By Chris Castle

As an important publisher panel observed at MIDEM this year, revenue share deals make it virtually impossible for publishers to tell songwriters what their royalty rate is. That’s especially true of streaming royalties payable under direct licenses for either sound recordings or songs or the compulsory licenses available for songs.

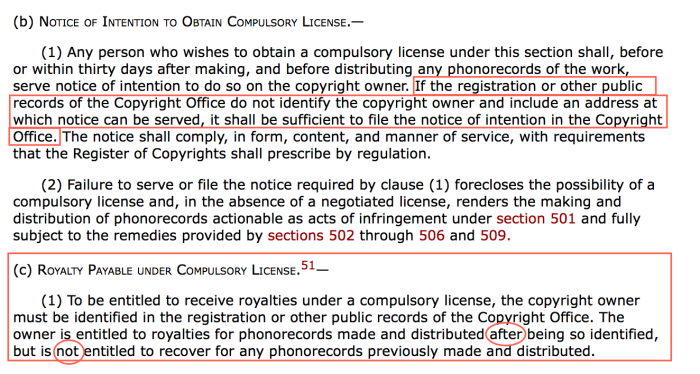

There are some good reasons why streaming rates developed without a penny rate–or at least some reasons that are the product of sequential thought–but there are also good reasons for creators to be distrustful of the revenue share calculation. This is particularly true of compulsory licenses for songs where songwriters and publishers don’t even have the right to examine the services books to check if the service complied with the terms of the compulsory license (known as an “audit” or “royalty compliance examination”).

If you thought record deals were complicated, you will probably have to find a new vocabulary to describe streaming royalties. (Calling Dr. Freud.) But even under direct licenses for songs or sound recording licenses where there usually is an audit right, the information that needs to be audited is so closely held, so over-consolidated and the calculations so complex that there may as well be no audit right.

The result is that smart people with resources at big publishing houses cannot determine the penny rate coming out of Spotify and others with the information that is on their accounting statements. That is hard to explain to songwriters (or artists for that matter, as they have similar problems).

Why is the calculation so complex? The artist revenue share calculation looks something like this in its generic configuration:

[Monthly Service Advertising Revenue or Monthly Subscription Revenue] x [Your Total Monthly Streams on the Service/All Monthly Streams on the Service] x [Revenue Share] = Royalty per stream

Both monthly revenue and monthly usage change each month–because they are monthly. In order to get a nominal royalty rate, you have many calculations on both sides of the equation. Because these calculations are made monthly, it is not possible to state in pennies the royalty rate for any one song or recording at any one time. There’s actually an additional eye-crossing wrinkle on subscription deals of setting a negotiated minimum per subscriber which can vary by country, but we will leave that complexity aside for this post–YouTube’s “Exhibit D” lists 3 pages of one line entries for per subscriber minima around the world.

In a simple example, if both advertising revenue and subscription revenue were $100, your one recording was played 10 times in a month, all recordings were played 100 times in a month and the revenue share was 50% for the sound recording then you would get:

$100 x [10/100] x .50 = $0.50 for that month. How you get to the multiplicand in the revenue pot is not so simple and has gotten more complex over the years. In fact, the contract language for these calculations make the Single Bullet Theory seem more plausible.

Revenue share formulas produce a different product when the factors change–which for the most part changes every month. The formula we’re using is for the sound recording side, but publishers have a version of this calculation for their songwriter’s royalties, too. The statutory rates are a version of this formula (see the nearly unintelligible 37 CFR §385.12).

Most of this information is under the exclusive control of the service, and largely stays that way, even if you are one of the lucky few who has an audit right. Bear in mind that the “Monthly Service Advertising Revenue” in our formula is a function of advertising rates charged by the service, and “Monthly Subscription Revenue” is a function of net subscription rates charged by the service. These calculations take into account day passes, free trial periods, and other exceptions to the royalty obligation. There is essentially no way to confirm the revenue pot when the royalty rates appear on the publisher or label statements.

The problem is that the entire concept of revenue share deals is out of step with how artists and songwriters are used to getting paid, even for other statutory mechanical rates such as that for downloads. If a publisher or label can’t come up with a nice crisp answer for what the songwriter or artist royalty is based on, the assumption often is that the creator is being lied to. And who’s to say that’s an unreasonable conclusion to jump to? The question is–who is lying? Here’s a tip–it’s probably not the publisher or label because they’re essentially in the same boat as the artist.

How Did We Ever Get Here?

Let me take you back to 1999. Fish were jumpin’, the cotton was high, and limited partners showed up for capital calls. Startups were starting up their engines–some to drive into a brick wall at scale, others to an IPO (and then into a brick wall at even greater scale).

On the Internet, you didn’t just do business with a company, they were your “partner.” You didn’t just negotiate a commercial relationship with a behemoth Fortune 50 company that could crush you like a bug–in the utopian value system your little company “partnered” with AOL for example. Or Intel. Or later, Google.

What that meant for music licensing was that startups wanted rights owners to take the ride with them so if they made money, the rights owner made money. Rights owners shared their revenue, you know, like a partner. Except you only shared some of their revenue. You weren’t really a partner and had no control over how they ran their business even if the only business they’d had previously run was a lemonade stand.

The revenue share deal was born. To some people, it seemed like a good idea at the time. And it might have been if there were relatively few participants in that revenue share. But revenue share deals don’t scale very well.

Enter Professor Coase and His Pesky Theorem

Here’s the basic flaw with revenue share deals: Calculating the share of revenue for the entire catalog of licensed music on a global basis requires a large number of calculations. For companies like Spotify, Apple or YouTube, calculating the share of revenue for millions of songs and recordings requires billions of calculations.

Free services like Spotify or YouTube involve billions of essentially unauditable calculations, all of which are based on a share of advertising revenue. Advertising revenue which is itself essentially unauditable due to the nearly pathological level of secrecy that prevents any royalty participant from ever knowing what’s in the pie they are sharing.

That secrecy runs both upstream, downstream and across streams. And as we all know, keeping secrets from your partner is the first step on the road to ruining a relationship.

But before you get too deep into nuances, let’s start with a basic problem with the entire revenue share approach. In order to get to a per unit royalty, you have to multiply one dynamic number (the revenue) by another dynamic number (the usage). Meaning that the thing being multiplied and the thing by which it is multiplied change from month to month. The only constant in the formula is the actual percentage of the pie payable to the rights owner (50% in our example).

Remember–this all started with the digital service proposing that artists, songwriters, labels and publishers should take a share of what the service makes. If you have a significant catalog, however, you do what you do with everyone who wants to license your catalog–you require the payment of a minimum guarantee as a prepayment of anticipated royalties (also called an “advance”).

So in our simple example, if the service is pitching that they will invest heavily in growth and make the catalog owner $50 over a two year contract, the catalog owner is justified in responding that however much confidence they have in the service, they’d like that $50 today and not a burger on Tuesday. The service can apply the $50 minimum guarantee against the catalog’s earnings during the term of the contract, but if the minimum guarantee doesn’t earn out, the catalog owner keeps the change. This shifts the credit or default risk from the catalog owner partner to the digital service partner (who actually controls the fate of the business).

But–given the complexity of the revenue share calculations, at least three questions arise:

Question: How will creators ever know if they are getting straight count from the service due to the complexity of the calculations?

Answer: The vast majority will never know.

Question: How will anyone know if the advance ever recoups with any degree of certainty if they cannot verify the revenue pot they are to share?

Answer: The royalty receiver has to rely on statements based on effectively unverifiable information.

Question: And most importantly, if streaming really is our future as industry leaders keep telling us, then which publisher wants to sign up for a lifetime of explaining the inexplicable to songwriters and artists who question their royalty statements?

Let’s Get Rid of Revenue Share Deals

There’s really no reason to keep this charade going any longer. If the revenue share deal was converted to a penny rate, life would get so much easier and calculations would get so much simpler. There would be arguments as always about what that penny rate ought to be. Hostility levels might not go away entirely, but would probably lessen.

Transaction costs should go down substantially as there would be far fewer moving parts. Realize that it’s entirely possible that the transaction costs of reporting royalties in revenue share deals (including productivity loss and the cost of servicing songwriters and artists) likely exceeds the royalties paid. My bet is that the costs vastly exceed the benefits.

And the people who really count the most in this business–the songwriters and artists–should have a lot more transparency. Transparency that is essentially impossible with compulsory licenses.

Because when you take into account the total transaction costs, including all the correcting and noticing and calculating and explaining on the publisher and label side, and all the correcting and processing and calculating and messaging that has to be done on the service side, surely–surely–there has to be a simpler way.