Nice post by Ed Christman in Billboard explaining the continuing crisis on frozen mechanicals. Ed comes up with a rough justice quantification of the impact on songwriter and music publisher revenues in light of controlled compositions clauses in recording contracts that apply to (a) songs written and recorded by artists, or (b) songs by “outside writers” if and only if the artist can get the outside writer to accept the controlled compositions terms and rates.

For those reading along at home, one theory (aside from sheer leverage) that gets used in this context is that the artist/writer can agree on behalf of all co-writers to accept the terms of the license granted by the artist to the label in the controlled compositions clause because they are co-owners of an undivided interest in the song copyright and can grant nonexclusive licenses in the whole subject to a duty to account provided the license is not economic waste or self-dealing. Let’s just leave all that where it lays for now, but that story has never really been properly challenged–particularly the economic waste part given the rate fixing date issue and even the frozen mechanicals crisis itself. We’ll come back to that bit some other time.

The rate fixing date is a key part of the discussion for understanding the impact of unfreezing mechanicals. So what is that rate fixing provision?

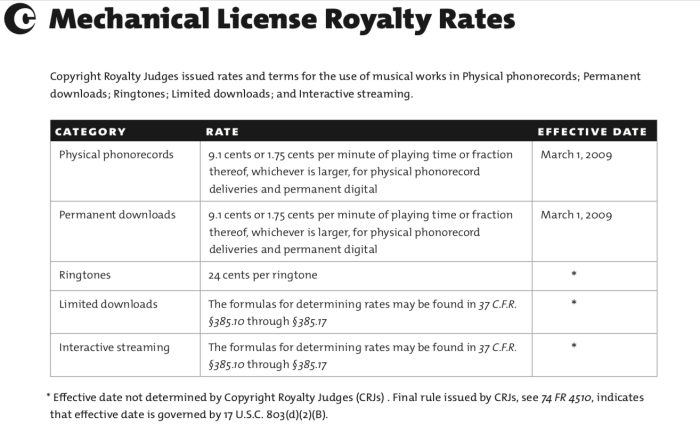

Remember, the controlled compositions clause starts with reducing the minimum statutory mechanical rate in the US (and in theory in Canada subject to MLA) in effect at a point in time. That point in time is either commencement of recording (booo!), delivery, release or sale of a unit embodying the song at issue. Remember that the labels only pay mechanical royalties on physical and downloads (the rates at issue in the frozen mechanicals crisis)–streaming services pay for the interactive streaming mechanicals (and there is no mechanical for webcasting, a whole other beef).

You say, wait–isn’t the mechanical rate 9.1¢? Why does it matter when the record was recorded, delivered, released or sold? Won’t the rates all be the same? And you’d be right if you were asking about a record recorded and released in 2006 or after, or a record recorded and released between 1909 and 1978, like, say some titles by Bob Dylan, The Beatles, Otis Redding or Miles Davis.

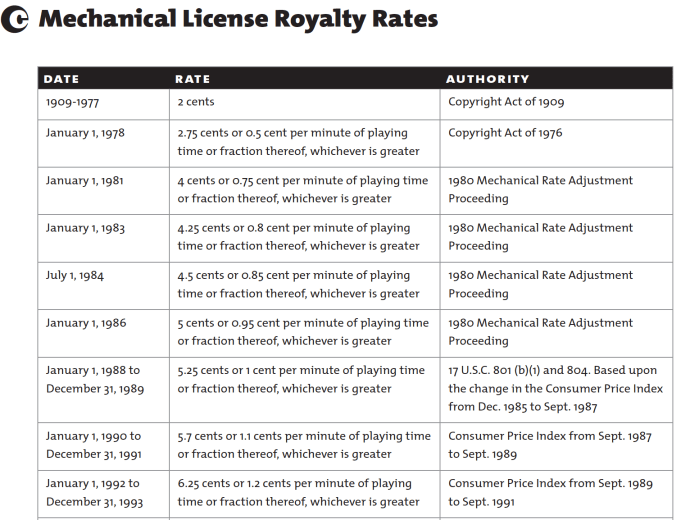

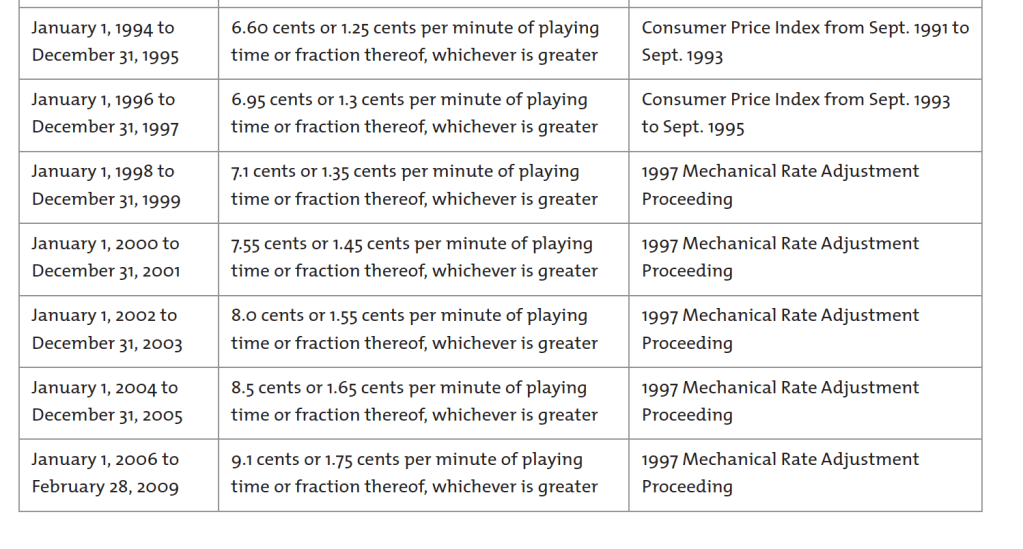

But–it wasn’t always this way. The mechanical royalty rate was set at 2¢ by Congress with the first statutory license, i.e., compulsory license, in 1909 and did not change until the 1976 revision of the US Copyright Act effective 1978. The rate then began to incrementally increase over the years until it reached 9.1¢ in 2006, a phased increase that was to compensate for Congress failing to increase the rate for 70 years, aka “the Ice Age”. The Congress really screwed up songwriters’ lives by freezing the rate at 2¢ during the Ice Age and songwriters and their heirs have been paying for it ever since, right up to the 2006-2022 period, aka “the Second Ice Age” or the Return of the Neanderthals.

In an effort to help songwriters shovel out from the Ice Age, The Congress also authorized indexing the minimum rate to inflation from 1988 to 1995. Indexing is again on the mind of the Copyright Royalty Board right now–bearing in mind that an increase in rates due to inflation has nothing to do with the intrinsic value of the song copyrights so there’s no confusion. Indexing simply applies any increase in the consumer price index to the statutory rate and preserves buying power. In a way, it is the opposite of a case about value. Indexing assumes that the value issue was already decided (in this case in 2006) and simply preserves buying power so that the “nominal” rate of 9.1¢ in 2006 can still buy the same amount of goods or services in 2022 (or 2023 in the case of the CRB rate period). Otherwise the “real” rate, i.e., the inflation adjusted rate, is not 9.1¢ it is about 6¢.

Remember–the proposed rate increase to 12¢ by the CRB is not about value, it’s about buying power because it’s solely focused on inflation.

So back to controlled compositions. It is no coincidence that at the same time as the 1978 increases were phased in, the labels established controlled compositions clauses that knocked songwriters back down. They would probably not have gotten away with freezing by contract at 2¢ so they let the rate float up but much more slowly and with several caps. The first cap is the maximum number of songs, usually 10 or 11. The next cap is the infamous 3/4 rate, where the label pays based on 75% of the minimum statutory rate. But the third cap is the rate fixing date and that’s the one we want to focus on in the unfrozen mechanicals context.

In simple form, it looks something like this contract language:

If the copyright law of the United States provides for a minimum compulsory rate: The rate equal to seventy-five percent (75%) of the minimum compulsory license rate applicable to the use of musical compositions on audio Records under the United States copyright law (hereinafter referred to as the “U.S. Minimum Statutory Rate”) at the time of the commencement of the recording of the Master concerned but in no event later than the last date for timely Delivery of such Master (the applicable date is hereinafter referred to as the “Copyright Fixing Date”). (The U.S. Minimum Statutory Rate is $.091 per Composition as of January 1, 2006);

The way that the statutory rate increases come into the controlled compositions clause is because from 1978-2006 the statutory rates increased across albums delivered across album cycles. If you consider that the rates used to increase about every two years and that an album cycle can be two years, it’s likely that LP 1 would have a lower rate than LP2, LP 2 than LP3 and so on right up to 2006.

Also remember that the increases in rates are prospective, meaning that the controlled compositions rate on recordings delivered in the future will, of course, get the higher rate, even if the past rates don’t change which they don’t, at least not yet. Also consider that permanent downloads often are excluded from controlled comp treatment and are paid at full rate, probably on the rate fixing date in the artist’s agreement. Sometimes the download rates “float” or increase in line with increases in the statutory rate, but that’s part of individual negotiations.

If there is an outside songwriter who does not agree to accept the artist’s controlled composition rate (and there are plenty of these) what happens? Typically the label will account to the outside writer at their full minimum statutory rate but will deduct that payment from the maximum aggregate mechanical royalty payable to the artist (i.e., the 10 song cap). There’s some twists and turns to this involving rates on different units “made and distributed”, but for our purposes there is one clear thing to understand:

Because of the rate fixing date which is frozen by contract (the Mini Ice Age) the artist/songwriter will be paying a higher mechanical to the outside writer from a frozen royalty “pool”.

This is why you should always, always demand “protection” for at least one outside song in your contract and then review each album to determine if that needs to be increased. This is particularly true for records made in places like Nashville where the record company will demand you work with “A” list songwriters (assume none of whom will take 3/4 rate) and then try to deduct the difference between the uncontrolled rate and the controlled rate from you (and if it gets big enough, cross it to your record royalties). (Not only will A list writers not take the 3/4 rate, they’re pissed because they can’t charge you double stat like they do double scale for sessions.)

Example: You have a 10 x 3/4 rate cap on mechanicals, the “cap rate”. That’s the 68.25¢ album rate you hear about (10 x .75 x 9.1¢). Say you have 10 songs on your album and you wrote all of them. You get the entire 68.25¢. If you had two outside songs whose writers get 9.1¢ under current rates, you deduct 18.2¢ from the cap rate, and that leaves 50.05¢ as the “controlled pool” or the total mechanical royalty payable to the artist/songwriter (actually all controlled writers, but leave aside that wrinkle).

So you can see, that’s no longer a 75% rate, it’s actually more like a 55% rate.

Now let’s assume that the new rate is 12¢. Same calculation, two outside songs now get 24¢, but the cap rate stays the same because of the rate fixing date. During the Mini Ice Age, i.e., while that cap rate is fixed at 9.1¢ x 10 x .75, the controlled pool now is expressed as 68.25¢ – 24¢ = 44.25¢, or about 48% (44.25 ÷ 91). The artist’s publisher is not going to be wild about that; the outside writer’s publishers will be thrilled.

This will start to true up on the next LP that takes a rate fixing date after the 12¢ rates go into effect. In that situation you’d be increasing both sides of the equation, so the cap rate would increase to 90¢ (10 x .12 x .75). The outside writers still get 12¢ each for two songs (or 24¢) which is deducted from the cap rate to get a controlled pool of 66¢. The true controlled comp rate is then back to about 55%.

These effects will be less pronounced if you have protection for one or more songs (or fractions of songs) or you have a higher cap, say 11 or 12 instead of 10 (with corresponding increases on other configurations). But you see the trend line.

I think this leads to the conclusion that increasing the statutory rate is a huge step forward and we should all be grateful to the Judges. The rate fixing dates for catalog titles (really the entire rate fixing date concept) must also be considered and any new effort to tweak the controlled compositions clause to effectively nullify the Judges’ rate increase will no doubt cause further conflict.

One day Congress will again act to reduce the effects of the controlled compositions clause and especially the rate fixing date, but in the meantime the Judges may well visit the issue to the extent they are able before we see the Return of the Neanderthals.