MusicTechPolicy readers will have seen my post about the interest rate paid by the MLC on the rather sizable black box of “unmatched” funds sitting at a bank account (rumored to be City National Bank in Nashville).

That rate was modernized in the Music Modernization Act to be a floating rate: The Federal short term interest rate essentially set by the Federal Reserve. In fact, that particular federal rate is one of the lowest interest rates set by the Federal government and is the kind of interest rate you would want to be obligated pay–very low–if you knew you’d be in the business of holding large sums of money that you wanted to earn interest on yourself and make money on the spread, often called “the float.” (The black box is usually free money, so it’s actually an improvement.). For example, the bank prime loan rate is currently 5.5% that may be a good indicator of what you could get in the way of relatively risk free interest for a big lump sum–if not better for a really big lump sum, say $500,000,000.

The MLC is not, after all, the government, however much that fact might be lost on them. Why should the lowball government rate apply to the MLC instead of a competitive bank rate? Particularly when it comes to the substantial unmatched funds that songwriters and publishers are forced by the government to allow the MLC to hold and for which they control distribution–a bit of the old moral hazard there.

Indeed, you could also express that rate of involuntary saving as “prime plus x” where “x” is an additional money factor like 1%, so the rate floats upward to the songwriters’ advantage. Get some inspiration for this by looking at your credit card interest rate.

You probably have heard that the Federal Reserve is increasing the federal funds rate, and therefore all interest rates that are a function of the federal funds rate including the short term rate that the MLC is required by law to pay on the black box. The Federal Reserve is expecting to keep making significant increases in the federal interest rates in an effort to get inflation under control, which means that the MLC’s black box interest rate will also continue to increase significantly.

A quick recap: The MLC’s short term interest rate was 0.44% in January in keeping with then-prevailing Zero Interest Rate Policy (or the “lower bound”) of the Fed for the easy money years since the crash of 2008. But in August 2022 (that is, now) the MLC’s rate has increased to 2.84% monthly. The modern black box holding period in the Music Modernization Act is pretty clear:

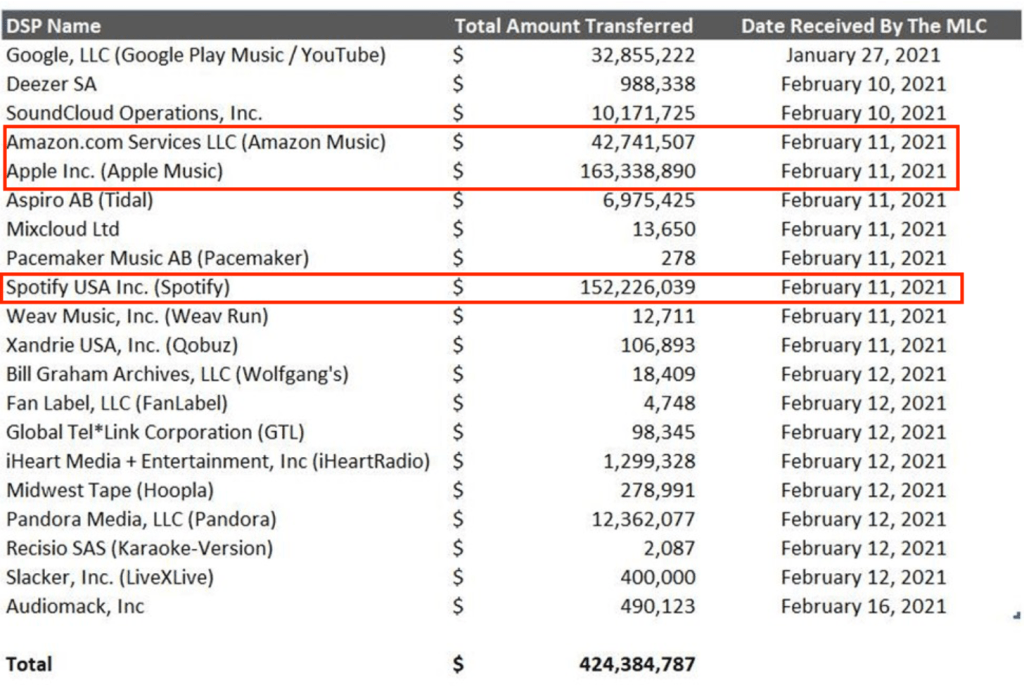

Also recall that the black box is to be held for an arbitrarily modern period of time while the MLC attempts to locate the rightful recipients as is their statutory burden under the MMA. Different numbers are thrown around for this holding period, but a three year holding period seems to be popular and has the benefit of having been modernized in the Music Modernization Act itself (see above). Bear in mind that the first tranche of “historical” black box (“historical” means “late” in this context) was $424,384,787 and was paid in February of 2021–nearly 18 months ago.

Also recall that we were not given any information that I am aware of as to when the services paying this rather large sum of other people’s money first accrued the black box. People who line up on the shorter holding period side of the argument generally favor rapid market share distributions which tends to help the majors; people on the longer holding period of time generally favor redoubled efforts to find the people who are actually owed the money.

The third group is that the MLC should simply find who is owed the money, have the money being held earn the highest rate of risk-free interest possible, and pay all of the interest money to the correct people when found and not have this cutesy limitation on the money factor paid out for holding OPM. Their argument goes something like your government takes away my right to negotiate my own rates, tells me how much I can charge, then makes it difficult to find me but easy to use my song and now you also want to take away the money you say I’m owed and give it to rich people I don’t know before I’ve had a change to claim it and pay yourselves to not do your jobs?

So we are at the midpoint of the three year statutory holding period. Although remember that this is a two pronged holding period of the earlier of 3 years after the MLC got the cash or 3 years after the date the service started holding the money that it subsequently transferred–a different holding period which would likely end sooner than the date the money was transferred to the MLC.

Although we know the date that the money was transferred in the aggregate to the MLC we may not know exactly when the money was accrued without auditing (although you would think that the MLC would release those dates since the timing of the accrual is relevant to the MMA calculation).

According to my reading of the statute, the modernized interest rate would likely attach from the time the money was accrued by the service, so should have been transferred to the MLC with accrued interest, if any. This may be in lieu of or in addition to a late fee. Very modern.

This leaves us with a couple questions. Remember that after the holding period, the black box is to be transferred on a market share basis to all the copyright owners who could be identified based on usage, which includes usage under voluntary licenses that are not administered by the MLC.

So this raises some questions:

- Why should the black box be divided up amongst copyright owners who have voluntary licenses and who are not administered by the MLC? They presumably have the most accurate books and statements and may have already had a chance to recover.

- What happens to the accrued interest at the time of distribution? Why should the market share distribution include interest on money that didn’t belong to the recipients?

- The statute takes the position that the MLC must pay the interest rate but is silent on how much interest the MLC can earn from the bank holding the substantial deposit of the unmatched monies. There’s nothing that requires the MLC to pay over all earned interest.

Here’s a rough justice calculation of 3 years compound interest at current rates with steadily increasing black box. While the holding period started at the .44% rate, I ran the numbers at the 2.84% rate because it was easier–but also left out an estimate of the increase in rates that is surely to come. Since we are at the midpoint of the holding period already, this gives you an idea: