The Copyright Royalty Judges have announced that the new COLA-adjusted minimum statutory rate for 2026 is 13.1¢ for physical and downloads, up from 12.7¢, effective 1/1/26. This is the last year of the Phonorecords IV rate period, so that’s an increase from the 9.1¢ frozen mechanical rate that had been in effect for 15 years.

The adjusted rate stands in stark contrast to the streaming mechanical which not only has been frozen for the entire 5 year rate period, but has actually declined substantially due to Spotify’s bundling silliness. That smooth move has set up what will no doubt be a donnybrook in Phonorecords V, i.e., the next rate proceeding which is due to start any minute now (actually more like January, which is close enough).

It must be said that the reason there’s a rate increase for physical/downloads is due to the efforts of independents who filed two rounds of comments in Phonorecords IV and also the willingness of the labels to be flexible and reasonable. I suspect that has a lot to do with the fact that at the end of the day, we are all in the same business and it’s to everyone’s advantage that songwriters thrive. Obviously, the same cannot be said of the streaming platforms like Spotify that are busy seeding AI tracks with both hands. I really don’t know what business those people think they are in, but it’s not the music business.

We are rapidly approaching the next rate-setting proceeding before the three-judge panel at the Copyright Royalty Board for the royalty payable to copyright owners (and ultimately to songwriters) for exploitations of songs. These proceedings set rates for the next five year period and are numbered to tell them apart. The last proceeding, for example, was styled “Phonorecords IV” or sometimes “CRB 4” for those who struggle with long words. (Using the “CRB” acronym instead of “Phonorecords” is actually misleading because the CRB sets a number of rates.)

The proceedings will likely be divided in two: One proceeding for songs exploited in physical records like vinyl, CDs and permanent downloads and one proceeding for streaming mechanicals. These hearings are simultaneous and not sequential, so each hearing will be conducted side by side.

One reason for these simultaneous hearings is that the participants in each of the proceedings differ–the physical/download participants are songwriters and publishers on one side and the record companies on the other. The streaming participants are (often) the same songwriters and publishers on one side, but the streaming services are on the other.

The participants are incented to reach a voluntary settlement that they then present to the Copyright Royalty Judges for approval. The settlement negotiations are largely conducted in secret and no one on the songwriter side except a couple of participants knows anything about the terms of the settlement until it is presented to the Judges and the Judges make it public.

At this point, the Judges are required to entertain comments from the public as to whether the public supports the settlement (as required under a federal law applicable to all of the administrative state agencies from the Environmental Protection Agency to the Social Security Administration to the Copyright Royalty Board).

No matter how much some of the publishers would like to spin it, it is this public comment step where it all began to fall apart during the last proceeding styled “Phonorecords IV”, particularly over the “frozen mechanicals” issue. Signally, this disintegration of the initial physical/downloads “settlement” attracted a prairie fire of public comments that rejected the authority of the NMPA and NSAI to speak on behalf of all songwriters and publishers and also rejected the side deal that these groups had negotiated with the labels. The Judges listened, and the Judges rejected that settlement–I believe for the first time in the history of the rate setting proceedings.

The same was not true of the streaming mechanicals piece, however. I never did read a well-reasoned explanation for why participants lacked authority to speak on behalf of all songwriters, i.e., beyond their own members, in the frozen mechanicals proceeding, but that authority could not be questioned in the streaming proceeding. It should have been apparent to anyone paying attention that any consensus behind the time-encrusted “Big Pool” royalty calculation method for streaming mechanicals was rapidly crumbling apart. The Judges’ “39 Steps” royalty calculation is as mysterious as a Hitchcock movie and many did not trust it. And more importantly for our discussion today–still do not trust it at all.

As we approach Phonorecords V, there are some fundamental questions that all involved need to be asking themselves. The first is whether we want to go back to the same tired process of secret meetings with the big reveal resulting in public hostilities in the comments–against what is ostensibly our side. This before we even get to the negotiation with the other side.

The powers that be had the chance over the last few years to bring in some different viewpoints. Had they done so, they would have both diffused the inevitable collision, but could also have gotten the benefit of those viewpoints when there was still time to build alliances. There’s an idea–an integrative negotiation with a collaborative outcome.

Another fundamental question is whether we can reach a fairly quick deal with the labels on the physical/download side so that all concerned can turn their attention to bringing the streaming rates into some semblance of reality. Because the songwriters did such a persuasive job of raising the frozen mechanicals rates from 9.1¢ to 12¢ plus a COLA, that minimum statutory rate has now increased to 12.7¢. Given current inflation projections, it’s likely that the statutory rate will increase to about 13¢ and change by the end of 2026.

If a settlement could be reached quickly, it would not surprise me if someone came up with the idea of simply taking the then-extant minimum rate (for 2027) as the new base rate for the first year of Phonorecords V (2028) plus extending the annual COLA to protect songwriters in the out-years of PR V. Wherever the actual penny rates end up, if the songwriters and labels could reach an agreement quickly, it would save a bunch of effort and allow everyone to turn their attention to the streaming rates.

I wonder if it’s even possible to reach a negotiated settlement with the streaming services on the streaming mechanical. The entire concept of the “Big Pool” royalty rate is failing for streaming on both the sound recording and the song side of the deals. It was, frankly, a silly idea to begin with–and that takes us back to the beginning of streaming when deals were poorly negotiated with little to no accountability because physical still paid the bills. The general idea was that “superfans” would rule according to Thomas Hesse in Billboard who was around at the time: “If you get to superfans, who listen to music all the time, you get to all the money — not just from those people, but you get all the money from everybody.” The reality is that you can replace “superfans” with “superstars” or more simply, “market share”, and you would have a much better understanding of the “Big Pool” concept. The Big Pool is actually just a hyper efficient marketshare distribution of a pool of money.

What Spotify has demonstrated with their short sighted move on bundling is simply all the reasons why they are disliked and untrustworthy. They said the quiet part out loud–we have no idea what we are doing in this business but we–and not songwriters or musicians–are getting stupid rich at it. It is unlikely that anyone is going to welcome more of the same in Phonorecords V.

What is becoming apparent to an increasing number of songwriters is that there is one metric that matters to Spotify’s CEO–stock market valuation. That is what has made him a billionaire. That is what has made plenty of people at Spotify into millionaires. That is also the one metric that songwriters and artists have never participated in. Our negotiators have had their eye on the wrong ball.

I say if we’re going to spend millions on the government’s rate proceedings anyway, let’s get something for it for a change, shall we?

When I made the soft call for impending stagflation last October I had no idea that that it would hit the US economy with such force and speed. The trends were, frankly, obvious and the signs unmistakable. But it’s the speed with which stagflation struck that I didn’t expect. We have seen each step of stagflation’s three point play undeniably demonstrated in real life and the result is inflation as far as the eye can see.

Stagflation’s Three Point Play

The return of 1970s style stagflation and the now-confirmed recession along with Federal Reserve “quantitative tightening” could mean policymakers recognize the need to end the easy money policy that has been in place since “quantitative easing” began around 2008. Arguably, the global economy has been in a post-Big Short bubble ever since, with the inevitable growth in the money supply that provided “too much money” that was chasing “too few goods.”

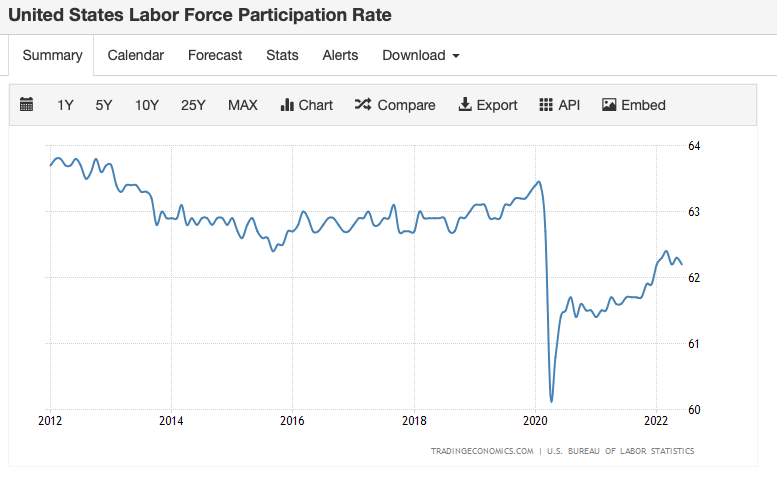

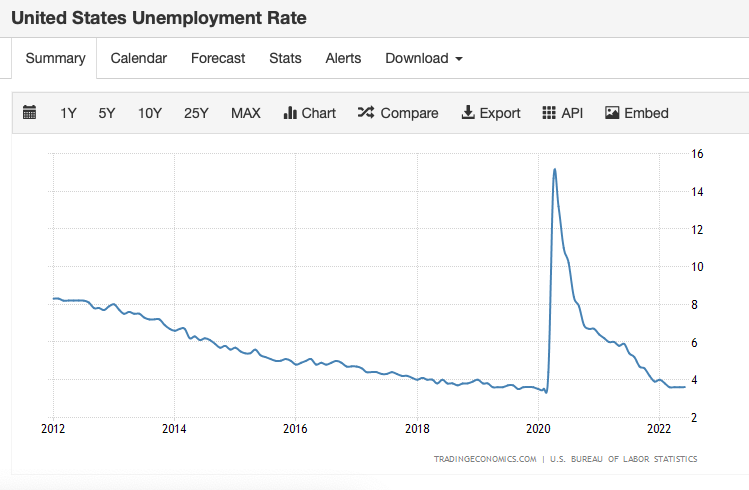

A recession and stagflation call is mitigated by the unemployment rate (which was about triple current rates during the 1970s), which itself is mitigated by the labor participation rate. A ten year view shows that the labor participation rate is still below pre-pandemnic levels even though the unemployment rate has been steady in the recent past. Yet even Y Combinator (that famously wanted to “Kill Hollywood” starting with the unions) warns of investment drying up for startups, but we’re not quite at the point of limited partners refusing to show up for capital calls at major VCs.

Inflation has, of course, been inevitable as has been the commensurate rot of inflation on the buying power of consumers. There is little doubt that inflation has been a long-term trend in the U.S. for quite some time and is likely to be with us for a good long while longer. For songwriters, if you’ve been following the rate increase confirmed in Phonorecords III, imagine what the rates would have been had the rates been indexed in this inflationary environment. We can understand how they missed indexing on Phonorecords III, but they cannot miss it on Phonorecords IV–or give it away as a bargaining chip.

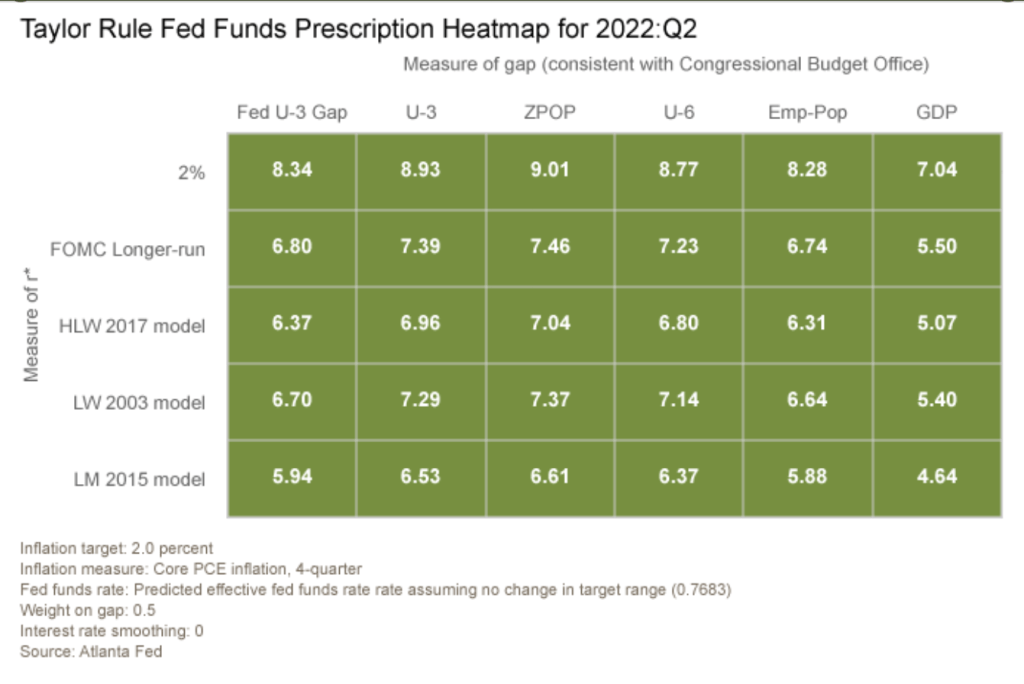

Realize that one accepted method of extinguishing inflation is the “Taylor Rule” implemented by Federal Reserve Chairman Paul Volker in the 1970s for which Presidents Carter and Reagan took tremendous political heat–raise interest rates OVER the inflation rate. (Which is why there was a 21% prime rate–think on that.).

Source: Atlanta Federal Reserve

It was a different country then–America was a creditor nation. No longer true. Of course that’s not likely to happen today because of all the government borrowing during the easy money era. If the government had to pay a rate over the current 8.7% inflation rate, the government would collapse. It is likely that high inflation will be with us for a long time to come.

Being aware of the inflationary economic environment is a critical issue for songwriters in the US who are in the middle of a government rate setting proceeding before the Copyright Royalty Judges at the Copyright Royalty Board in Washington, DC. Songwriters at least have the opportunity to include a cost of living adjustment in the government’s rate and have asked for it in the streaming proceeding. Remember, there are two rate proceedings underway: One for physical mechanicals and downloads and the other for streaming. Songwriters, publishers and labels are in the physical and downloads proceeding. Songwriters, publishers and Big Tech are in the streaming proceeding soon to go to trial.

Credit where credit is due, Universal, Sony and Warner labels have included an annual CPI adjustment (or “indexing”) for songwriters in their voluntary agreement to raise the previously frozen mechanical rate for physical and downloads. The Copyright Royalty Judges also included indexing in the rate for webcasting of sound recordings that they recently decided (Web V). Many of the same Big Tech services were parties to Web V but are now arguing against CPI for songwriters in Phonorecords IV. Different hearings, true, but a lot of overlap in the parties and their smug little straight faces.

In our stagflationary economy, an agreed-upon inflation adjustment is a fairness making term that doesn’t make songwriters eat all of the inflationary rot from cost increases for “food at home” and force them to predict those price changes five years in advance. Indexing helps to fix that guess work in what is already a process of educated guessing in the non-existent willing buyer/willing seller folie à deux.

An inflation index is a particularly crucial tool when songwriters are prevented from stepping away from a deal because the government forced a deal upon them, like any statutory rate or in countries where there is a tariff or other compelled agreement.

Failing to use indexing makes the fairly controversial assumption that economically rational songwriters would charge a fixed price regardless of the fluctuations of the cost of energy, food and rent. By using the government to impose a non-indexed rate, there is a government-mandated implied discount that accrues to the benefit of the services, aka the largest companies in commercial history who just can’t bring themselves to treat songwriters fairly.

But want to bet these failures will have no impact on the services’ ESG scores on Wall Street?

Take Google for example, flatly rejecting indexing on the streaming side of the CRB proceedings:

“None of Google’s agreements with music publishers contain CPI adjustments for the [Per Subscriber Minimums] contained in those agreements. The Copyright Owners’ proposed CPI adjustment to PSMs is simply unsupported by marketplace evidence.” https://app.crb.gov/document/download/26528

Google is, as usual, full of it and is gaslighting the CRB with inapt arguments. Google is in a rate proceeding where the government—not Google—sets the terms. I know that line gets a little blurry for Googlers given how much strangulation Google sustains over government through its vast network of lobbyists, revolving door men and women, consultants and on and on and on.

I also know that Google would love nothing more than to dictate the terms to the government because Google has not-unjustified delusions of grandeur in this regard due to their mind-blowing level of brazen influence peddling. It’s not just Google, it’s all of the Big Tech oligarchs, the latter day Xerxes who seek to overwhelm creators through lawfare—songwriters are just low hanging fruit because of the ancient compulsory license—Section 115 of the Copyright Act—that is ready made for Big Tech’s copyright abuse.

But Google is not the government. It is the Congress and not Google that created Section 115 to interfere with private contracts and more importantly interfere with the right to privately contract. That’s a big deal in the US.

So, the issue isn’t what Google may have done in contracts with a totality of vastly different terms in a completely unrelated setting. It’s whether the government is paying just compensation for taking away rights under the Constitution of the United States. More specifically the 5th Amendment “takings” clause.

And the government’s compensation to songwriters is not just. It never has been.

Remember that at the heart of this process, the Judges are required to set a price for songs that the Judges believe reflects what a willing buyer would pay a willing seller in a transaction that has been devoid of willing buyers and sellers for over 100 years.

Google and other Big Tech DSPs in the CRB present the Judges with benchmarks based on prices that are not only distorted by years of abuse to begin with but are permanently disfigured. Remember, the government set the mechanical rate at 2¢ from 1909 to 1978 and had raised it very slowly ever since while at the same time pretending that the distortion of the 2¢ rate did not exist.

This deep 2¢ hole that songwriters are digging out of may not be the only reason songwriters are so poorly compensated, but this “tuppence” era definitely is a contributing factor. So whatever value-based rate increase that songwriters can claw out of the Big Tech services must be supported by a cost of living adjustment measured by the CPI just to tread water.

Price is truth if prices are truthful. And undistorted.

Otherwise, it’s just frozen mechanicals by another name, and Big Tech is simply free riding on the government’s license due to their outsized lobbying influence and government capture. (Need we name names?)

The songwriter is simply subsidizing the biggest corporations in commercial history.

It looks like the statutory rate for songs on compact discs and vinyl is finally going to get a significant increase starting January 1, 2023 (assuming the Copyright Royalty Board approves the settlement proposed by the major labels and the publishers). We have to acknowledge that there are many independent record companies that have never had to deal with an increase in the mechanical rate–the old 9.1¢ rate has been in effect since 2006. If a label was founded any time after 2006 the issue just hasn’t come up before.

The new rate (which may well change every year of the 2003-2007 rate period due the cost-of-living indexing) will require labels to check their royalty accounting programs to make sure they change the rates as required. It will also become an audit point for artist audits by artist/songwriters or producer audits by producer/songwriters, and of course publisher audits as well.

But there’s also a question of how to address what I call the “controlled comp squeeze” caused by the collision of rate fixing dates with the new rate as applied to outside writers. (I’ve posted a bunch on these topics, so if you don’t immediately recognize what I’m getting at, I refer you to those posts.)

In addition to the controlled comp squeeze, the conversation should include what to do about the entire controlled compositions concept, a contract clause that only applies to the US and Canada and a concept that is anathema to ex-US and Canada songwriters and collecting societies. Because digital recordings are typically paid at the full statutory rate (or should be), controlled compositions clauses are really a feature of physical configurations.

There’s a feeling out there that the entire concept of controlled compositions should be abandoned. Since record companies have come to rely on certain economics when they decide to keep titles in print and not to cut them out, i.e., stop making them available to retailers, it is important to understand what effect that trying to force labels to pay every song at full rate will have on the music economy, especially for independent labels that sell a disproportionate number of vinyl units. Sudden increases in royalty costs could have dire consequences for the people who frequently are the main investors in certain genres of music and have the least ability to lobby for their interests, so we should tread prudent in rebalancing the songwriter economy.

One intermediate step might be to take a cue from a business practice in Canada called the “Mechanical License Agreement” that has worked very well for many years. The “MLA” offers protections from the worst terms of the controlled compositions clause and was a voluntary agreement between the labels and the CMRRA (Canada”s mechanical collecting society).

2011 Interview with David Basskin

The MLA originated with David Basskin, the former head of CMRRA, and David negotiated the MLA with the major and independent labels in Canada. You can listen to my 2011 interview with David on SoundCloud.

The principal terms of the MLA cover the rate (which was no less than 3/4 rate but that dog won’t hunt anymore, plus after 1988 Canada did not have a statutory rate like the US does), free goods limited to 15%, no reduction for outside writers paid at full rate.

1. Full Rate: Songs should be paid at the full applicable rate and should be paid on standard sales plan LP free goods (a common give if the artist/writer is signed to a publisher affiliated with the record company);

2. Cap: Rather than a contract rate of 10 or 11, the MLA pegs the cap at 12;

3. No Rate Fixing Date: The rate not only is full, it also floats so there is no concept of a rate fixing date and should apply retroactively and prospectively; and

4. Floor: The application of the cap cannot result in any song being paid less than 50% of the full rate (which could happen on multiple disc or box sets).

There are other bells and whistles, but these are the main points.

While I understand that a record company would want to cap their mechanical royalty expense, any one of these terms would further that commercial goal. It is the application of all of the controlled comp terms that make the clause so onerous.

While the Copyright Royalty Board can set the rates, I doubt that they have the jurisdiction to address private contracts. Congress could pass legislation, but I think that would be a bitter struggle and I’m not so sure I want Congress to be micromanaging the music business any more than they already do with statutory rates and rate courts.

But there’s nothing stopping a voluntary agreement.

As readers will recall, I’ve been beating the drum about inflation and stagflation coming home to roost for many months, nearly a year now. These posts are in the context of the compelling need for a cost of living adjustment for songwriters’ statutory rates and the absurdity of a frozen mechanical for the booming vinyl and CD configurations which thankfully has now been rejected by the Copyright Royalty Board once and for all.

When you force songwriters to license and also force them into accepting a government rate for mechanical licensing set by a little intellectual elite in a far-distant capitol, the last thing that’s fair or reasonable is to unilaterally freeze those rates when songwriters are staring down the worst inflation in 40 years. This is particularly galling when rampant inflation was all entirely predictable and the smart people and the economists they supposedly consult with just missed the boat.

Why do I say that the current inflation was entirely predictable? I’ve promised a few times to discuss quantitative easing so here it is. As you read this post, remember that both the current story on inflation and the need to index the statutory mechanical rate started in 2008 with the Great Recession and has been coming for at least fourteen years–plenty of time to recognize that the answer to inflationary destruction of a rate songwriters are forced to accept was not to freeze the rate to make the inflationary destruction even worse. Rather, the answer was to index the rates to inflation at a minimum. Indexing would at least preserve purchasing power if the government was not willing to provide an actual increase based on value. The central bank policy known as “quantitative easing” and its corresponding zero interest rate policy guaranteed the rot of inflation was inevitable.

Printing Too Much Money

Start with the definition of inflation we all have probably heard: Too much money chasing too few goods. When you hear this, some people think of the transaction on the consumer level, as in too much consumer money chasing goods in a productivity decline, aggregate inventory mismatch or raw supply shortage.

But that’s not the fundamental question–how do you get “too much money” in the aggregate across the entire economy at the same time? The way you always do; the government increases the money supply by putting too much money into circulation. The old fashioned way of doing this was literally printing paper money, but the terribly modern digital way of doing it is called “quantitative easing” which has the same inflationary effect because it is effectively the same thing as printing paper money. (The powers that be also refer to it as “QE” like it’s a cute little puppy or a Star Wars android. It’s not so we won’t.)

The difference between old school and new school is that instead of printing money that ends up in bank accounts of those guarantors of the full faith and credit of the United States–that guarantor is the person you see in the mirror–the Federal Reserve created digital money and they gave it a Fedspeak name that conveyed no information about what was really going on. They called it “quantitative easing” which is right up there with “Department of Defense” and “late fee program” in Orwellness. It’s quantitative because it digitally creates money on the books of the Federal Reserve and it’s easing because easy money. The Fed also cut interest rates to near zero (the “lower bound”) and some would argue they essentially created negative interest rates, all in the name of financial stimulus that Congress–i.e., elected officials we vote for–didn’t vote for.

This quantitative easing started out in 2008 to be an emergency method of propping up the economy after the last time that Wall Street screwed things up on a grand scale in the 2008 financial crisis.

What was supposed to be a short term fix is still going on to this day 14 years later. So the unelected smart people who deal with the Copyright Royalty Board (also not elected) must have known this was coming and that the last thing you would want to do was freeze rates when the watchword in the general economy was “stimulus”.

The combination of the Fed’s quantitative easing and the Fed’s zero interest rate policy caused one of the greatest asset bubbles in the history of mankind. And when you hear that the Fed is now increasing interest rates and simultaneously “reducing its balance sheet” by selling about $1 trillion of government and corporate bonds, this is what they are talking about. Many think that the only way of getting out of this bubble is to either raise taxes–fat chance–or raise interest rates and reduce the money supply. The truth is, the U.S. has never been in this exact situation before so no one really knows what will work, but we do know what has worked before. And wage and price controls such as freezing the statutory rate does not work (as President Nixon discovered in 1971). Of course if you wanted to fix the problem by properly aligning incentives, songwriters could have told their publishers that for every 1% increase in inflation, they could reduce the salaries of the smart people by 1% until the freeze comes off. That’s called incenting the wrong people to do the right thing. Like that will happen.

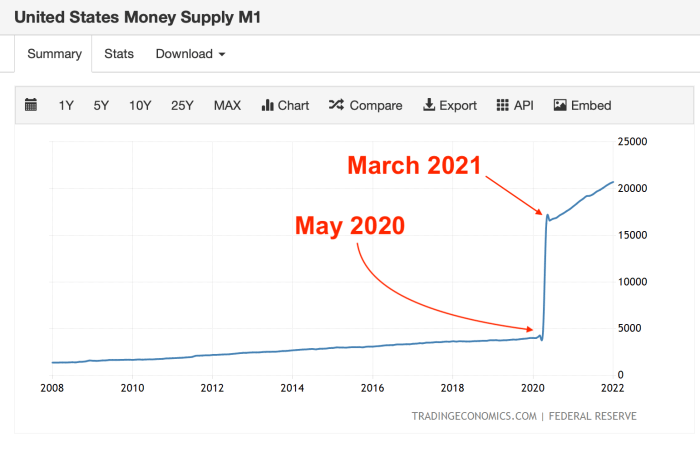

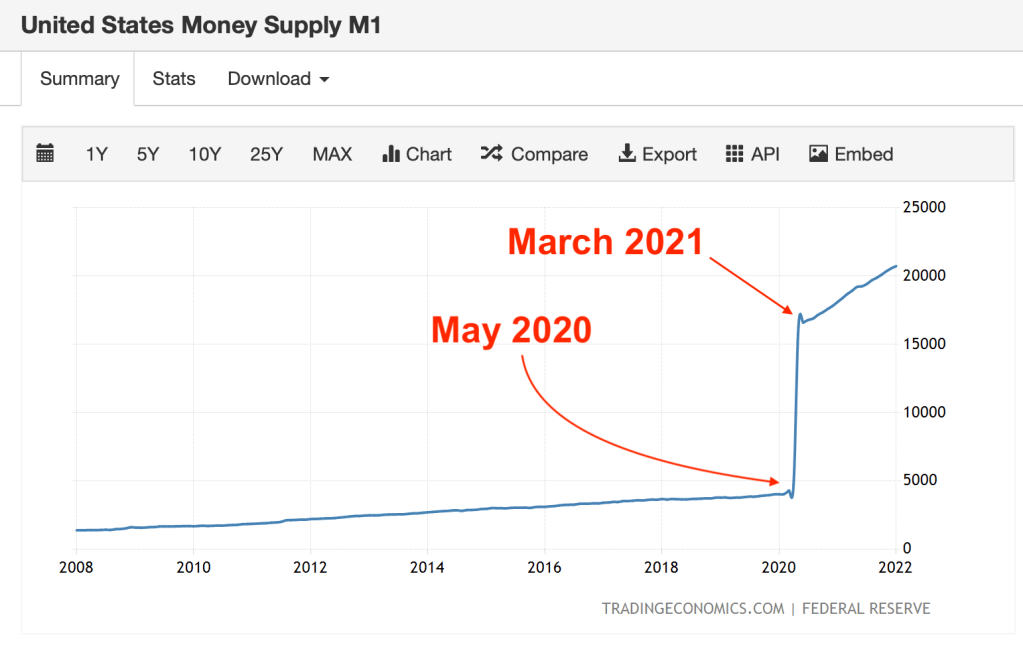

So time for charts. Back to the “too much money”, let’s look at the basic money supply often called “M1” and remember–inflation is not a cause of the growth in the money supply, it is a symptom of the government printing too much money. Because you have to have money to chase goods, right? And the money only comes from one place.

As you’ll see in this snapshot of the growth of M1 since 2008, there’s fairly steady growth until it hockey sticks in 2020 and continues after the $1.9 trillion American Rescue Plan passed in March of 2021. More on economist Steve Rattner’s take on that coincidence later.

Remember, the U.S. central bank (called the “Federal Reserve” or “the Fed”) has two tasks in its mission: Keep inflation and unemployment low. The Fed historically has two “weapons” to control the economy to accomplish its mission: interest rates (especially a targeted “federal funds rate”) and the money supply.

The money supply is going to be our focus in this post, but it wasn’t much of an issue at the Fed until the financial crisis of 2008 when the Fed introduced “quantitative easing.” The growth of the money supply has become a significant issue since COVID and especially since 2021.

How the Fed Injects Too Much Money in the Economy

The way the Fed typically increased the money supply before quantitative easing was by buying Treasury notes or other liquid assets in the open market or by actually printing more currency which was distributed in the real economy through retail banks. (Remember we separated banks between retail and commercial during the New Deal in the Glass Steagall legislation. Read up on that separately, beyond our scope here.) Most of the Fed activity before 2008 has been focused on tinkering with the interest rates that the Fed controls, often the “Federal funds rate”.

Increasing the money supply before quantitative easing typically lowered interest rates, put more money in the hands of the consumer and stimulated business activity—including loaning money to other retail banks–through an increase in aggregate demand. Lowering interest rates expands the economy by making money cheaper; raising interest rates contracts the economy by making money more expensive. The Fed can decrease the money supply by selling Treasuries in the open market which is another way to control inflation, or try to anyway. This is also called reducing the Fed’s “balance sheet” (securities held by the Fed) and tends to raise interest rates. If you follow the financial press, you’ll hear a lot about that currently.

When demand is high, i.e., economic activity heats up, the Fed typically raises interest rates to avoid high demand becoming hyper inflationary. (People often use post WWI Germany as an example of hyperinflation when workers were paid a few times a day to avoid their money losing value by the time they got off work–yeah. Think on that when you buy gasoline or groceries this week.) The Fed also may largely leave the money supply alone. When demand is low or collapses, as has happened in various financial crises such as the Great Recession, the Fed may lower interest rates to encourage demand with debt-driven economic activity by consumers and firms—and, of course the government. We’ll come back to the government part.

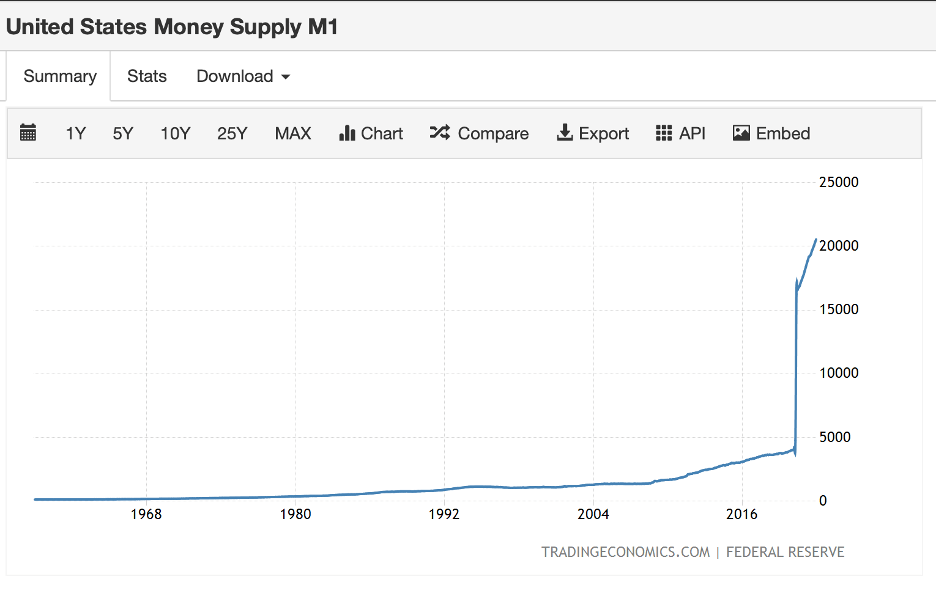

The Fed historically has let the money supply grow at a relatively steady rate. The growth of the M1 (M0 plus demand deposits less reserves) looks something like this which makes that 2020-2022 hockey stick look even more pronounced:

What do we remember most about the financial crisis? I don’t know about you, but the event I remember most was the first time I heard one of the newsreaders utter the word “trillion” as a modifier for “dollars.” I remember that like I remember where I was on 9/11. And I also remember what I thought at that moment—these numbskulls are going to bankrupt the lot of us because it’s the government. When it comes to a trillion dollars, it’s betcha can’t spend just one. (Fast forward a few years to the Speaker of the House saying with a straight face, “if they come up a trillion, we’ll come down a trillion.” And they give you that look like they just said something smart. Insane.)

But I digress. Quantitative easing was a workaround to get more cash into the financial markets. Not in your bank account, but into Wall Street. How so?

Some Mechanics on Quantitative Easing

Remember, the Federal Reserve is responsible for controlling the money supply. The civics class version of this story is that the Treasury Department prints the money. When the Federal Reserve actually prints currency, it submits an order to the Treasury Department’s Bureau of Engraving and Printing then distributes that newly printed currency to the thousands of banks, savings and loans and credit unions in the banking system. But you see the problem there? Someone at the Federal Reserve Board of Governors has to submit an order (which must be voted on) to the BEP, and then all those bankers know what’s going on.

Does that sound easy? Does that sound like a politically costless transaction? Why no, it does not. And that may be why that process is called printing money. So it’s not quantitative easing.

When the U.S. Government spends money—and it spends lots of money—it does it in two ways at a high level. It either takes in money in what are euphemistically called “revenues” or it borrows the money backed by the full faith and credit of the United States. Which means you and me. “Revenues” are also called “taxes,” paid by you and me. Borrowing means that you and I promise to pay interest and principal on U.S. Treasury bonds. But that means someone has to buy the bonds.

And therein lies the rub.

If the U.S. Government needs to sell $X in bonds but only has buyers for say 2/3 $X, what happens? Does the government say, I better cut that spending by 1/3? Oh, no, no, no. It doesn’t do that. What happens is that indirectly, the Federal Reserve buys the bonds that the government can’t sell to unrelated third parties.

Wait you say—do you mean that the Government is borrowing from itself? How can that be legal? Good question.

And here is where we need to understand an entity called a “primary dealer.” According to Wikipedia (because why not):

“A primary dealer is a firm that buys government securities directly from a government, with the intention of reselling them to others, thus acting as a market maker of government securities…. In the United States, a primary dealer is a bank or securities broker-dealer that is permitted to trade directly with the Federal Reserve…. The relationship between the Fed and the primary dealers is governed by the Primary Dealers Act of 1988 and the Fed’s operating policy “Administration of Relationships with Primary Dealers.” Primary dealers purchase the vast majority of the U.S. Treasury securities (T-bills, T-notes, and T-bonds) sold at auction, and resell them to the public.”

Primary dealers are trading counterparties of the New York Fed in its implementation of monetary policy. They are also expected to make markets for the New York Fed on behalf of its official accountholders as needed, and to bid on a pro-rata basis in all Treasury auctions at reasonably competitive prices.

Any guesses about which banks might be “primary dealers”? That’s right. Wall Street banks, like JP Morgan Chase (or JP Morgan Securities, more precisely), and that would not be the First Bank of Your Town.

Let’s say the New York Federal Reserve Bank has some treasury bonds to sell. A trader at the Fed calls a trader at JP Morgan to place an order to buy the treasuries for say $1 billion. (It will be a lot more but humor my dread of the “T” word.) The Fed then futzes with the JP Morgan reserve accounts and presto-changeo JP Morgan has more of this digital money to buy the bonds the government can’t sell.

Printing money? I think it is, but people will quibble about it, particularly people who could get blamed for that whole hyperinflation thing. And then there’s that whole Constitutional speed bump, but let’s not worry about that. I’m sure there’s no legal problems with the authority for quantitative easing. The smart people in the Imperial City said so and that must be true. Remember, the Federal Reserve isn’t directly elected by anyone.

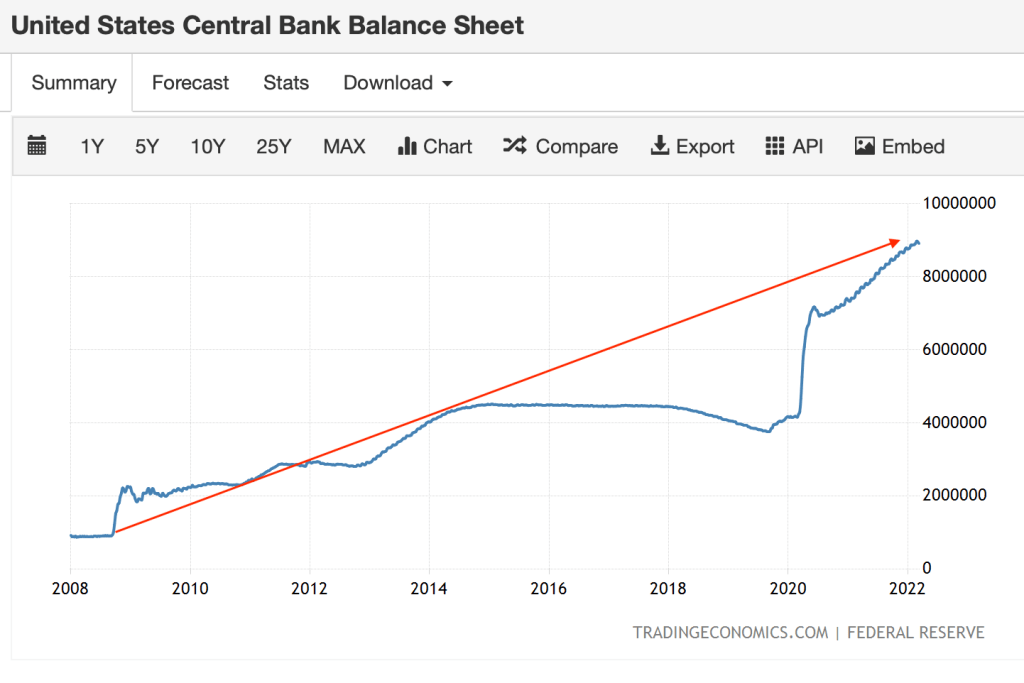

The Fed’s Balance Sheet

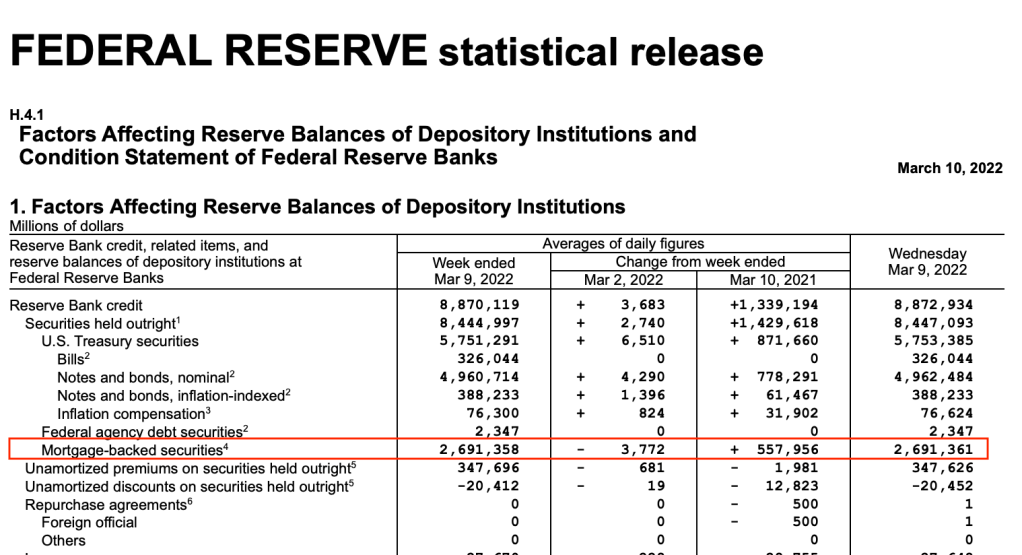

But that’s not the only thing the Fed has been doing during this 14 year period of quantitative easing. In addition to government bonds, the Fed has also been buying mortgage backed securities and other corporate debt in the open market. (That’s right–mortgage backed securities as in The Big Short. Feeling nauseated yet?) The Fed’s balance sheet since 2008 has looked like this:

The Fed actually publishes its balance sheet so that the taxpayers who can do little to nothing to affect the Fed’s decisions can at least see where the Fed spends the full faith and credit of the United States. A recent balance sheet looks like this:

After 14 years of quantitative easing, cutting interest rates to 1/4% (aka the “lower bound”) and buying securities we still have extraordinary inflation at rates not seen in 40 years. All of this was predictable as soon as the Fed started the quantitative easing program after the Great Recession and did not stop.

Various COVID relief spending programs compounded the inflationary effects as Steve Rattner stated in a widely-read op ed (Rattner was an Obama Treasury official and is a frequent go-to for the New York Times, Morning Joe and other programs):

[The Biden Administration] can’t say they weren’t warned — notably by Larry Summers, a former Treasury secretary and my former boss in the Obama administration, and less notably by many others, including me. We worried that shoveling an unprecedented amount of spending into an economy already on the road to recovery would mean too much money chasing too few goods….

The original sin was the $1.9 trillion American Rescue Plan, passed in March. The bill — almost completely unfunded — sought to counter the effects of the Covid pandemic by focusing on demand-side stimulus rather than on investment. That has contributed materially to today’s inflation levels.

Focused on the demand side, even most pessimists — me included — missed a pressing problem. Supply-chain bottlenecks have led to shortages of many goods, a crisis that has been exacerbated by the reluctance of Americans to return to work. The worker shortage has also hurt the service sector. Many restaurants, for example, remain closed because they can’t find workers. Both also spark higher prices.

Now, between the government payments and underspending during the pandemic, American consumers are sitting on an estimated $2.3 trillion more in their bank accounts than projected by the prepandemic trend. As they emerge from seclusion, Americans are eager to spend on everything from postponed vacations to clothing. But the supply chain breakdown has turned the simple act of spending money into a challenge.

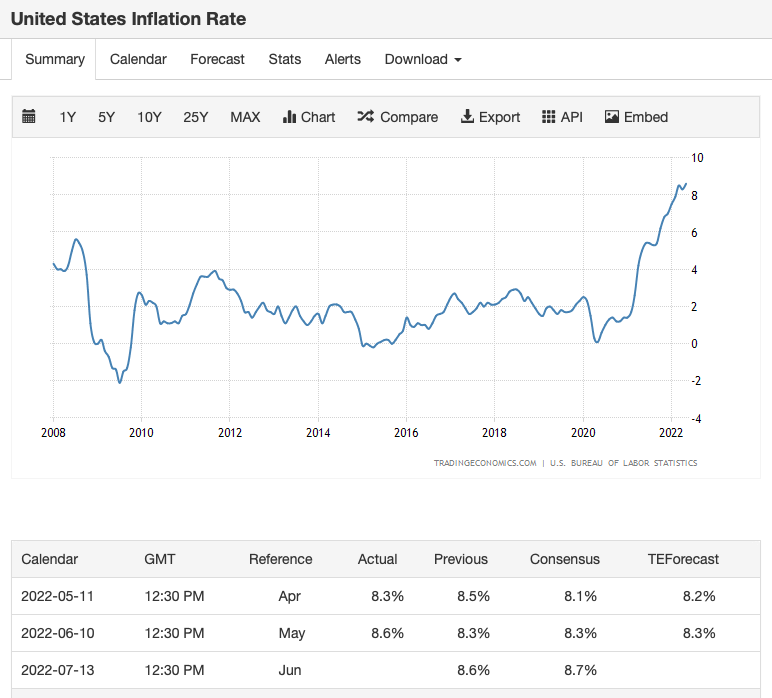

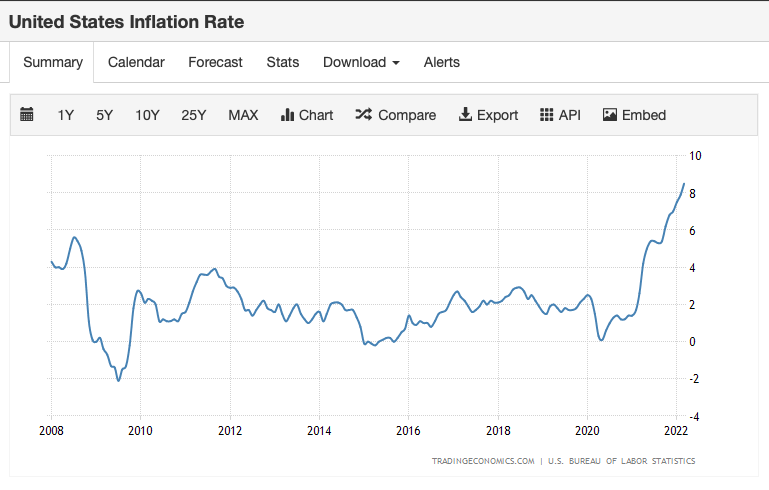

Mr. Rattner was writing in November 2021 before the onslaught of inflation in the first few months of this year and before Russia invaded Ukraine. The most recent inflation rate, a lagging indicator, tells the story (and notice the higher lows and higher highs over time):

The Easy Money Tax Comes to the Kitchen Table

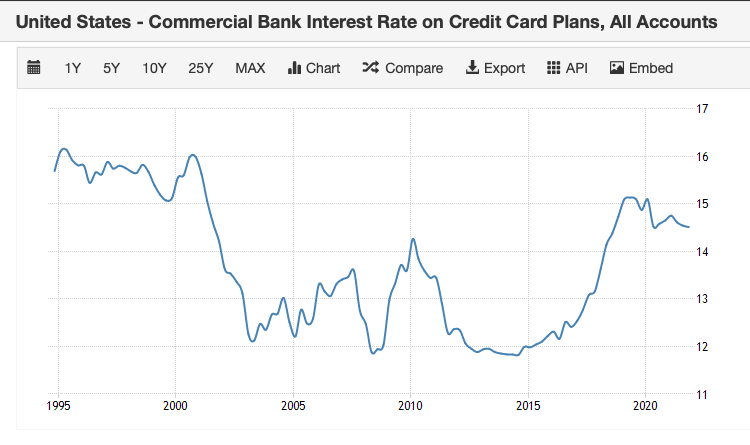

After inflating asset prices (like stocks and real estate) through quantitative easing, the easy money bubble is now coming to consumer goods. And what happens to consumers when there is a sudden price shock for consumer goods? They have to cover those goods in the short run in one of two ways–take on more debt (usually credit card debt) or spend their savings (called “dis-saving”). And a couple last charts:

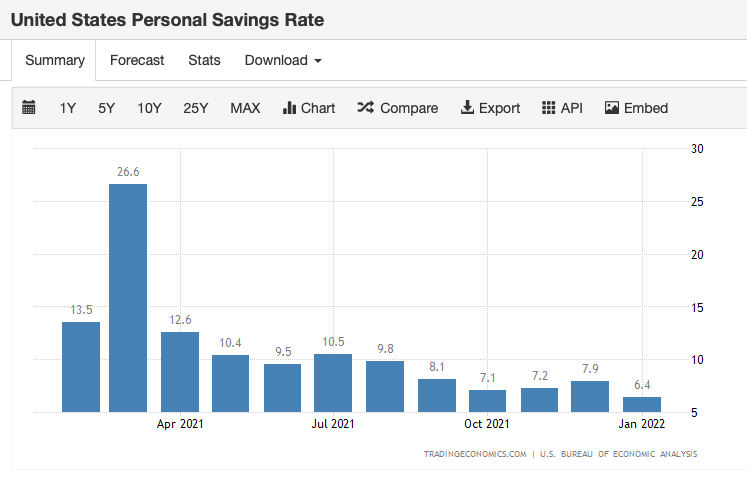

12-month view of personal savings

Savings shot up in March 2021 coincidentally at the time of the American Rescue Plan passing in March 2021 and have decreased ever since, and the saving’s rate is headed toward zero or at least the lower lows that it hit in the recession.

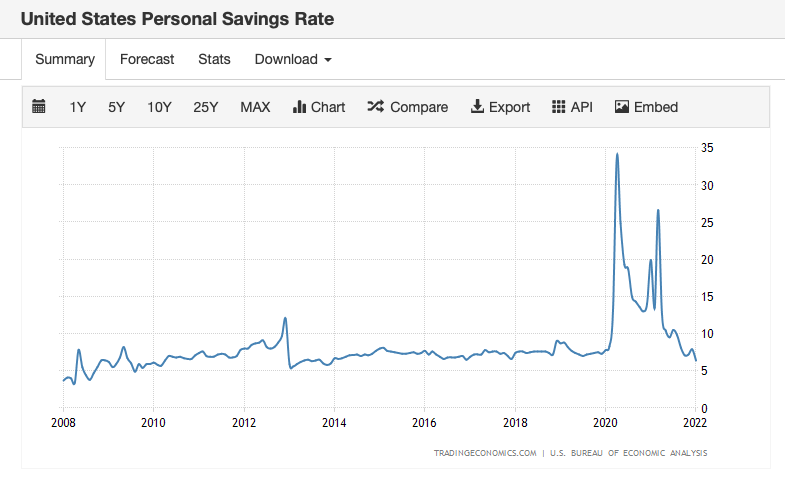

2008-present view of personal savings

And of course when savings decline to zero, out comes the credit card. What else does the Fed tell us will be happening starting this month? Interest rates will increase, which means that credit card interest rates will may well trend higher interest rates just at the moment that consumers will be increasing debt.

Remember, savings deposits were made in historical dollars but are spent on goods and services in inflated dollars, so there is essentially a implied tax on dis-saving. The same is true of running high credit card balances on inflated goods, particularly at a time of higher credit card interest rates. A good example of paying higher interest on inflated prices is filling up the van with $5-$7 gas for a tour and financing shows on the credit card.

The frozen mechanicals crisis points up one of the key problems in administering the statutory mechanical license in the US: Songwriters are a fragmented group. Merely chanting to courts that you represent all songwriters and publishers in the world when you know that is not reflective of reality is not a recipe for successful negotiations. It was only a matter of time until one of these deals imposed on the songwriter community turned sour. Frozen mechanicals turned out to be the black ice on the Nantucket sleigh ride.

Getting a result that is satisfactory to a broad group of songwriters and independent publishers is a challenge, no doubt. But the frozen mechanicals situation is actually not quite as bad as it could be.

First, we know what the dispute is about and the way the dispute could be solved. Those terms:

–Raise rates on the “Subpart B” configurations, meaning songs sold under the compulsory license in the permanent download, vinyl and compact disc configurations;

–Reach a private settlement and avoid the “battle of the experts” and further expensive litigation

–Include a broad group of activists from the US and other countries in the process.

–Create a settlement that is likely to pass review by the Copyright Royalty Judges (and ultimately Congress) and is at least less likely to get appealed by George Johnson and whoever else can manage to be granted standing.

–Unite the community against the streaming services.

The detailed and well-thought out sober comments by so many songwriters that seem to have been at least somewhat compelling and persuasive to the Judges tell the RIAA members who they must deal with and also give a good idea of what these group would find satisfactory. The RIAA members also have a unique opportunity to extract themselves from the “late fee waiver” deal that can be recast on more appropriate terms and include a much wider group with far fewer relations that give the appearance of conflicts.

Second, this is why it was encouraging to read this quote from Mitch Glazier, a long time community leader, deal maker, and head of the RIAA in an Ed Christman post from yesterday–a comment made outside the four corners of the RIAA’s controversial filing now characterized as “procedural”:

Glazier, however, says that he has no control who participates in the CRB proceedings — it has its own process that makes those decisions — he does have a say who participates in the negotiations for a new rate settlement and wants to include other independent songwriting groups, publishers and labels. He wants their point of view to inform negotiations, he says. But in order to have those discussion, it will take more time than the CRB currently would allow, thus the motion to delay responding to the judges on how adjudication should move forward.

I have to imagine that the major labels probably went into this Phonorecords IV proposed settlement first filed in early 2021 (so negotiated in late 2020, one would guess) feeling that surely their counterparties would have polled their membership and reached a bona fide consensus before making the deal. Particularly when the streaming companies were so obviously going to make the “good for the goose” argument in the streaming piece about frozen rates being applied equally to mechanicals regardless of who was paying.

This is particularly true when the services get to pay the old rates pending an appeal and are therefore incented to stretch out appeals as long as they can as a matter of drill if not sport. Another huge miss in the negotiation of Title I of the Music Modernization Act.

Songwriters know that if they are not at the table, they are on the menu as our dear late Governor Ann Richards used to say. It’s nice to see Mitch Glazier offering to include the wider group in settlement negotiations and we should all look forward to see how that goes. As Mr. Glazier said, his members are free to negotiate with anyone they want, and it’s obvious that the people who held themselves out has having all the experience and authority to speak for all songwriters in the world fell a bit short this time.

Let’s not make that mistake again. We are on the clock, and the golden hour for settlement is at hand.

The U.S. central bank, the Federal Reserve, is expected to raise their target interest rate by 1/2% or (“50 basis points”) several times this year. These rate raises are usually executed at meetings of the Federal Reserve on a monthly basis.

How high will these rates go? One way to look at a potential near-term target is for the Fed to reach a “neutral interest rate”, that is one that is neither accommodative nor restrictive. Given that inflation is currently in the 8% range and likely to go higher still in the near term, that means raising the federal funds rate to over 8%. Such an increase highlights the debt trap that the US is in (along with most of the world), because if the government had to pay over 8% for government bonds it would bankrupt the country or require massive tax increases in a shrinking GDP. The failure to tax as we went along is, of course, how we got here. Government will always take easy money debt that nobody really notices rather than tax to pay as it goes, which everyone will notice and not like.

If the federal funds rates increase, then all other interest rates will increase including mortgages (and therefore rents), credit cards, and so on. You would expect to see credit card interest rates at or above 25%, for example, so if you’ve been paying for inflation on the credit card, you see where this leads.

This is all, of course, for your own good as you will be told by the same nomes who told you inflation was transitory.

The worst thing that the government could do (as President Nixon discovered in the 1970s) is to impose wage and price controls, and frozen mechanical rates are just such a wage and price control depending on which side of the sale you are on.

This is all the more reason why if the Copyright Royalty Judges are going to keep the 9.1¢ rate for vinyl, it must be indexed just like it should be on the streaming mechanical side of the house when the Google, Amazon, Apple and Spotifys of this world are paying the freight.

Or we could come up with a formula that would allow the mechanical royalty to vary inversely to the total legal fees spent (some might say wasted) in the Copyright Royalty Board. Instead of TCC we could adopt TLF and the proxy for songwriters.

But brace yourself–if you don’t get the inflation adjustment to the mechanical rate, whatever the base rate is, you are going to be looking for a chair if the fed funds rate gets to “neutral.”

Nice post by Ed Christman in Billboard explaining the continuing crisis on frozen mechanicals. Ed comes up with a rough justice quantification of the impact on songwriter and music publisher revenues in light of controlled compositions clauses in recording contracts that apply to (a) songs written and recorded by artists, or (b) songs by “outside writers” if and only if the artist can get the outside writer to accept the controlled compositions terms and rates.

For those reading along at home, one theory (aside from sheer leverage) that gets used in this context is that the artist/writer can agree on behalf of all co-writers to accept the terms of the license granted by the artist to the label in the controlled compositions clause because they are co-owners of an undivided interest in the song copyright and can grant nonexclusive licenses in the whole subject to a duty to account provided the license is not economic waste or self-dealing. Let’s just leave all that where it lays for now, but that story has never really been properly challenged–particularly the economic waste part given the rate fixing date issue and even the frozen mechanicals crisis itself. We’ll come back to that bit some other time.

The rate fixing date is a key part of the discussion for understanding the impact of unfreezing mechanicals. So what is that rate fixing provision?

Remember, the controlled compositions clause starts with reducing the minimum statutory mechanical rate in the US (and in theory in Canada subject to MLA) in effect at a point in time. That point in time is either commencement of recording (booo!), delivery, release or sale of a unit embodying the song at issue. Remember that the labels only pay mechanical royalties on physical and downloads (the rates at issue in the frozen mechanicals crisis)–streaming services pay for the interactive streaming mechanicals (and there is no mechanical for webcasting, a whole other beef).

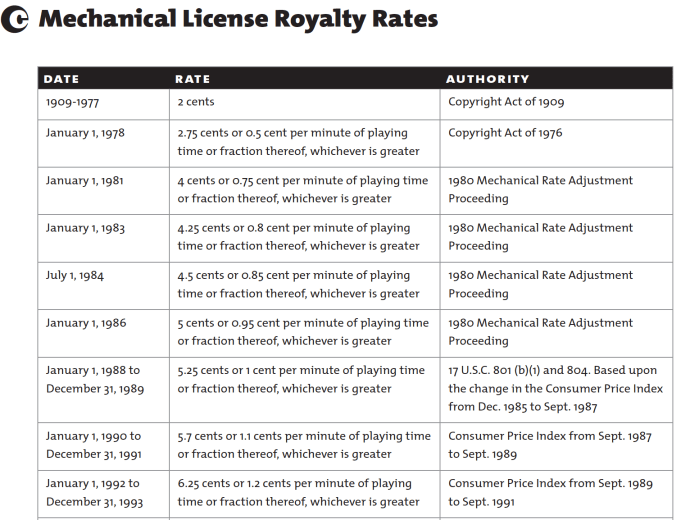

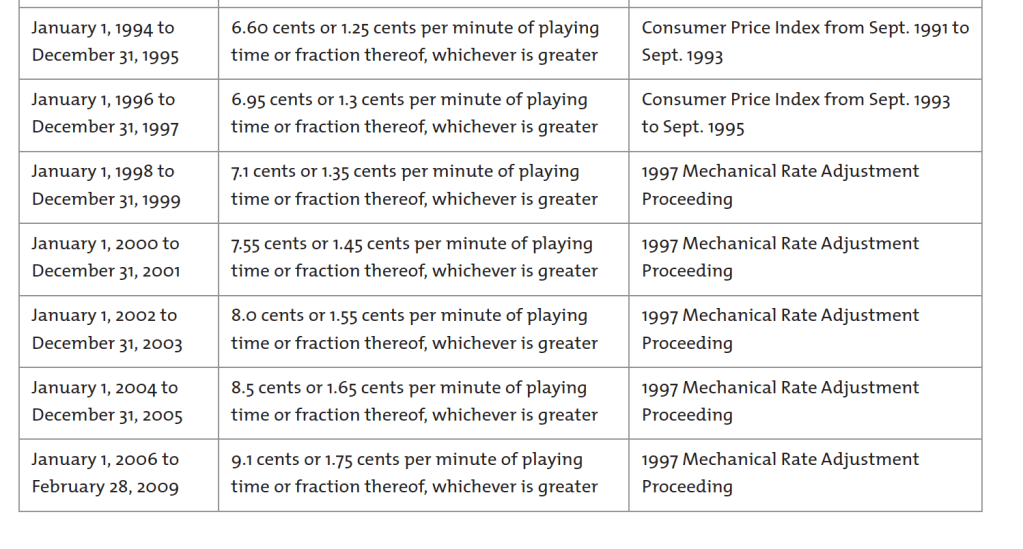

You say, wait–isn’t the mechanical rate 9.1¢? Why does it matter when the record was recorded, delivered, released or sold? Won’t the rates all be the same? And you’d be right if you were asking about a record recorded and released in 2006 or after, or a record recorded and released between 1909 and 1978, like, say some titles by Bob Dylan, The Beatles, Otis Redding or Miles Davis.

But–it wasn’t always this way. The mechanical royalty rate was set at 2¢ by Congress with the first statutory license, i.e., compulsory license, in 1909 and did not change until the 1976 revision of the US Copyright Act effective 1978. The rate then began to incrementally increase over the years until it reached 9.1¢ in 2006, a phased increase that was to compensate for Congress failing to increase the rate for 70 years, aka “the Ice Age”. The Congress really screwed up songwriters’ lives by freezing the rate at 2¢ during the Ice Age and songwriters and their heirs have been paying for it ever since, right up to the 2006-2022 period, aka “the Second Ice Age” or the Return of the Neanderthals.

In an effort to help songwriters shovel out from the Ice Age, The Congress also authorized indexing the minimum rate to inflation from 1988 to 1995. Indexing is again on the mind of the Copyright Royalty Board right now–bearing in mind that an increase in rates due to inflation has nothing to do with the intrinsic value of the song copyrights so there’s no confusion. Indexing simply applies any increase in the consumer price index to the statutory rate and preserves buying power. In a way, it is the opposite of a case about value. Indexing assumes that the value issue was already decided (in this case in 2006) and simply preserves buying power so that the “nominal” rate of 9.1¢ in 2006 can still buy the same amount of goods or services in 2022 (or 2023 in the case of the CRB rate period). Otherwise the “real” rate, i.e., the inflation adjusted rate, is not 9.1¢ it is about 6¢.

Remember–the proposed rate increase to 12¢ by the CRB is not about value, it’s about buying power because it’s solely focused on inflation.

So back to controlled compositions. It is no coincidence that at the same time as the 1978 increases were phased in, the labels established controlled compositions clauses that knocked songwriters back down. They would probably not have gotten away with freezing by contract at 2¢ so they let the rate float up but much more slowly and with several caps. The first cap is the maximum number of songs, usually 10 or 11. The next cap is the infamous 3/4 rate, where the label pays based on 75% of the minimum statutory rate. But the third cap is the rate fixing date and that’s the one we want to focus on in the unfrozen mechanicals context.

In simple form, it looks something like this contract language:

If the copyright law of the United States provides for a minimum compulsory rate: The rate equal to seventy-five percent (75%) of the minimum compulsory license rate applicable to the use of musical compositions on audio Records under the United States copyright law (hereinafter referred to as the “U.S. Minimum Statutory Rate”) at the time of the commencement of the recording of the Master concerned but in no event later than the last date for timely Delivery of such Master (the applicable date is hereinafter referred to as the “Copyright Fixing Date”). (The U.S. Minimum Statutory Rate is $.091 per Composition as of January 1, 2006);

The way that the statutory rate increases come into the controlled compositions clause is because from 1978-2006 the statutory rates increased across albums delivered across album cycles. If you consider that the rates used to increase about every two years and that an album cycle can be two years, it’s likely that LP 1 would have a lower rate than LP2, LP 2 than LP3 and so on right up to 2006.

Also remember that the increases in rates are prospective, meaning that the controlled compositions rate on recordings delivered in the future will, of course, get the higher rate, even if the past rates don’t change which they don’t, at least not yet. Also consider that permanent downloads often are excluded from controlled comp treatment and are paid at full rate, probably on the rate fixing date in the artist’s agreement. Sometimes the download rates “float” or increase in line with increases in the statutory rate, but that’s part of individual negotiations.

If there is an outside songwriter who does not agree to accept the artist’s controlled composition rate (and there are plenty of these) what happens? Typically the label will account to the outside writer at their full minimum statutory rate but will deduct that payment from the maximum aggregate mechanical royalty payable to the artist (i.e., the 10 song cap). There’s some twists and turns to this involving rates on different units “made and distributed”, but for our purposes there is one clear thing to understand:

Because of the rate fixing date which is frozen by contract (the Mini Ice Age) the artist/songwriter will be paying a higher mechanical to the outside writer from a frozen royalty “pool”.

This is why you should always, always demand “protection” for at least one outside song in your contract and then review each album to determine if that needs to be increased. This is particularly true for records made in places like Nashville where the record company will demand you work with “A” list songwriters (assume none of whom will take 3/4 rate) and then try to deduct the difference between the uncontrolled rate and the controlled rate from you (and if it gets big enough, cross it to your record royalties). (Not only will A list writers not take the 3/4 rate, they’re pissed because they can’t charge you double stat like they do double scale for sessions.)

Example: You have a 10 x 3/4 rate cap on mechanicals, the “cap rate”. That’s the 68.25¢ album rate you hear about (10 x .75 x 9.1¢). Say you have 10 songs on your album and you wrote all of them. You get the entire 68.25¢. If you had two outside songs whose writers get 9.1¢ under current rates, you deduct 18.2¢ from the cap rate, and that leaves 50.05¢ as the “controlled pool” or the total mechanical royalty payable to the artist/songwriter (actually all controlled writers, but leave aside that wrinkle).

So you can see, that’s no longer a 75% rate, it’s actually more like a 55% rate.

Now let’s assume that the new rate is 12¢. Same calculation, two outside songs now get 24¢, but the cap rate stays the same because of the rate fixing date. During the Mini Ice Age, i.e., while that cap rate is fixed at 9.1¢ x 10 x .75, the controlled pool now is expressed as 68.25¢ – 24¢ = 44.25¢, or about 48% (44.25 ÷ 91). The artist’s publisher is not going to be wild about that; the outside writer’s publishers will be thrilled.

This will start to true up on the next LP that takes a rate fixing date after the 12¢ rates go into effect. In that situation you’d be increasing both sides of the equation, so the cap rate would increase to 90¢ (10 x .12 x .75). The outside writers still get 12¢ each for two songs (or 24¢) which is deducted from the cap rate to get a controlled pool of 66¢. The true controlled comp rate is then back to about 55%.

These effects will be less pronounced if you have protection for one or more songs (or fractions of songs) or you have a higher cap, say 11 or 12 instead of 10 (with corresponding increases on other configurations). But you see the trend line.

I think this leads to the conclusion that increasing the statutory rate is a huge step forward and we should all be grateful to the Judges. The rate fixing dates for catalog titles (really the entire rate fixing date concept) must also be considered and any new effort to tweak the controlled compositions clause to effectively nullify the Judges’ rate increase will no doubt cause further conflict.

One day Congress will again act to reduce the effects of the controlled compositions clause and especially the rate fixing date, but in the meantime the Judges may well visit the issue to the extent they are able before we see the Return of the Neanderthals.

Both the consumer price index and the producer price index increased this month and the Federal Reserve is making noises like it intends to increase interest rates and reduce what is called the Fed’s “balance sheet”. Once again, the freeze on mechanical royalties for physical records like CDs and vinyl and failure to index to the consumer price index looks increasingly irresponsible if not downright antagonistic. If you agree that songwriters need to have a cost of living adjustment permanently built into all statutory rates, we have to also recognize that may be a heavy lift and needs to be supported by evidence. Here’s a few ideas.

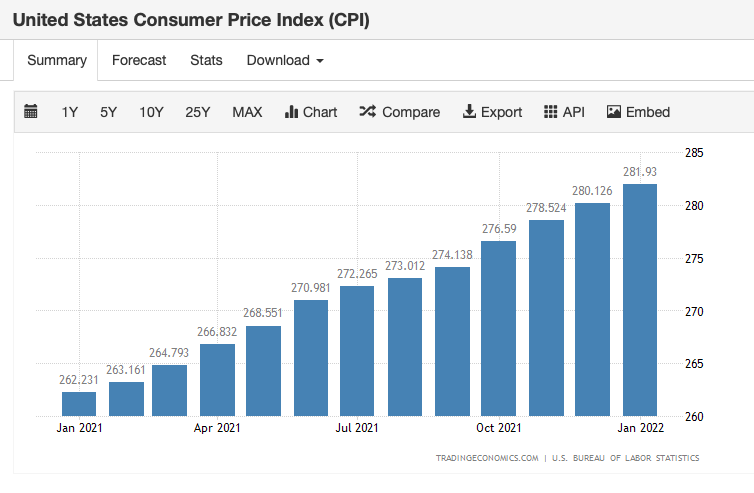

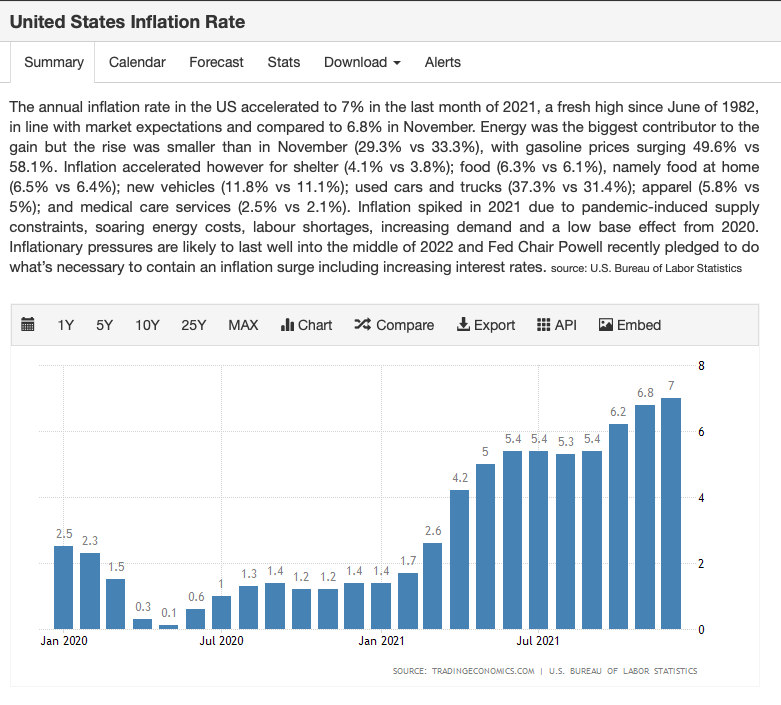

Consumer Price Index

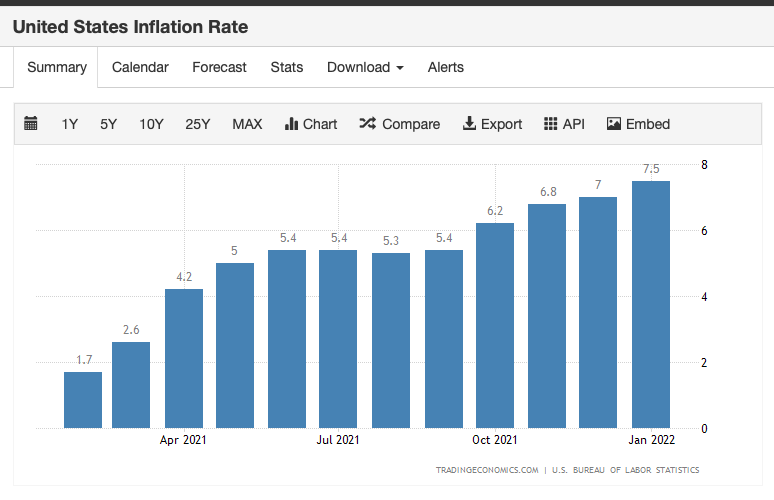

US Inflation Rate Jan 2020-Jan 2022

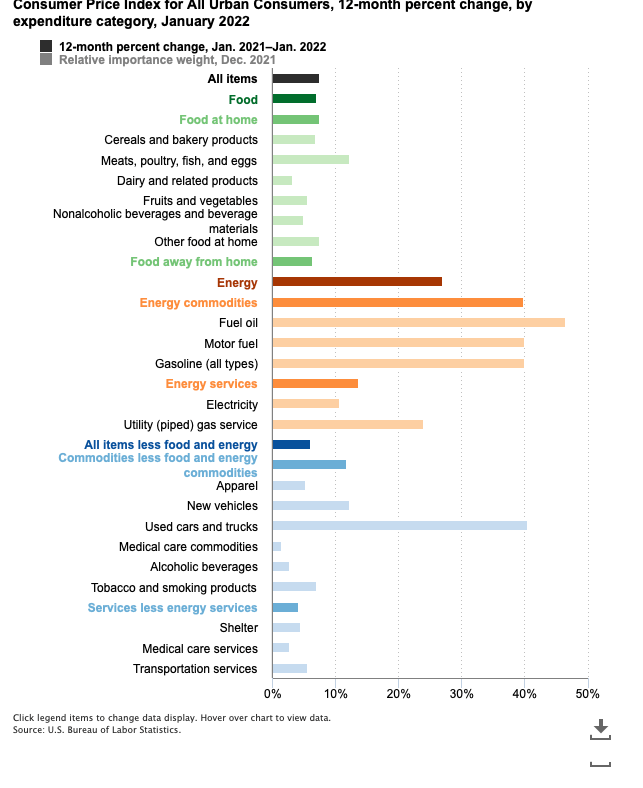

The Consumer Price Index tracked a 7.5% increase in inflation, and even excluding energy and food prices the CPI rose 6% (which applies to all those who don’t drive and don’t eat).

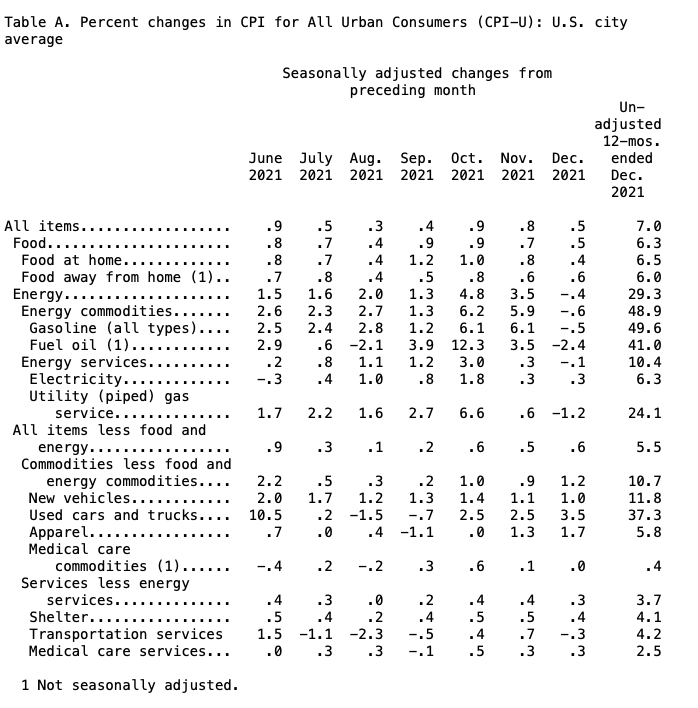

The next chart shows increases in the categories of goods that make up the CPI.

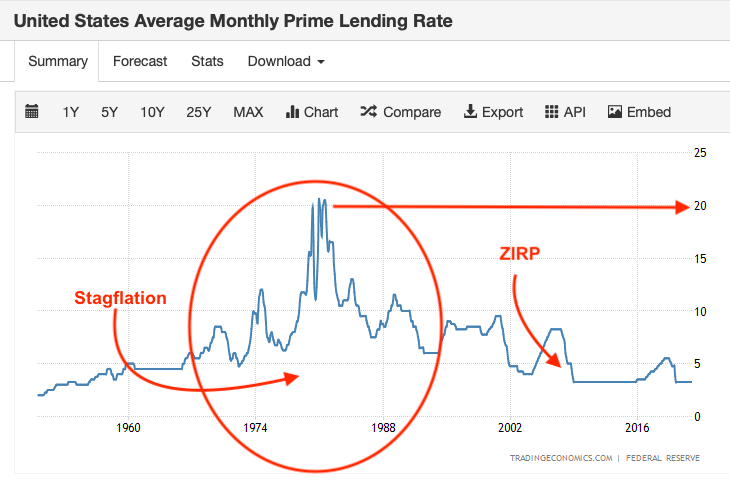

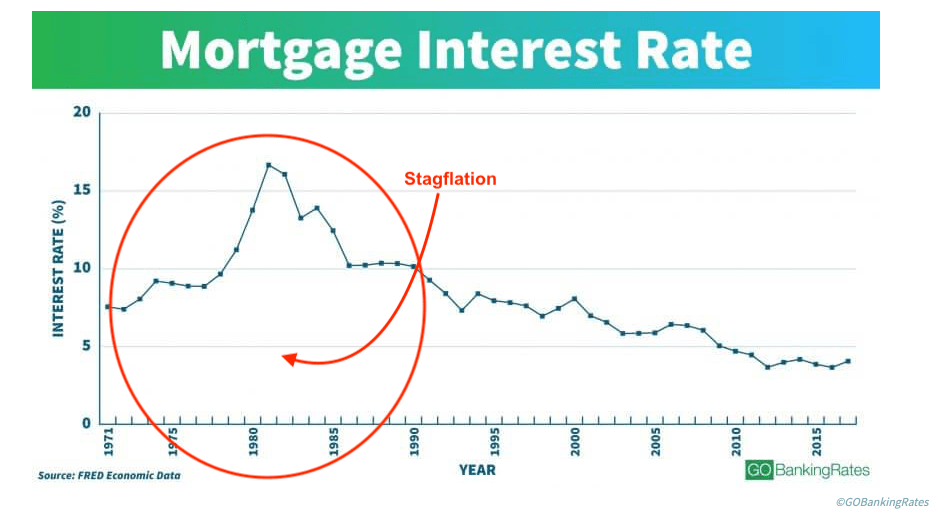

The January inflation rate is the highest since February 1982. If you don’t remember what was happening in February 1982, it was the end of the 1970s stagflation with supply side “exogenous” shocks to a number of sectors including energy. The other hallmark of the 1970s and early 1980s corresponding to the staglation is a black swan (we hope) increase in the prime rate of lending. The prime rate exceeded 20%.

One could say that the only reason that the prime rate is not much higher today is because the Federal Reserve adopted a zero interest rate policy (or “ZIRP”) in response to the 2008 financial crisis as did other central banks in other countries. The idea was that cheap money would encourage banks to make loans to borrowers as well as other banks and more debt would stimulate the economy. That’s why interest rates have been at or near zero for so long. (Not everyone thought this was a good idea, including me.) The truth is we don’t really know what interest rates would be absent the central banks’ distortion of the credit markets–perhaps for all the right reasons, but distortions nonetheless.

Increases in the 1970s prime rate caused all interest rates to increase, including credit card rates and mortgage rates. We are accustomed to seeing mortgage rates around 5% partly due to ZIRP, but mortgage rates were much higher in the 1970s. This caused a contraction in the number of people who could qualify for a mortgage and extremely high mortgage payments for those who could (not to mention “points” paid to compensate for the credit risk).

Remember the Federal Reserve’s mission is to use monetary policy to keep inflation under control and unemployment low. There are two policy “weapons” the Fed has to accomplish its mission: interest rates and the money supply. When the Fed adopts a ZIRP, what happens if those low rates don’t have the desired stimulus? That just leaves the money supply when zero interest rates lead to a “liquidity trap.”

With interest rates at their lower range (or “lower bound”) the Fed stimulated the money supply in a particular way called “quantitative easing” which involved increasing the money supply by creating money to buy treasury notes in a special way (not exactly printing money, but effectively similar) and also buying mortgage backed securities and other bonds in the open market. This was especially true in “busted offerings” when the government financed deficits with Treasury notes purchased by the Federal Reserve. And yes, that does sound rather hinky.

We’ll come back to that ZIRP policy and quantitative easing in another post, but let’s just say for now that the Federal Reserve provided more money to certain kinds of banks than they’d ever seen before in an effort to stimulate the economy without raising inflation. Yet they must have always known that an easy money policy was inflationary and due to ZIRP they had limited options–to kick the can down the road. Like a balloon payment in a mortgage, the devil would come for his due at some point. That time may be now.

Whenever inflation goes up, there is an assumption–fueled by those who wish to avoid blame–that inflation is just transitory and will recede if the central banks take anti-inflation steps, such as raising interest rates by targeting even higher interest rates on Federal Funds (currently 0.25%) on top of an already higher 10 Year Treasury Bond.

If the Fed raises rates by .25% five times this year as projected by banks like Goldman Sachs, that will essentially double the interest payment on government bonds which fuels both federal spending and the national debt. The problem with that is the higher interest rates proposed by the central bank also affect government borrowing to service the $30 odd trillion dollar national debt. Maybe you can withstand your credit card rate increasing by five percent, but the government cannot.

As you can see from the charts above, some of this inflation is increasing at an increasing rate. It is going to take time to recede. Energy markets are fluid, for example, but rents are not. The conventional wisdom is that mortgage rates and home prices vary inversely to each other. Mortgage rates can also have an effect on rental prices, too; the harder it is to qualify for a mortgage, the more people have to rent, so rental prices go up. Rental prices are also sticky, meaning that once they go up, they don’t decline very rapidly or at all. Ask yourself the last time a landlord cut your rent?

Speaking of the government’s credit card, it is important to look at the effect that inflation has on interest rates for another reason: many people have been dealing with the cost of inflation is by putting it on the credit card. Not everyone has a seven figure base salary.

Credit card interest rates are currently averaging around 14.5%, which means that if you don’t have a good credit score, you’ll probably pay closer to 20%. Bear in mind that the Federal Reserve has announced its intention to hike interest rates multiple times this year, so if that happens those in the riskier tier will be paying closer to 25% by December and people with “good” credit will be paying closer to 20%. Both of which are loan shark rates.

Bands are prone to maxing out credit cards in the best of economic times so are likely to be especially hard hit just with increased interest payments on existing balances. This multiplier effect is important because on top of everything else the cost of inflation for people who have been putting it on the credit card is going to be many times worse than it is for people who have been paying cash. This is not something that you really wanna mess with, so if there’s any possible way and I mean any possible way you can either stop making it worse or start paying down that credit card do it because this is going to get very weird.

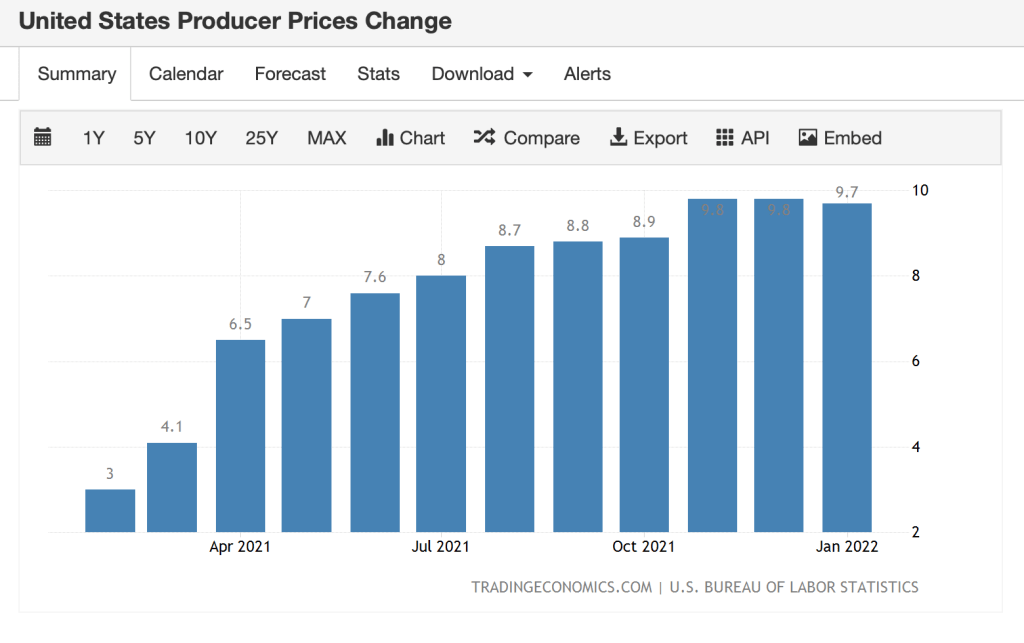

Producer Price Index

The Producer Price Index rose 1.9% in January to 9.7%. Remember, the PPI is a leading indicator of future inflation because producer prices foreshadow increases in future goods as lower priced inventories decline and price increases are in part passed through to consumers (or are in part absorbed by firms to sustain demand).

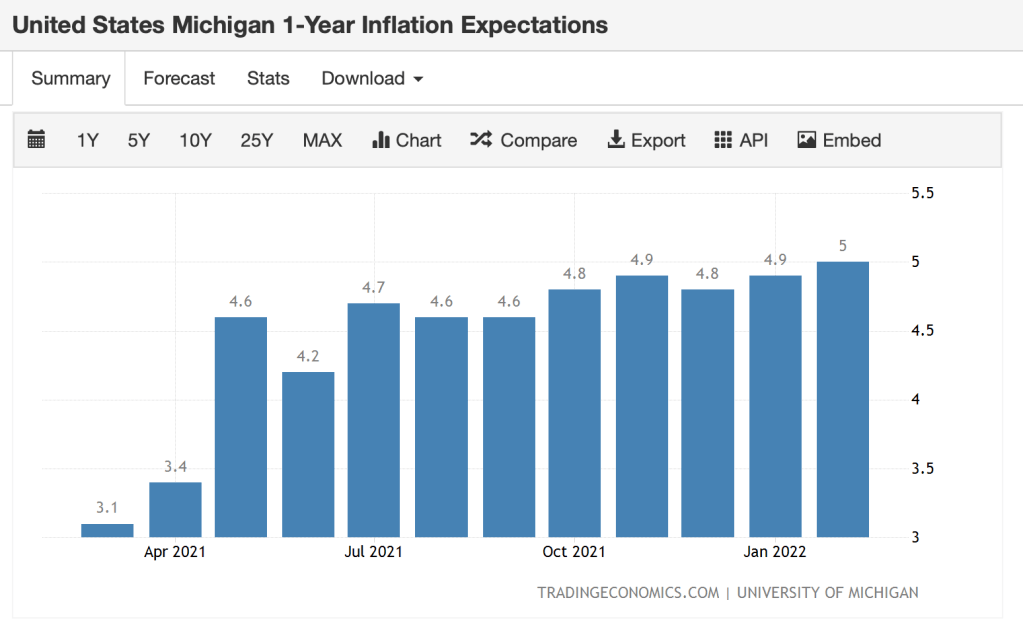

Inflation Expectations

Should songwriters expect inflation rates will effect the statutory rates in the coming years? Remember that inflation expectations can have a direct effect on actual inflation because those expectations determine wages–if you think inflation will rise, you ask for higher wages. You see this on the interactive streaming mechanical rates (which recently were amended to include a cost of living adjustment), but for some reason not on the physical.

Determining inflation expectation requires survey data, and the benchmark surveys of consumer sentiment and inflation expectations are conducted by the University of Michigan. US inflation expectations for the next 12 months rose to 5% in February of 2022 from 4.9% in January. That is the highest level of 1-year Inflation expectations since July of 2008.

Conclusion

All this confirms again that inflation for the foreseeable future is not and will not be “transitory.” Statutory rates should be indexed to inflation for the foreseeable future. This should not even be a question (and was the rule in the latter half of the 1970s, and all of 80s and 90s). If the Copyright Royalty Board will not include a cost of living adjustment in all statutory rates, perhaps it should be imposed on them.

We hear from an increasing number of songwriters who are learning about what is going on in the current rate fixing movements at the Copyright Royalty Board, some for the first time. In a nutshell, the Copyright Royalty Board rate fixing is a hugely expensive process that puts generations of children through university among the participating lawyers and lobbyists. By the time the money gets through the snake, so to speak, that process results in what are, frankly, scraps delivered to the kitchen tables of songwriters at the end of the day.

The rate fixing proceeding sets the statutory rate for certain times of song uses that are mandated by the federal government. There are two main categories of statutory rates under that compulsory mechanical license: physical (sometimes called “Subpart B” rates) typically paid by record companies, and interactive streaming (sometimes called “Subpart C” rates) typically paid by services like Spotify. (At least theoretically paid–often not judging by the size of the $424 million black box that is still just sitting under the collective’s five year plan.)

We all know that songwriters have been crushed by the failure of streaming mechanical rates to keep pace with streaming’s cannibalization of physical carriers. What many songwriters do not know is that one reason why their mechanical royalty income has dropped is due to an agreement among the major players to freeze the physical mechanical rates at the 2006 level of a minimum rate of $0.091 (currently worth approximately $0.06), and then to extend that freeze several more times for a total of 15 years so far. (The freeze essentially codified the controlled compositions rate but applied to all songwriters in the world.) There is a current proceeding at the Copyright Royalty Board in which the major players have reached an agreement to extend that 2006 freeze for another five years starting in 2023 and running to 2027. Shocking, I know.

In fact, the majors have now got themselves boxed into a corner on the interactive streaming rates that they are trying to increase. Why boxed? Obviously because the services are not stupid and if they see physical mechanical rates frozen when the record companies are paying, they ask why should the streaming rates increase when the services are paying? (And before you ask, this bid rigging is “legal” because everyone gets an antitrust exemption (17 USC §115(c)(1)(D). Cute.)

There is, of course, an unholy connection between statutory rates, controlled compositions clauses in record deals and mechanical royalties–see this post for the history. Let’s just say for this post that a page of history is worth a volume of logic.

The point I want to make to you in this post is that time is going by and no progress is being made in the current proceeding (styled “Phonorecords IV“) just like there’s no progress being made in the last proceeding (styled “Phonorecords III“); some people ask why these rates and appeals were not resolved in the giveaway that was part of Title I of the Music Modernization Act (aka the Harry Fox Preservation Act) which created the Mechanical Licensing Collective. If you’re going to make a major change to collectivize songwriters and vastly expand the scope of the compulsory mechanical license, shouldn’t you have gotten something for it? I’d count myself in the group that’s asking those questions so you know my bias. In a recent comment, I called the Copyright Royalty Board the “cornucopia of chaos,” which it is at least on the mismanaged mechanical royalty rates.

Inflation and Mechanicals

One thing that everyone should be able to agree on is that inflation is a major factor in determining any statutory royalty rate. This is certainly standard with the webcasting rates negotiated by SoundExchange with the same Copyright Royalty Board. It seems that if someone just asked for “indexing” the rates to inflation, the CRB just might give it. But no one is pushing on that open door except the songwriters and publishers who commented on the majors proposed settlement but who cannot afford to be part of the Phonorecords IV proceeding itself.

So leaving aside an increase in all of the actual rates that would reflect the value of songs, it does seem that we must accept the thinking of many economists that inflation is here to stay for a while and will surely extend into the 2023-27 rate period of Phonorecords IV. I’ve posted about these indicators before, but here’s some additional information. A cost of living adjustment seems like it should be a pro forma request–it only increases the rates if there is an actual increase in the cost of living as measured by an objective standard, typically the CPI-U (Consumer Price Index-Urban) measured by the government’s Bureau of Labor Statistics.

Since we are projecting at least two years into the future, let’s consider a few metrics that measure two years into the past. What is the trend line for inflation? Up and to the right, as they say.

US Inflation Rate

Equity Markets

We normally don’t spill much ink on the stock market because markets go up and down, can’t pick a top and can’t pick a bottom. But–stock markets are often a leading indicator of the direction of growth in the broader economy so let’s look at what’s been happening in a few different measures. Remember–the conventional wisdom is that a 20% correction to the downside is the definition of a bear market.

I have been beating the stagflation war tocsin for quite some time now (since May 2021), and unfortunately I think the markets are waking up to the true-1970s style stagflationary environment we may be entering. This means lower growth combined with surging prices for consumers and producers. And that is truely bad news bears. (If you don’t know about 1970s stagflation, take a few minutes and read up on it. And even if you don’t, the negotiators of the statutory mechanical rates really should know. Some of them may have lived through it the first time around.)

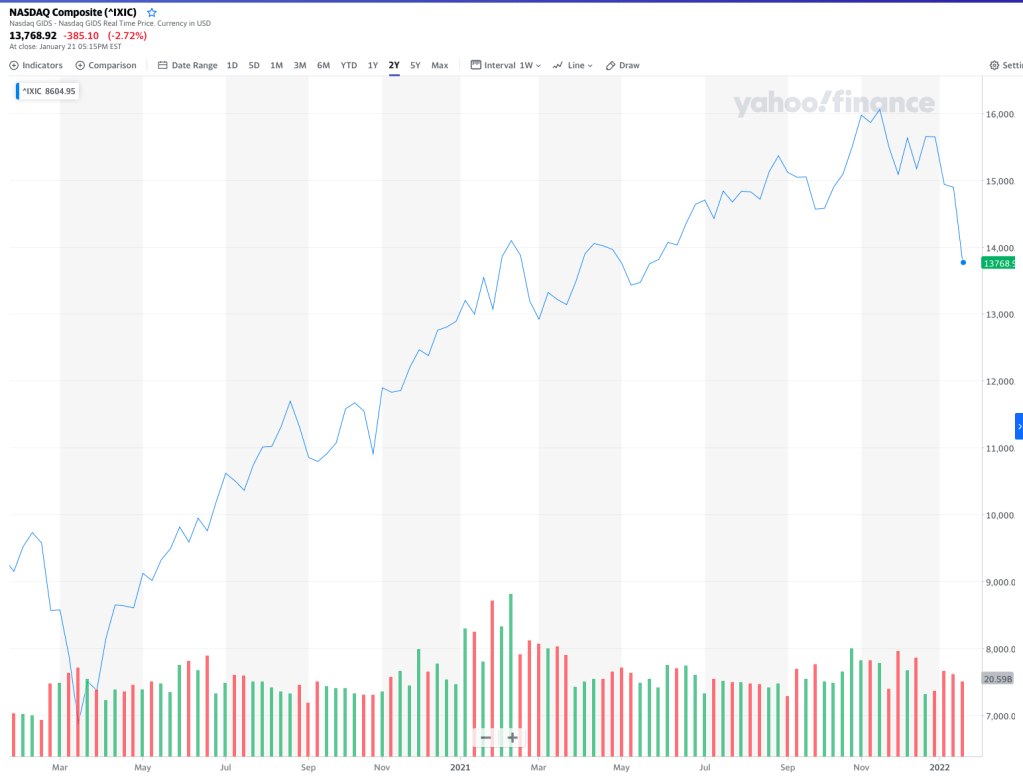

The tech-heavy NASDAQ index has dropped about 14% since November, returning to February 2021 levels with no end in sight.

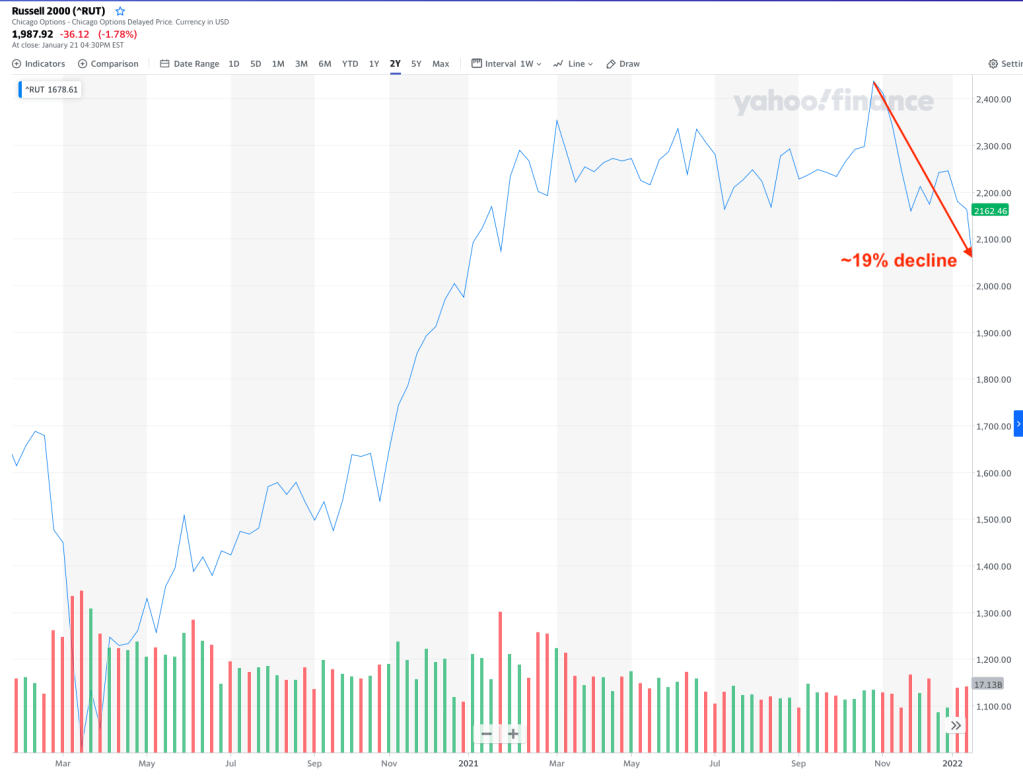

The broader Russell 2000 is more revealing with a 19% decline over a few weeks as more inflation/stagflation confirmation data comes in:

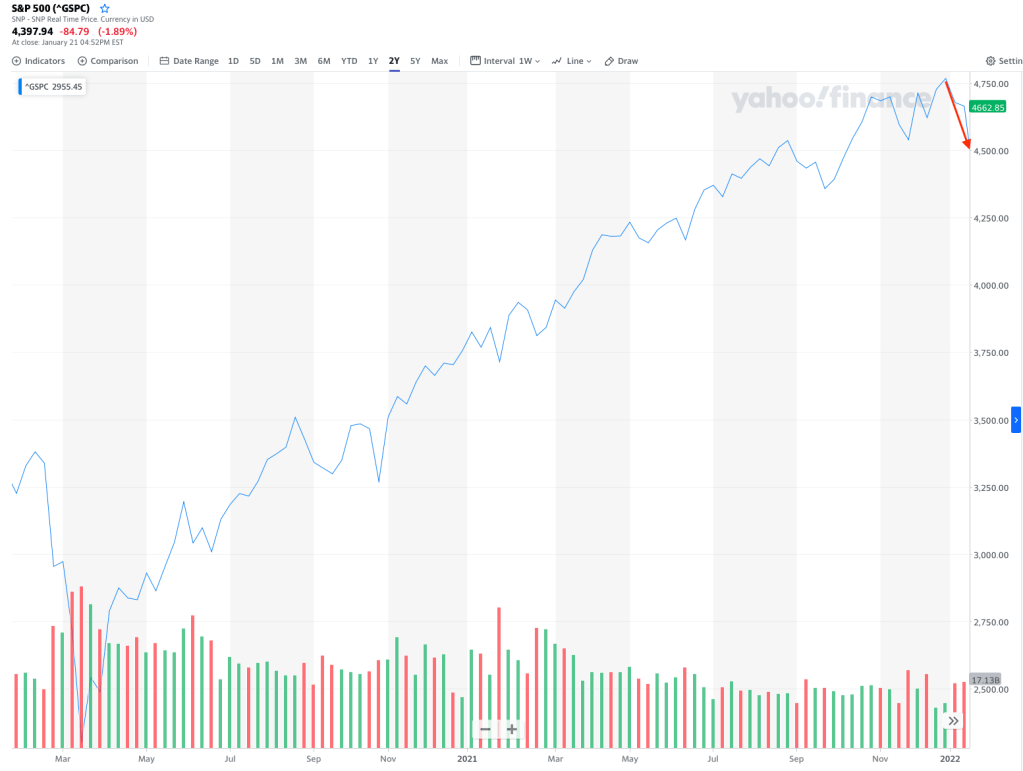

This broader decline is confirmed by the S&P 500:

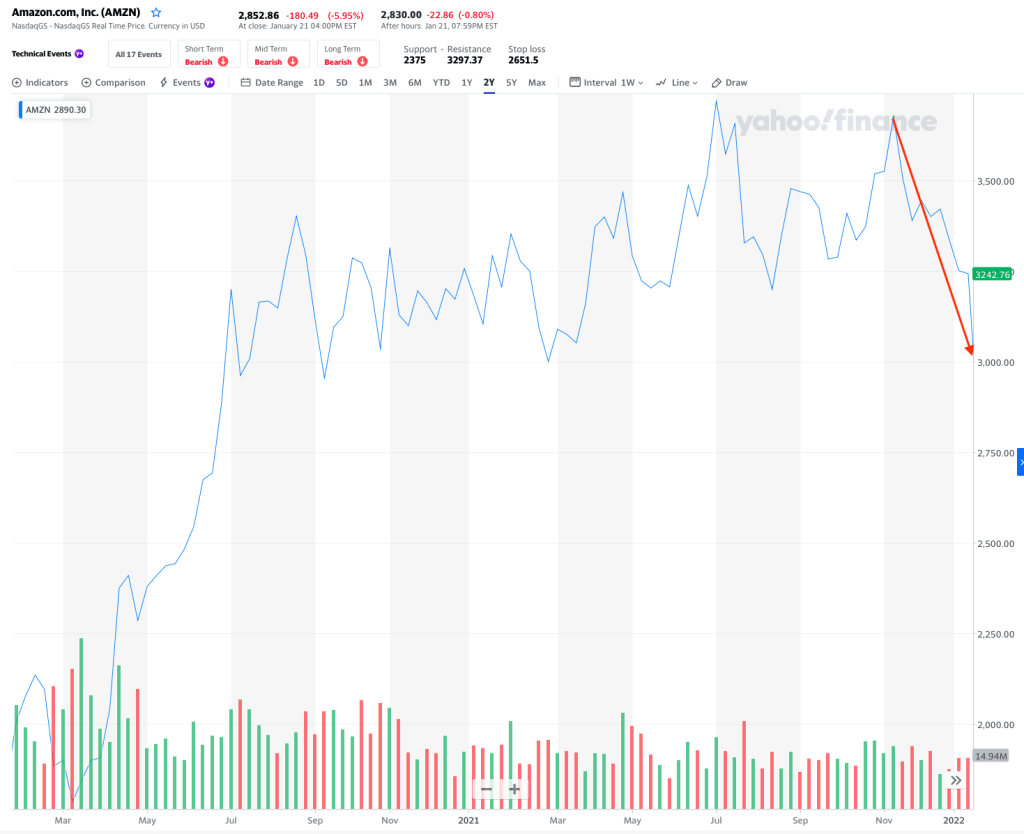

And if you were looking for confirmation of declining retail sales as a measure of growth, consider Amazon’s stock performance:

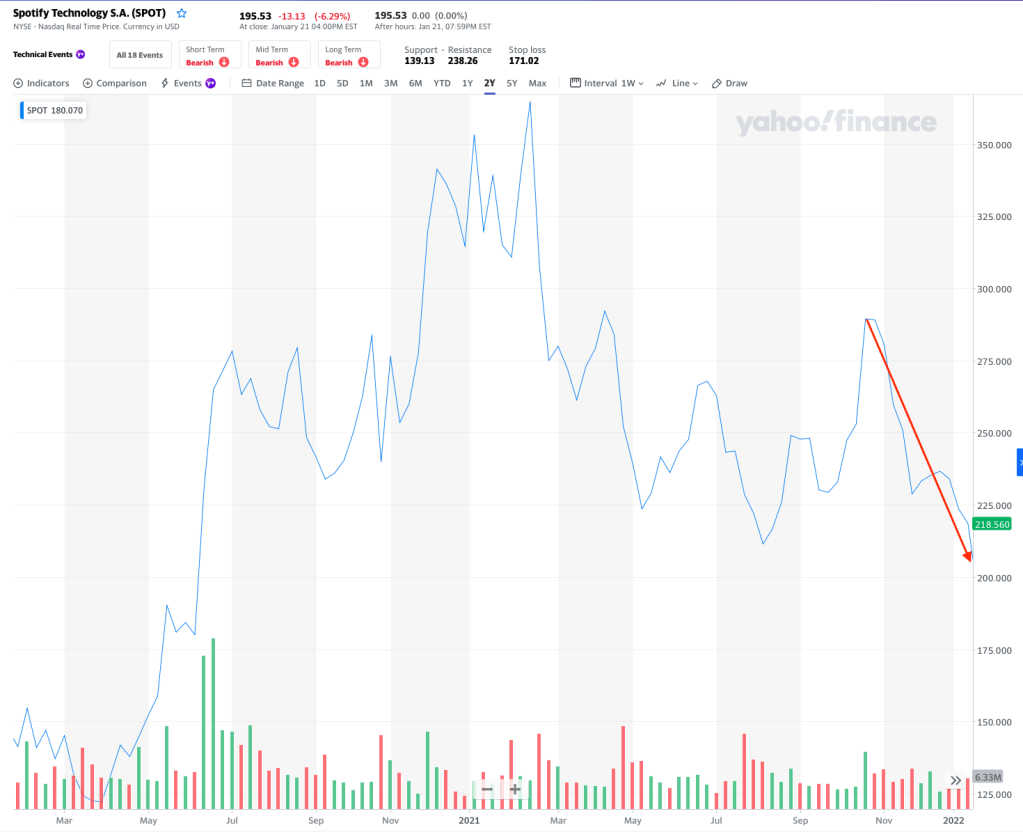

A little closer to home, consider Spotify’s recent stock performance which shows its pandemic-fueled riches coming back to reality (although not so good for any employees who got a stock option grant in the last 18 months or so):

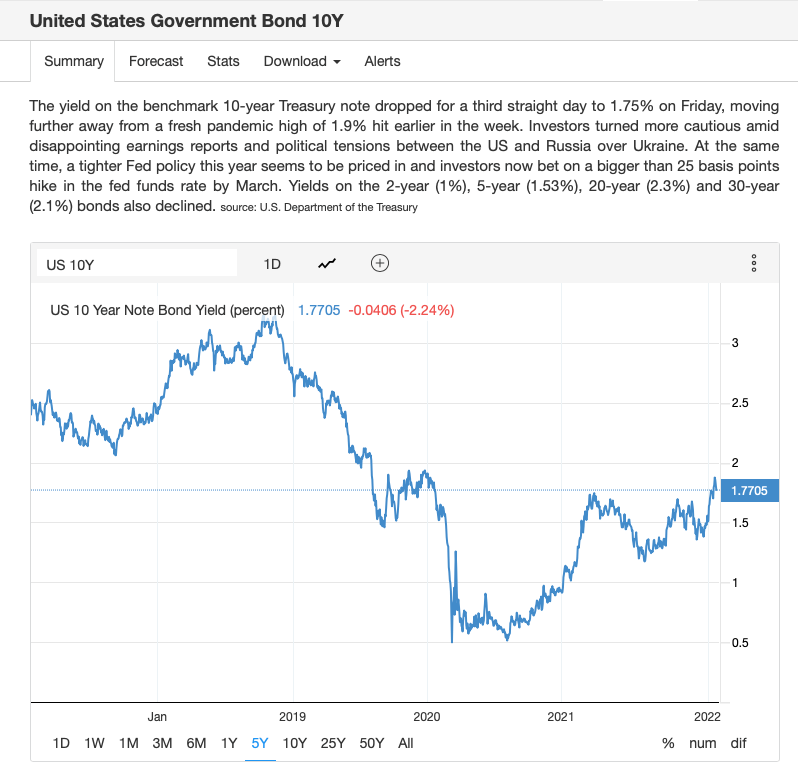

Bond Yields

Remember, the bond market is exponentially larger than the stock market. We’ll come back to this, but consider what is happening in the bond market and think about this question: what could cause both the stock market and the bond market to decline?

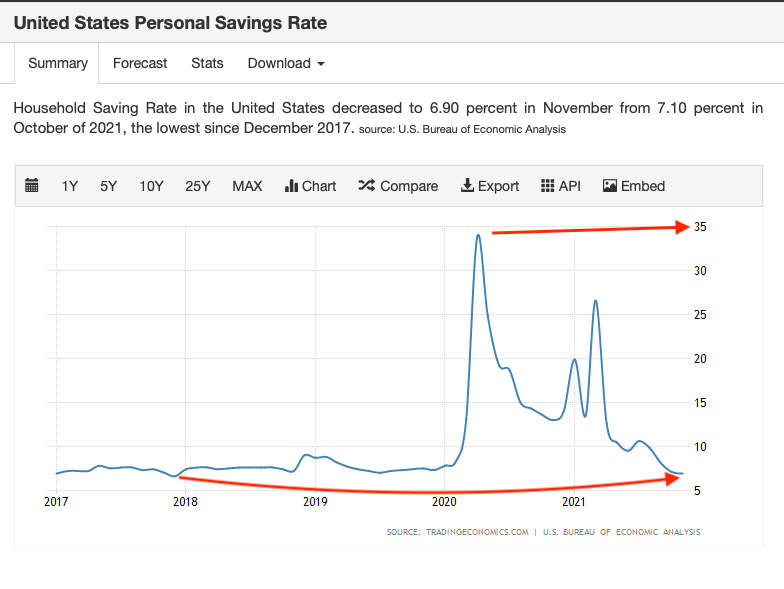

US Savings Rate

The savings rate shows a couple of anomalies where the savings rate spiked to unnatural highs of 34% in a lockdown era and again to 27% after government stimulus, but–the savings rate has sharply declined to pre-pandemic 2018-ish levels Why? I would speculate that this is partly due to rising prices of goods to consumers, particularly energy, rent and food and the decline of “real” wages (nominal wages less inflation).

Commodities

Consider a couple of inputs–there are many–but note for our purposes that these commodity prices are at or near recent highs, or are retracing recent highs. The trend line is up and to the right, which suggests that these prices are likely to continue upward into at least the first year of the Phonorecords IV rate period (2023) and potentially beyond.

Energy

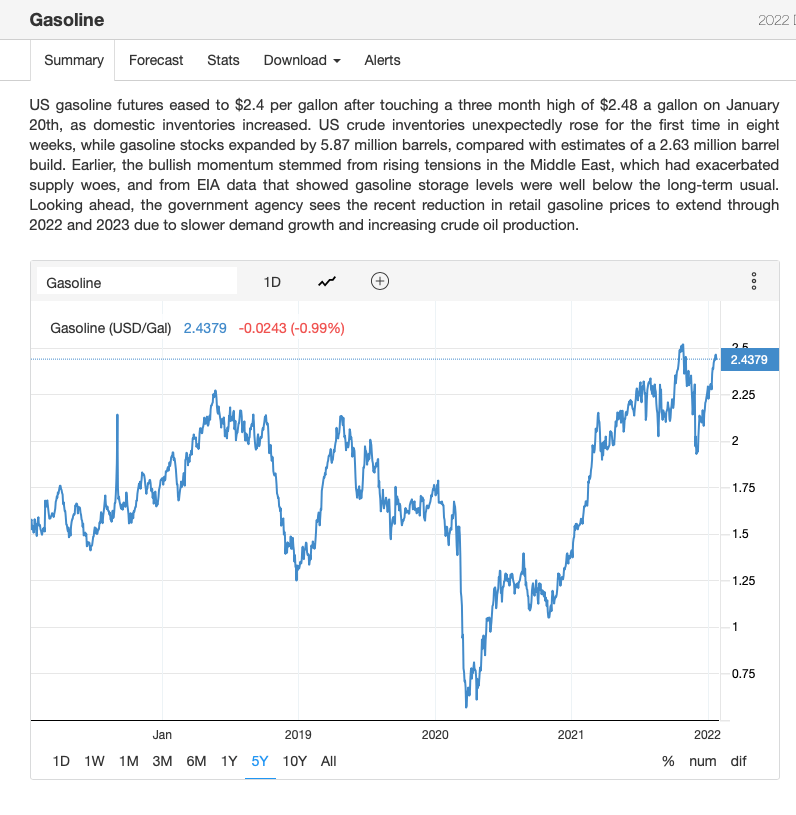

However you feel about fossil fuels, the reality for singer/songwriters or bands is that the way they try to supplement their declining songwriting income is by touring and for almost everyone, touring means gasoline. I don’t have to tell you what gasoline prices are doing–you know whenever you fill up the van. This chart is a measure of gasoline futures, which is the bet that the commodity traders are making on the future price of gasoline (not the price at the pump where you live). Again, the trend line is up and to the right.

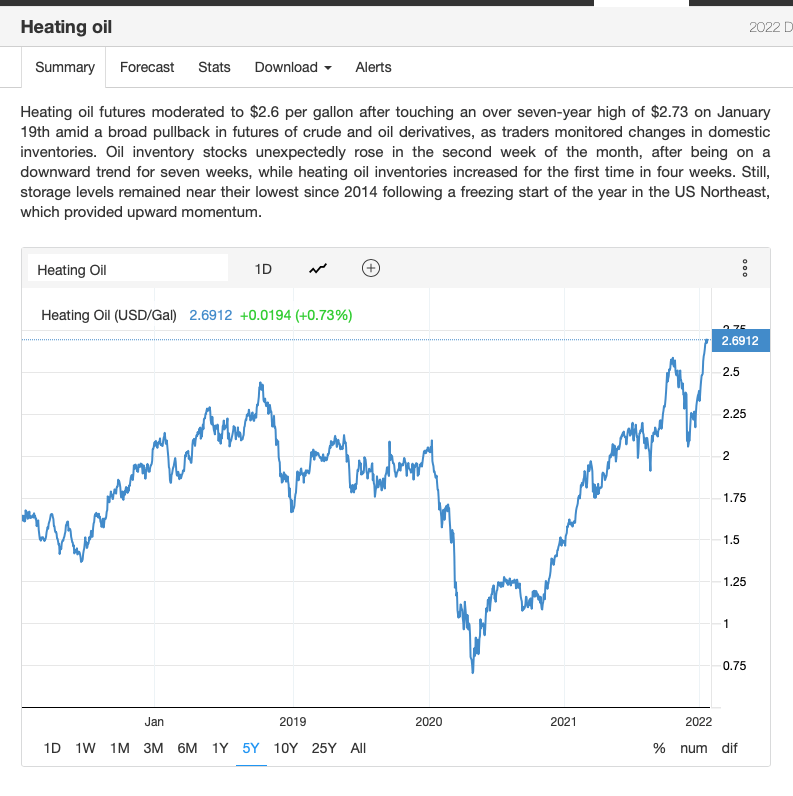

And of course if you’re going to make it to the gig or the writer room you’ll need to avoid that freezing to death thing and you’ll care about heating oil prices, up 70% year over year:

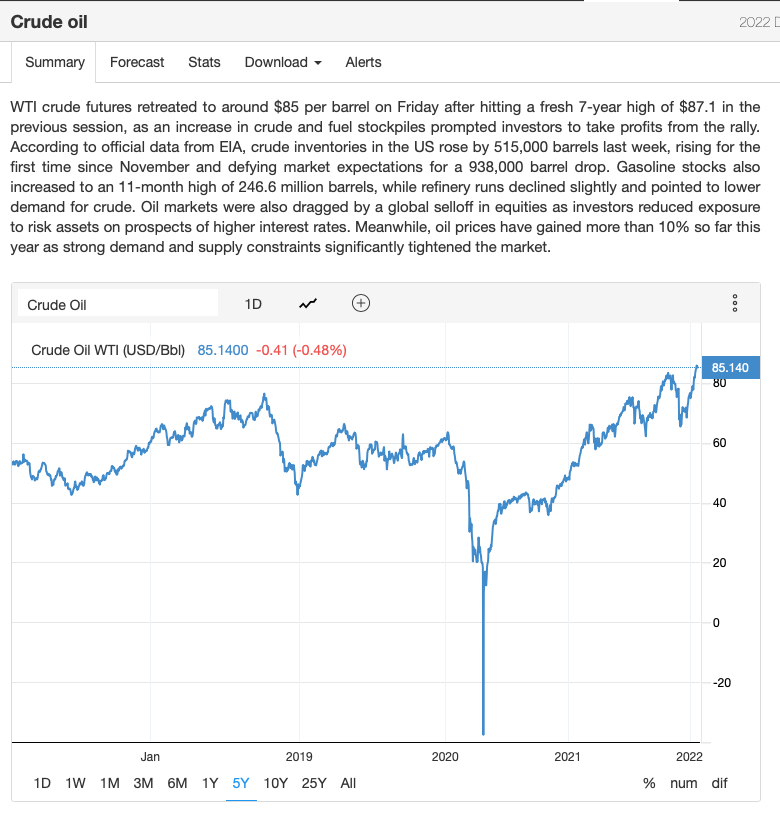

To take it a step back, crude oil is closing in on $100 a barrel due in part to exogenous supply side shocks and contractions. If crude goes over $100, we are in a whole new world that we have not seen since 2014.

Conclusion

So you get the idea, right? This is all evidence supporting a cost of living adjustment for mechanical royalties. When the stock market declines, particularly declines sharply as it is currently performing, that is largely to do an expectation of slower growth in the economy as a whole. They’ve been wrong before, but the market is actually a pretty good leading indicator of the direction of growth.

Declining stock prices foreshadow declining earnings which foreshadows declining economic growth. What happens when growth decreases? Inventories may drop, and supply declines (which is already happening and you know that if you’ve been to the grocery store lately). GDP may also decline.

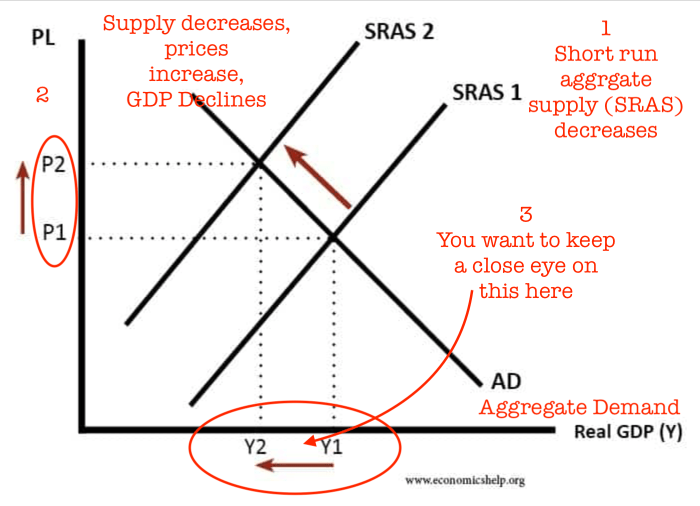

Remember the stagflation three point play? In this chart, Y1 GDP declines in Y2.

Lower growth or economic stagnation is the “stag” part of stagflation.

When bond prices go down, typically interest rates are trending up, which signals an inflationary outlook. If current bond prices decline because interest rates are increasing (or are anticipated to increase), that is most likely anticipating the Federal Reserve’s announced rate increases in 2022. The number of rate increases is anticipated to be somewhere between three and five (some say even six) in 2022. The Fed increases interest rates to tamp down inflation, so you can say that lower bond prices (which vary inversely to interest rates) is anticipating the “inflation” part of 1970s-style stagflation. Just to be clear, this is all readily available public information.

It’s becoming more obvious that we are watching a slow moving train wreck (cynics like me might say we’re beginning to get hit with the balloon payment for 2008 after 15 years of quantitative easing, but that’s a story for another day). The slower the train wreck, the more likely the wreck will occur during the Phonorecords IV rate period. Since the Federal Reserve is still busily printing money, these metrics are all leading indicators of how much blood will be left on the floor starting around March 2022 or so. And we haven’t even talked about what the announced Federal Reserve rate hikes will do to the housing market even if each one is a relatively small increase.

You don’t need an expert economist to produce any original research on this for the CRB–the question for songwriters is why don’t we already have a government rate indexed to inflation? The indexed rate is only paid if you actually get an increase in the CPI, which even then only preserves the value of whatever nominal rate you do have–it’s not a “real” rate increase. So why not at least try to get a cost of living adjustment? There’s no reason not to at least try to get indexing on every statutory rate which was the standard approach on mechanicals for many years after 1978 until the 2006 freeze. Unless your bonus is tied to a big percentage increase in the headline rate rather than the less obvious indexing that would actually protect the value of songs.

Which all seems to be to be so obvious that if you don’t have it you’d have to ask yourself, do I feel lucky? The odds are all on the house.