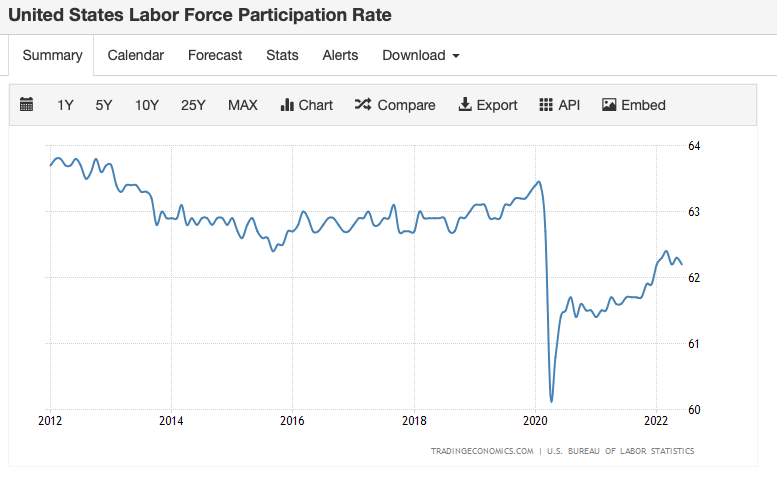

A recession and stagflation call is mitigated by the unemployment rate (which was about triple current rates during the 1970s), which itself is mitigated by the labor participation rate. A ten year view shows that the labor participation rate is still below pre-pandemnic levels even though the unemployment rate has been steady in the recent past. Yet even Y Combinator (that famously wanted to “Kill Hollywood” starting with the unions) warns of investment drying up for startups, but we’re not quite at the point of limited partners refusing to show up for capital calls at major VCs.

Inflation has, of course, been inevitable as has been the commensurate rot of inflation on the buying power of consumers. There is little doubt that inflation has been a long-term trend in the U.S. for quite some time and is likely to be with us for a good long while longer. For songwriters, if you’ve been following the rate increase confirmed in Phonorecords III, imagine what the rates would have been had the rates been indexed in this inflationary environment. We can understand how they missed indexing on Phonorecords III, but they cannot miss it on Phonorecords IV–or give it away as a bargaining chip.

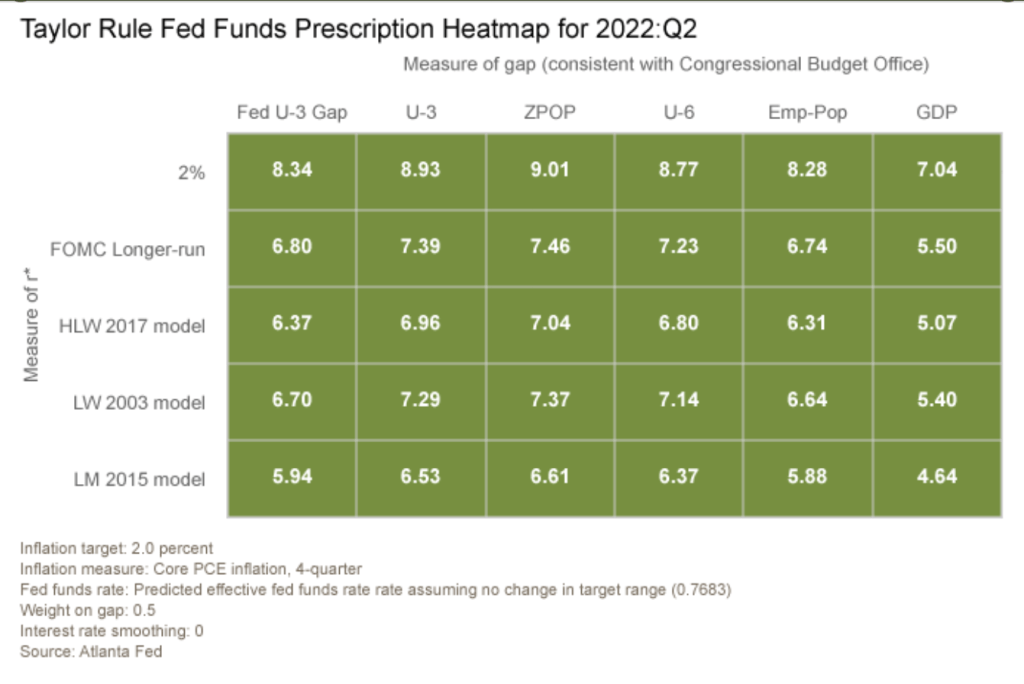

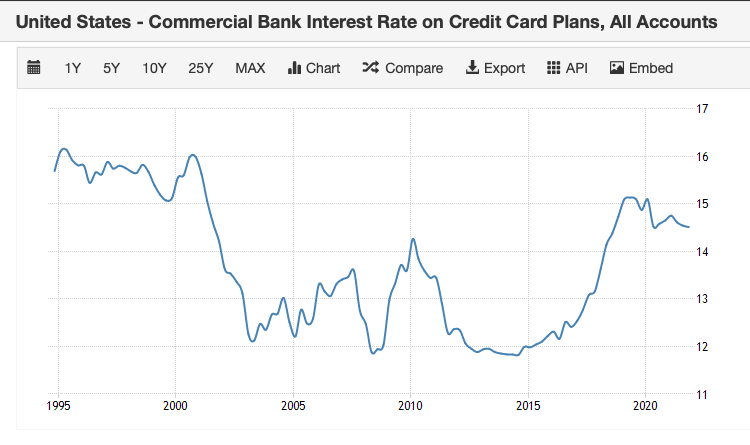

Realize that one accepted method of extinguishing inflation is the “Taylor Rule” implemented by Federal Reserve Chairman Paul Volker in the 1970s for which Presidents Carter and Reagan took tremendous political heat–raise interest rates OVER the inflation rate. (Which is why there was a 21% prime rate–think on that.).

Source: Atlanta Federal Reserve

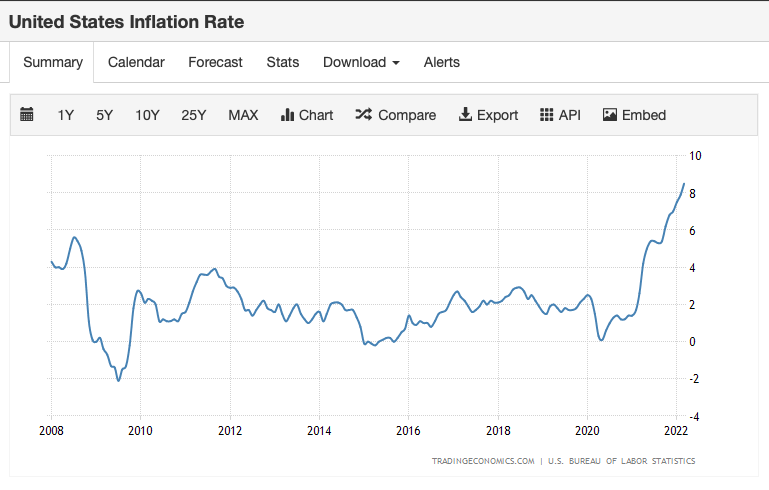

It was a different country then–America was a creditor nation. No longer true. Of course that’s not likely to happen today because of all the government borrowing during the easy money era. If the government had to pay a rate over the current 8.7% inflation rate, the government would collapse. It is likely that high inflation will be with us for a long time to come.

Being aware of the inflationary economic environment is a critical issue for songwriters in the US who are in the middle of a government rate setting proceeding before the Copyright Royalty Judges at the Copyright Royalty Board in Washington, DC. Songwriters at least have the opportunity to include a cost of living adjustment in the government’s rate and have asked for it in the streaming proceeding. Remember, there are two rate proceedings underway: One for physical mechanicals and downloads and the other for streaming. Songwriters, publishers and labels are in the physical and downloads proceeding. Songwriters, publishers and Big Tech are in the streaming proceeding soon to go to trial.

Credit where credit is due, Universal, Sony and Warner labels have included an annual CPI adjustment (or “indexing”) for songwriters in their voluntary agreement to raise the previously frozen mechanical rate for physical and downloads. The Copyright Royalty Judges also included indexing in the rate for webcasting of sound recordings that they recently decided (Web V). Many of the same Big Tech services were parties to Web V but are now arguing against CPI for songwriters in Phonorecords IV. Different hearings, true, but a lot of overlap in the parties and their smug little straight faces.

In our stagflationary economy, an agreed-upon inflation adjustment is a fairness making term that doesn’t make songwriters eat all of the inflationary rot from cost increases for “food at home” and force them to predict those price changes five years in advance. Indexing helps to fix that guess work in what is already a process of educated guessing in the non-existent willing buyer/willing seller folie à deux.

An inflation index is a particularly crucial tool when songwriters are prevented from stepping away from a deal because the government forced a deal upon them, like any statutory rate or in countries where there is a tariff or other compelled agreement.

Failing to use indexing makes the fairly controversial assumption that economically rational songwriters would charge a fixed price regardless of the fluctuations of the cost of energy, food and rent. By using the government to impose a non-indexed rate, there is a government-mandated implied discount that accrues to the benefit of the services, aka the largest companies in commercial history who just can’t bring themselves to treat songwriters fairly.

But want to bet these failures will have no impact on the services’ ESG scores on Wall Street?

Take Google for example, flatly rejecting indexing on the streaming side of the CRB proceedings:

“None of Google’s agreements with music publishers contain CPI adjustments for the [Per Subscriber Minimums] contained in those agreements. The Copyright Owners’ proposed CPI adjustment to PSMs is simply unsupported by marketplace evidence.” https://app.crb.gov/document/download/26528

Google is, as usual, full of it and is gaslighting the CRB with inapt arguments. Google is in a rate proceeding where the government—not Google—sets the terms. I know that line gets a little blurry for Googlers given how much strangulation Google sustains over government through its vast network of lobbyists, revolving door men and women, consultants and on and on and on.

I also know that Google would love nothing more than to dictate the terms to the government because Google has not-unjustified delusions of grandeur in this regard due to their mind-blowing level of brazen influence peddling. It’s not just Google, it’s all of the Big Tech oligarchs, the latter day Xerxes who seek to overwhelm creators through lawfare—songwriters are just low hanging fruit because of the ancient compulsory license—Section 115 of the Copyright Act—that is ready made for Big Tech’s copyright abuse.

But Google is not the government. It is the Congress and not Google that created Section 115 to interfere with private contracts and more importantly interfere with the right to privately contract. That’s a big deal in the US.

So, the issue isn’t what Google may have done in contracts with a totality of vastly different terms in a completely unrelated setting. It’s whether the government is paying just compensation for taking away rights under the Constitution of the United States. More specifically the 5th Amendment “takings” clause.

And the government’s compensation to songwriters is not just. It never has been.

Remember that at the heart of this process, the Judges are required to set a price for songs that the Judges believe reflects what a willing buyer would pay a willing seller in a transaction that has been devoid of willing buyers and sellers for over 100 years.

Google and other Big Tech DSPs in the CRB present the Judges with benchmarks based on prices that are not only distorted by years of abuse to begin with but are permanently disfigured. Remember, the government set the mechanical rate at 2¢ from 1909 to 1978 and had raised it very slowly ever since while at the same time pretending that the distortion of the 2¢ rate did not exist.

This deep 2¢ hole that songwriters are digging out of may not be the only reason songwriters are so poorly compensated, but this “tuppence” era definitely is a contributing factor. So whatever value-based rate increase that songwriters can claw out of the Big Tech services must be supported by a cost of living adjustment measured by the CPI just to tread water.

Price is truth if prices are truthful. And undistorted.

Otherwise, it’s just frozen mechanicals by another name, and Big Tech is simply free riding on the government’s license due to their outsized lobbying influence and government capture. (Need we name names?)

The songwriter is simply subsidizing the biggest corporations in commercial history.

It looks like the statutory rate for songs on compact discs and vinyl is finally going to get a significant increase starting January 1, 2023 (assuming the Copyright Royalty Board approves the settlement proposed by the major labels and the publishers). We have to acknowledge that there are many independent record companies that have never had to deal with an increase in the mechanical rate–the old 9.1¢ rate has been in effect since 2006. If a label was founded any time after 2006 the issue just hasn’t come up before.

The new rate (which may well change every year of the 2003-2007 rate period due the cost-of-living indexing) will require labels to check their royalty accounting programs to make sure they change the rates as required. It will also become an audit point for artist audits by artist/songwriters or producer audits by producer/songwriters, and of course publisher audits as well.

But there’s also a question of how to address what I call the “controlled comp squeeze” caused by the collision of rate fixing dates with the new rate as applied to outside writers. (I’ve posted a bunch on these topics, so if you don’t immediately recognize what I’m getting at, I refer you to those posts.)

In addition to the controlled comp squeeze, the conversation should include what to do about the entire controlled compositions concept, a contract clause that only applies to the US and Canada and a concept that is anathema to ex-US and Canada songwriters and collecting societies. Because digital recordings are typically paid at the full statutory rate (or should be), controlled compositions clauses are really a feature of physical configurations.

There’s a feeling out there that the entire concept of controlled compositions should be abandoned. Since record companies have come to rely on certain economics when they decide to keep titles in print and not to cut them out, i.e., stop making them available to retailers, it is important to understand what effect that trying to force labels to pay every song at full rate will have on the music economy, especially for independent labels that sell a disproportionate number of vinyl units. Sudden increases in royalty costs could have dire consequences for the people who frequently are the main investors in certain genres of music and have the least ability to lobby for their interests, so we should tread prudent in rebalancing the songwriter economy.

One intermediate step might be to take a cue from a business practice in Canada called the “Mechanical License Agreement” that has worked very well for many years. The “MLA” offers protections from the worst terms of the controlled compositions clause and was a voluntary agreement between the labels and the CMRRA (Canada”s mechanical collecting society).

2011 Interview with David Basskin

The MLA originated with David Basskin, the former head of CMRRA, and David negotiated the MLA with the major and independent labels in Canada. You can listen to my 2011 interview with David on SoundCloud.

The principal terms of the MLA cover the rate (which was no less than 3/4 rate but that dog won’t hunt anymore, plus after 1988 Canada did not have a statutory rate like the US does), free goods limited to 15%, no reduction for outside writers paid at full rate.

1. Full Rate: Songs should be paid at the full applicable rate and should be paid on standard sales plan LP free goods (a common give if the artist/writer is signed to a publisher affiliated with the record company);

2. Cap: Rather than a contract rate of 10 or 11, the MLA pegs the cap at 12;

3. No Rate Fixing Date: The rate not only is full, it also floats so there is no concept of a rate fixing date and should apply retroactively and prospectively; and

4. Floor: The application of the cap cannot result in any song being paid less than 50% of the full rate (which could happen on multiple disc or box sets).

There are other bells and whistles, but these are the main points.

While I understand that a record company would want to cap their mechanical royalty expense, any one of these terms would further that commercial goal. It is the application of all of the controlled comp terms that make the clause so onerous.

While the Copyright Royalty Board can set the rates, I doubt that they have the jurisdiction to address private contracts. Congress could pass legislation, but I think that would be a bitter struggle and I’m not so sure I want Congress to be micromanaging the music business any more than they already do with statutory rates and rate courts.

But there’s nothing stopping a voluntary agreement.

As readers will recall, I’ve been beating the drum about inflation and stagflation coming home to roost for many months, nearly a year now. These posts are in the context of the compelling need for a cost of living adjustment for songwriters’ statutory rates and the absurdity of a frozen mechanical for the booming vinyl and CD configurations which thankfully has now been rejected by the Copyright Royalty Board once and for all.

When you force songwriters to license and also force them into accepting a government rate for mechanical licensing set by a little intellectual elite in a far-distant capitol, the last thing that’s fair or reasonable is to unilaterally freeze those rates when songwriters are staring down the worst inflation in 40 years. This is particularly galling when rampant inflation was all entirely predictable and the smart people and the economists they supposedly consult with just missed the boat.

Why do I say that the current inflation was entirely predictable? I’ve promised a few times to discuss quantitative easing so here it is. As you read this post, remember that both the current story on inflation and the need to index the statutory mechanical rate started in 2008 with the Great Recession and has been coming for at least fourteen years–plenty of time to recognize that the answer to inflationary destruction of a rate songwriters are forced to accept was not to freeze the rate to make the inflationary destruction even worse. Rather, the answer was to index the rates to inflation at a minimum. Indexing would at least preserve purchasing power if the government was not willing to provide an actual increase based on value. The central bank policy known as “quantitative easing” and its corresponding zero interest rate policy guaranteed the rot of inflation was inevitable.

Printing Too Much Money

Start with the definition of inflation we all have probably heard: Too much money chasing too few goods. When you hear this, some people think of the transaction on the consumer level, as in too much consumer money chasing goods in a productivity decline, aggregate inventory mismatch or raw supply shortage.

But that’s not the fundamental question–how do you get “too much money” in the aggregate across the entire economy at the same time? The way you always do; the government increases the money supply by putting too much money into circulation. The old fashioned way of doing this was literally printing paper money, but the terribly modern digital way of doing it is called “quantitative easing” which has the same inflationary effect because it is effectively the same thing as printing paper money. (The powers that be also refer to it as “QE” like it’s a cute little puppy or a Star Wars android. It’s not so we won’t.)

The difference between old school and new school is that instead of printing money that ends up in bank accounts of those guarantors of the full faith and credit of the United States–that guarantor is the person you see in the mirror–the Federal Reserve created digital money and they gave it a Fedspeak name that conveyed no information about what was really going on. They called it “quantitative easing” which is right up there with “Department of Defense” and “late fee program” in Orwellness. It’s quantitative because it digitally creates money on the books of the Federal Reserve and it’s easing because easy money. The Fed also cut interest rates to near zero (the “lower bound”) and some would argue they essentially created negative interest rates, all in the name of financial stimulus that Congress–i.e., elected officials we vote for–didn’t vote for.

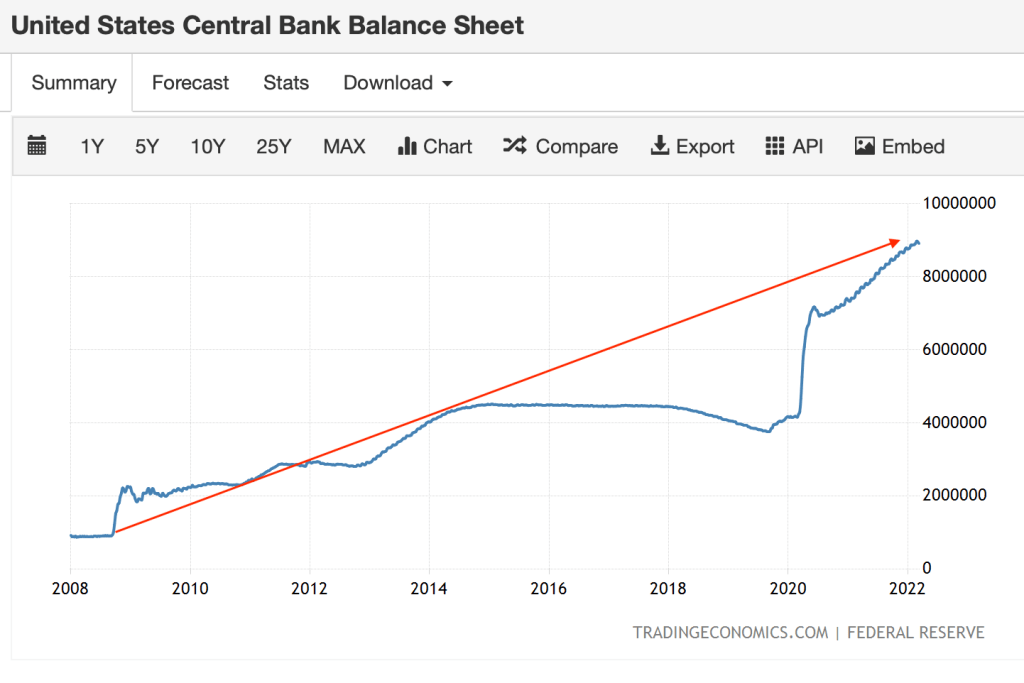

This quantitative easing started out in 2008 to be an emergency method of propping up the economy after the last time that Wall Street screwed things up on a grand scale in the 2008 financial crisis.

What was supposed to be a short term fix is still going on to this day 14 years later. So the unelected smart people who deal with the Copyright Royalty Board (also not elected) must have known this was coming and that the last thing you would want to do was freeze rates when the watchword in the general economy was “stimulus”.

The combination of the Fed’s quantitative easing and the Fed’s zero interest rate policy caused one of the greatest asset bubbles in the history of mankind. And when you hear that the Fed is now increasing interest rates and simultaneously “reducing its balance sheet” by selling about $1 trillion of government and corporate bonds, this is what they are talking about. Many think that the only way of getting out of this bubble is to either raise taxes–fat chance–or raise interest rates and reduce the money supply. The truth is, the U.S. has never been in this exact situation before so no one really knows what will work, but we do know what has worked before. And wage and price controls such as freezing the statutory rate does not work (as President Nixon discovered in 1971). Of course if you wanted to fix the problem by properly aligning incentives, songwriters could have told their publishers that for every 1% increase in inflation, they could reduce the salaries of the smart people by 1% until the freeze comes off. That’s called incenting the wrong people to do the right thing. Like that will happen.

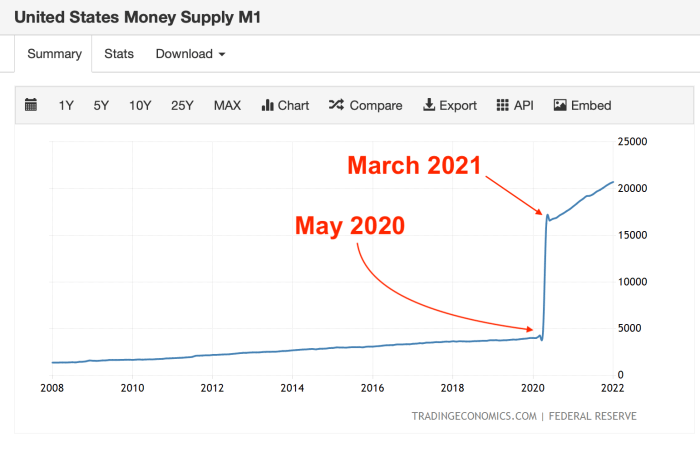

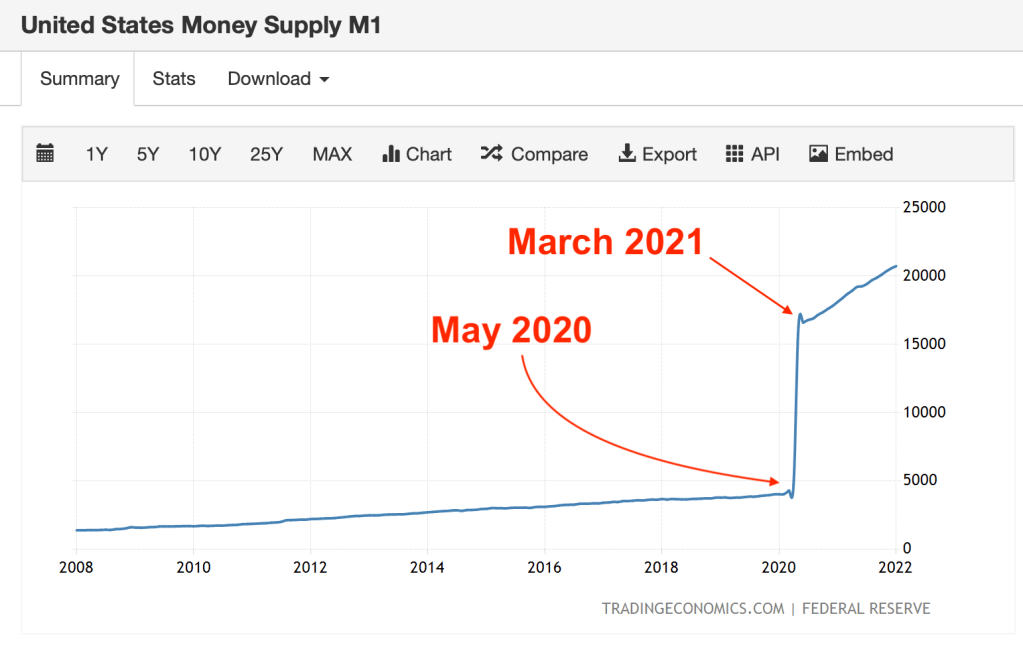

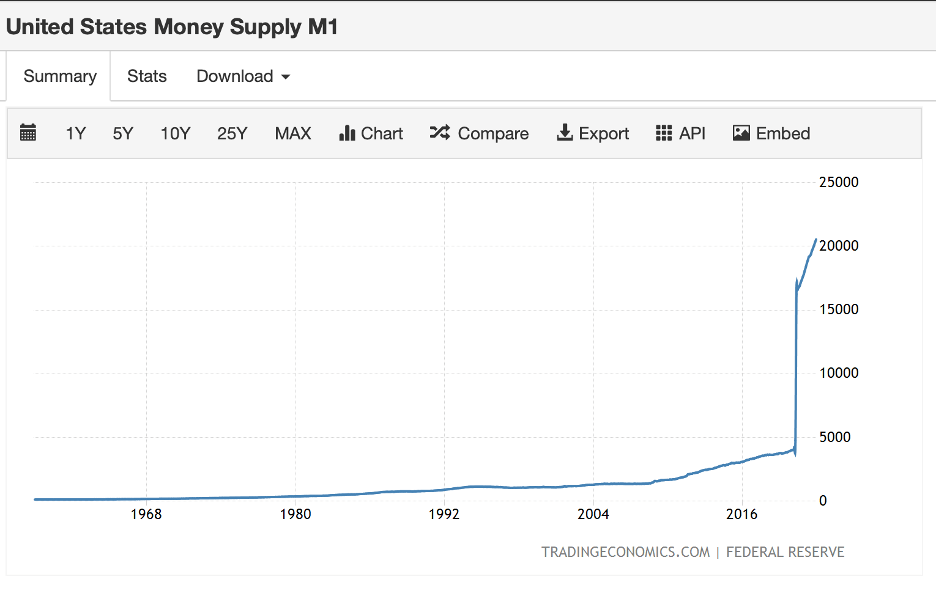

So time for charts. Back to the “too much money”, let’s look at the basic money supply often called “M1” and remember–inflation is not a cause of the growth in the money supply, it is a symptom of the government printing too much money. Because you have to have money to chase goods, right? And the money only comes from one place.

As you’ll see in this snapshot of the growth of M1 since 2008, there’s fairly steady growth until it hockey sticks in 2020 and continues after the $1.9 trillion American Rescue Plan passed in March of 2021. More on economist Steve Rattner’s take on that coincidence later.

Remember, the U.S. central bank (called the “Federal Reserve” or “the Fed”) has two tasks in its mission: Keep inflation and unemployment low. The Fed historically has two “weapons” to control the economy to accomplish its mission: interest rates (especially a targeted “federal funds rate”) and the money supply.

The money supply is going to be our focus in this post, but it wasn’t much of an issue at the Fed until the financial crisis of 2008 when the Fed introduced “quantitative easing.” The growth of the money supply has become a significant issue since COVID and especially since 2021.

How the Fed Injects Too Much Money in the Economy

The way the Fed typically increased the money supply before quantitative easing was by buying Treasury notes or other liquid assets in the open market or by actually printing more currency which was distributed in the real economy through retail banks. (Remember we separated banks between retail and commercial during the New Deal in the Glass Steagall legislation. Read up on that separately, beyond our scope here.) Most of the Fed activity before 2008 has been focused on tinkering with the interest rates that the Fed controls, often the “Federal funds rate”.

Increasing the money supply before quantitative easing typically lowered interest rates, put more money in the hands of the consumer and stimulated business activity—including loaning money to other retail banks–through an increase in aggregate demand. Lowering interest rates expands the economy by making money cheaper; raising interest rates contracts the economy by making money more expensive. The Fed can decrease the money supply by selling Treasuries in the open market which is another way to control inflation, or try to anyway. This is also called reducing the Fed’s “balance sheet” (securities held by the Fed) and tends to raise interest rates. If you follow the financial press, you’ll hear a lot about that currently.

When demand is high, i.e., economic activity heats up, the Fed typically raises interest rates to avoid high demand becoming hyper inflationary. (People often use post WWI Germany as an example of hyperinflation when workers were paid a few times a day to avoid their money losing value by the time they got off work–yeah. Think on that when you buy gasoline or groceries this week.) The Fed also may largely leave the money supply alone. When demand is low or collapses, as has happened in various financial crises such as the Great Recession, the Fed may lower interest rates to encourage demand with debt-driven economic activity by consumers and firms—and, of course the government. We’ll come back to the government part.

The Fed historically has let the money supply grow at a relatively steady rate. The growth of the M1 (M0 plus demand deposits less reserves) looks something like this which makes that 2020-2022 hockey stick look even more pronounced:

What do we remember most about the financial crisis? I don’t know about you, but the event I remember most was the first time I heard one of the newsreaders utter the word “trillion” as a modifier for “dollars.” I remember that like I remember where I was on 9/11. And I also remember what I thought at that moment—these numbskulls are going to bankrupt the lot of us because it’s the government. When it comes to a trillion dollars, it’s betcha can’t spend just one. (Fast forward a few years to the Speaker of the House saying with a straight face, “if they come up a trillion, we’ll come down a trillion.” And they give you that look like they just said something smart. Insane.)

But I digress. Quantitative easing was a workaround to get more cash into the financial markets. Not in your bank account, but into Wall Street. How so?

Some Mechanics on Quantitative Easing

Remember, the Federal Reserve is responsible for controlling the money supply. The civics class version of this story is that the Treasury Department prints the money. When the Federal Reserve actually prints currency, it submits an order to the Treasury Department’s Bureau of Engraving and Printing then distributes that newly printed currency to the thousands of banks, savings and loans and credit unions in the banking system. But you see the problem there? Someone at the Federal Reserve Board of Governors has to submit an order (which must be voted on) to the BEP, and then all those bankers know what’s going on.

Does that sound easy? Does that sound like a politically costless transaction? Why no, it does not. And that may be why that process is called printing money. So it’s not quantitative easing.